Riding the tax rollercoaster

Share this article

Giles Mooney and Tim Good provide guidance on navigating the complex field of personal tax calculations

Key Points

What is the issue?

Filing tax returns electronically this year could be harder than usual for many taxpayers.

What does it mean for me?

Understanding the maths behind the law and what it means for your clients is essential.

What can I take away?

A firm understanding of the challenges adviser will face to ensure clients’ tax returns will be as accurate as possible.

When I started working in tax you could count on a major new topic every year – business asset taper relief, entrepreneurs’ relief, tax credits, A-day pension changes etc. but, as majorities have shrunk and backbench power has grown, Chancellors have been forced to tinker more subtly and either change things that are off the radar of average voters or, alternatively, things that sound tempting to the electorate. The changes to dividend tax, the starting savings rate band and the introduction of the personal savings allowance all meet that logic. However, while appealing to the section of the electorate Mr Osborne was keen to impress, it seemed very little thought had been given to policing, administering or applying the rules. What has followed is, quite simply, a shambles.

Let’s start with the computational principles.

The income tax legislation requires us to allocate different types of income to the various rate bands in a prescribed order:

- Non-savings income (employment, self-employment, pension, rent etc); then

- Interest; then

- Dividends.

The starting savings rate band (SRB) replaces the 20% basic rate of tax with a 0% rate on up to £5,000 of interest income. We must also identify whether the taxpayer is entitled to either the £1,000 or the £500 personal savings allowance (PSA) – a basic rate taxpayer qualifies for a PSA of £1,000 and a higher rate taxpayer for a PSA of £500. Additional rate taxpayers (adjusted net income exceeding £150,000) do not qualify for a PSA. Any interest covered by the PSA has an effective tax rate of 0% but uses up an equivalent amount of the appropriate rate band.

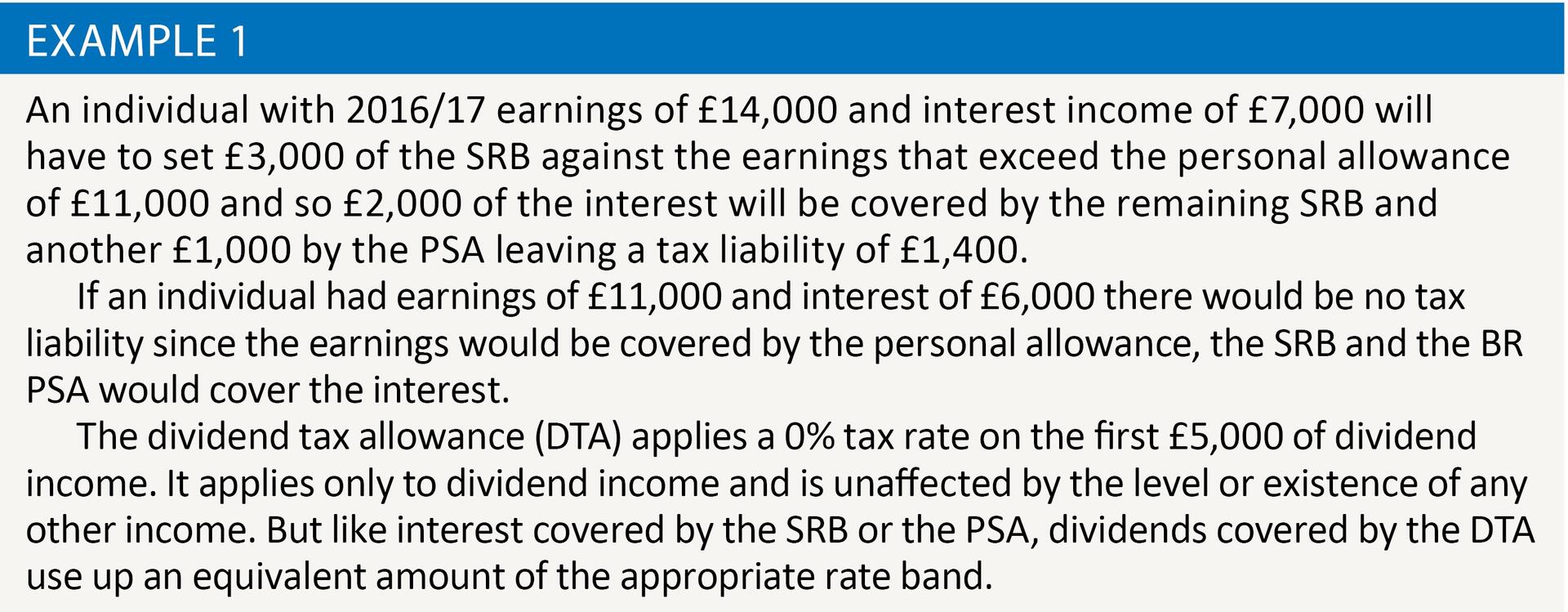

The SRB works in a very different way from the PSA. Bizarrely, the SRB must first be allocated to non-savings income before being allocated to interest. It is never allocated to dividend income. Unless the non-savings income is less than the sum of any personal allowance and other general reliefs plus the SRB there will be no SRB available to the interest. See example 1.

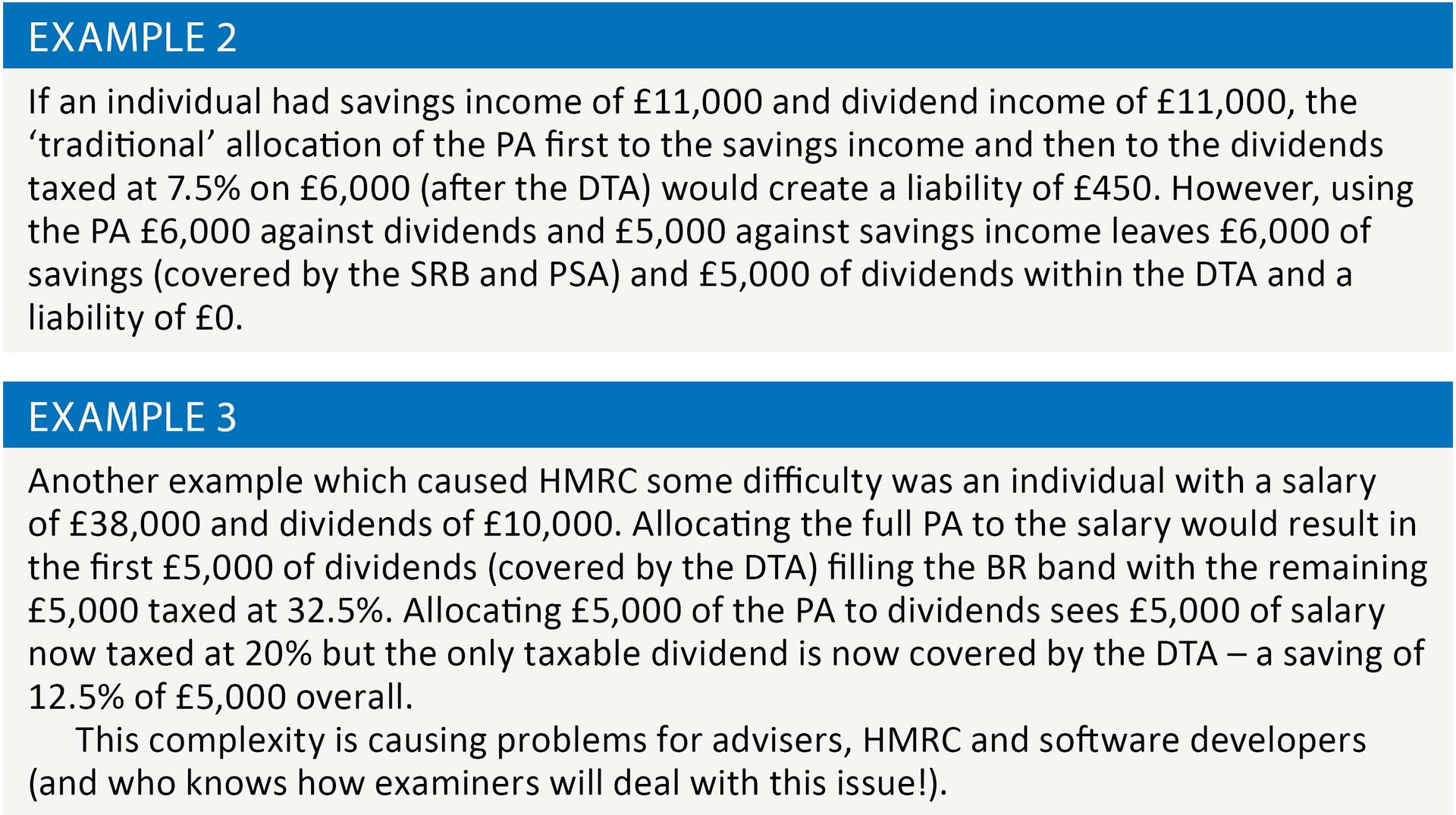

The real computational difficulties arise when we consider the allocation of personal allowances etc (PA). These include the usual personal allowance of £11,000 for 2016/17, but also any reliefs that are available against general (rather than specific sources of) income such as qualifying loan interest, sideways loss relief and share loss relief. These do not have to be allocated in the same prescribed order as the types of income. Instead (under s 25(2) ITA 2007) the PAs etc may be deducted ‘in the way which will result in the greatest reduction in the taxpayer’s liability to income tax’. See example 2.

HMRC have had to concede that these rules have made the personal tax computation too complicated for the Revenue technicians to program their tax computation accurately, with some mistakes creeping into their work. At the time of writing, an individual filing a tax return using HMRC’s online filing system with salary of £11,000 and interest of £26,000 would be told their liability is £5,000. The correct answer is £4,000 but, unfortunately the Revenue system isn’t allocating the income to the SRB correctly, creating the £1,000 overcharge.

As a result of these issues (which affect three distinct groups of taxpayers) the software houses have been told by HMRC that their software should not be used to file online if a taxpayer has combinations of particular types of income. Instead, a paper return should be submitted. Each year HMRC list various people for exclusion from e-filing. Many will be familiar with those excluded by career (MPs, judges, GCHQ employees etc) with others excluded because of software issues. All those who file on paper because they’re excluded have an extension to the normal deadline of 31 October for paper returns to the online filing deadline of 31 January.

The potential tax overcharge if online filing is used for these so-called ‘exclusion’ cases could be as much as £1,000.

We have been working with HMRC since May 2016 through our software company, Absolute Accounting Software Ltd, and HMRC have incorporated some of the algorithms that we have developed into its own briefing document and spreadsheet for the 2016/17 tax calculation. But the HMRC team responsible for coding the main HMRC self-assessment system were unable to complete the task from the Excel algorithms in time for the start of the new tax year.

Most commercial software houses follow the HMRC specification when coding their software and so, if the HMRC system has in-built errors, those will have been replicated by those commercial providers – otherwise returns filed using commercial packages will risk being rejected. Some developers have written their own code which differs from HMRC code but this will not prevent rejection under e-filing.

Some software developers have added warnings to their systems to advise users that paper filing should be carried out. However, some have not managed to capture all the exclusions accurately, so testing well in advance of major use of this year’s software is advisable for all firms or incorrect filing could occur unnoticed.

It will also be advisable to prepare returns earlier than normal to allow for time for returns to be signed and returned by clients (many of whom won’t have been asked to sign a tax return for over a decade).

The three main groups of taxpayers who could be affected are:

- those with total income made up of savings and non-savings income over £32,000 of which the non-savings income is between £11,000 and £16,000; and

- those with non-dividend income of £27,000 to £32,000 plus dividends which take their total income to over £145,000.

- Higher rate taxpayers with interest income of more than £500 but who would be additional rate taxpayers if qualifying deductions (e.g. losses or loan interest) are ignored.

Taxpayers in Group 1 should benefit from the savings rate band of up to £5,000 as their non-savings income not covered by the personal allowance will not use all of the savings rate band. The HMRC tax return software specification fails to give the benefit of the savings rate band in this scenario and hence overcharges taxpayers in this group by up to £1,000, as shown in the example above.

Taxpayers in Group 2 do not receive any personal savings allowance, as their income makes them additional rate taxpayers. However, they do qualify for the £5,000 dividend tax allowance. The HMRC tax software specification incorrectly deducts the dividend tax allowance that falls in the unused basic rate band from the higher rate band which then pushes dividends up into the additional rate. This error could cost up to £280 if the return is filed electronically instead of by paper.

Taxpayers in Group 3 are entitled to a personal savings allowance of £500 but the HMRC calculation does not allow this amount.

Absolute has developed a spreadsheet that gets the right answer and has already supplied this to over one thousand accountancy firms. It now seems that most agents are likely to need such a tool to satisfy themselves that a particular client will be paying the right amount of tax.