Rocket science

Share this article

Greg Morris provides a comprehensive guide to the taxation of pensions

Key Points

What is the issue?

Reducing pension allowances has meant more and more people are impacted by potentially significant and unexpected tax charges.

What does it mean to me?

The mechanics of pension taxation are complicated, but understanding the issues and taking relevant advice can save a lot of value in the long term.

What can I take away?

Exceeding the allowances may incur additional tax, but this doesn’t mean that pension saving should be ceased.

Pensions and taxation are two of the most fiendishly complicated subjects. Put them together and you have a subject akin to rocket science for most people.

This article is intended to cover the basics of how pension saving within (and pension income taken from) registered pension schemes are taxed, the impacts on individuals and some thoughts on what the future may hold. It doesn’t attempt to cover all of the issues and quirks in pension taxation (and there are plenty). Many changes have happened in recent years, so the contents of this article may be subject to revision in short order!

Individuals should of course take appropriate financial and tax advice before making any changes to their financial plans.

Background

HMRC has estimated that pension tax relief cost the Exchequer some £34.2 billion in 2014/15. Relief on employer National Insurance Contributions costs a further £13.8 billion.

Pension saving is tax exempt at the point of saving, tax exempt whilst invested prior to retirement, then taxed as income upon receipt. This is often referred to as ‘Exempt-Exempt-Taxed’ or ‘EET’.

The current pension taxation regime started on 6 April 2006 (‘A-Day’). Prior to A-Day, pension taxation for defined benefit schemes was ‘benefits based’, i.e. there was a limit on the nominal size of the benefits that could be taken from a pension scheme. This maximum pension was 2/3rds of remuneration at retirement. On the face of it, this seemed quite straightforward, however in reality there were numerous different underlying regimes and individuals could find themselves subject to different limits for different schemes. Defined contribution schemes were capped by limiting the tax relief on contributions made into them.

To remove this complexity and attempt to merge the two systems, the Government introduced ‘Pensions Simplification’ at A-Day and we moved to the current ‘value based’ system, with the introduction of the Annual Allowance (AA) and Lifetime Allowance (LTA).

The aim was a ‘one-size-fits-all’, easily understandable approach. However Defined Benefit (DB) and Defined Contribution (DC) pensions are fundamentally different and any single regime will struggle to be equitable between them. Further, for DB schemes, a simple approach struggles to maintain equity between individuals of varying ages with varying benefit terms.

The LTA was initially £1.5m and grew to £1.8m in 2010/11. The AA started at £215,000 p.a. growing to £255,000 p.a. over the same period. In subsequent years, these allowances have experienced several reductions to the current LTA of £1m and AA of £40,000.

These reductions, combined with associated transitional protections have introduced more complexity again.

Basics

Pension saving

Income tax relief is provided on pension saving made in each year up to 100% of your earnings. Individuals without earnings for tax purposes can still contribute up to £3,600 p.a. gross and receive basic rate relief on this amount.

However, individuals will incur a tax charge if:

- the pension saving exceeds the Annual Allowance (AA) (£40,000 p.a.); and/or

- the ultimate value of pension saving over the working life exceeds the Lifetime Allowance (LTA) (£1m).

(State Pensions are not assessed against the AA or the LTA.)

Tax relief is provided at the marginal rate of income tax, be that basic rate (20%), higher rate (40%) or additional rate (45%). For earnings above £100,000, an individual loses their Personal Allowance and will therefore experience a higher effective rate of income tax; in 2017/18, earnings between £100,000 and £123,000 will be effectively taxed at 60%. Individual pension contributions in this range can therefore provide effective tax relief at 60%.

Investment growth on pension saving

Investment return or growth on pension saving made in pension schemes is tax free.

Pension income

Pension income (including State Pension) is subject to income tax. This sounds obvious, but it often features as an FAQ about retirement. The exception is, of course, the Pension Commencement Lump Sum (‘PCLS’) or ‘tax free cash lump sum’ taken at the point of retirement, upon which no tax is payable.

Method of tax relief

There are two different methods of providing tax relief on pension saving, and pension schemes can only provide tax relief through one of these methods. These are known as Net Pay Arrangements and Relief at Source Arrangements. Individuals should be aware of what method is used in their pension schemes, as this will determine how much relief is provided automatically, and how much needs to be claimed via Self Assessment.

The Annual Allowance (‘AA’)

What is the AA and what is the charge for exceeding it?

The AA is the limit to the total amount of contributions that can be paid in to DC schemes and the total capitalised value of benefits that individuals can build up in DB schemes each year, for tax relief purposes.

Exceeding the available AA results in an AA charge for the individual. The charge is intended to remove the relief given automatically on pension saving exceeding the AA. In simple terms the relief given is the tax that would have been paid if the value of the saving exceeding the AA was taken as income. The charge could therefore be at the basic, higher or additional rate or a combination of those if the excess saving would have crossed any of these tax thresholds.

The tax charge is only levied on the saving exceeding the AA; the saving up to the AA still attracts full relief.

How much is the AA?

The standard AA is £40,000 p.a. From 6 April 2016, higher earners (earnings over £150,000) will see their AA ‘tapered’ down to a minimum of £10,000 p.a. (see below).

Once an individual accesses any DC saving ‘flexibly’ under the new freedoms recently introduced i.e. draws some cash, they are then subject to a reduced Money Purchase Annual Allowance for any future contributions (‘MPAA’). The MPAA was initially set at £10,000 p.a. but the Spring Budget 2017 confirmed that this would reduce to £4,000 p.a. with effect from April 2017. Due to the snap general election, the Government have not had chance to include the necessary provisions in the pre-election Finance Act. Legally, the MPAA therefore remains at £10,000. If the current Government is returned to office, the reduction to £4,000 is expected go ahead. The effective date of the change is however uncertain. The MPAA restricts individuals from accessing pension savings and re-contributing those savings into another pension and claiming tax relief again.

Individuals subject to the MPAA still have the remainder of their full (or tapered) AA for use for DB saving (assuming they are still in an open DB scheme).

What should be assessed against the AA?

The value of pension savings for assessment against the AA is called the Pension Input Amount (‘PIA’). Each tax year, individuals must assess their total PIA across all of their active schemes, declaring any excess over the AA via Self Assessment.

Active DC Schemes are those into which contributions have been paid by or on behalf of the individual in that tax year.

Active DB schemes are those in which employees continue to earn additional benefits, by virtue of additional service and/or increasing salary in that tax year.

Scheme administrators must notify individuals of their PIA when they have exceeded the standard AA in that scheme, so the individual can complete their Self Assessment. This information is usually provided on annual benefit statements.

How do I calculate my PIA?

For a DC scheme, PIA is the gross amount of all contributions paid into the DC scheme during the tax year (by the employee and employer). Investment return (or losses) are excluded.

For example, an individual earning £20,000 p.a., pays 5% gross contributions with 5% employer contributions has a PIA of £2,000 in that scheme.

For a DB scheme, PIA assessment is more complicated. Individuals accrue additional pension benefits each year through additional service and/or salary increases. The PIA is the ‘capitalised’ value of the resulting increase in benefits as calculated by:

PIA = 16 x [pension accrued at the end of the tax year less pension accrued at the start of the tax year*]

* Statutory inflation proofing of accrued pension is excluded, hence pension accrued at the start of the year is uprated in the calculation. The inflation figure used is normally the increase in CPI over the 12 months to the September before the tax year.

For example:

John has 25 years in a DB scheme. Each year he accrues a pension of 1/50th of his salary. John’s salary is £50,000 p.a. at the start of the tax year, increasing by 2% over the year to £51,000.

Pension at the start of the tax year = 25/50 x £50,000 = £25,000 p.a.

Assuming 1% CPI, the inflation-proofed start figure becomes: £25,250 p.a.

At the year end, John has completed 26 years and has a higher salary.

Pension at the end of the tax year = 26/50 x £51,000 = £26,520 p.a.

PIA = 16 x (£26,520–£25,250) = £20,320

If members also accrue a lump sum in addition to pension (common in public sector schemes) then the inflation adjusted increase in the lump sum should also be included.

Care is needed on the amount of benefits used in this calculation. This should be the amount of benefits that the member would get if they were at normal pension age at the date of calculation.

There is (usually) no need to include increases in benefits from DB schemes that you left previously, unless that scheme grants higher increases prior to retirement than the statutory minimum.

What if I don’t use up my full AA?

Unused AA from the previous three tax years can be carried forward to offset any PIA exceeding the AA in the current year. The oldest year’s unused AA is used first.

(The AA was £50k in 2013/14. Due to transitional arrangements for the AA Taper (see below), a higher AA was available (possibly up to £80k) in 2015/16.)

How do I pay the AA charge?

After declaring the necessary information via Self Assessment, payment of the AA charge may be made as follows:

- The individual can pay the tax charge directly; or

- If the PIA in a single scheme exceeds the standard AA and the charge in that scheme exceeds £2,000, the individual can nominate the scheme to pay the charge. The scheme administrator then deducts the payment from the individual’s pension saving. The individual remains liable for payment and must notify HMRC that the scheme will pay the charge.

Individuals should consider the implications of this second ‘Scheme Pays’ method carefully as it will naturally reduce the ultimate benefits received.

Paying the AA charge personally means paying the charge from taxed income. With ‘Scheme Pays’, the payment is effectively made from gross income, but will mean taking money from a tax efficient investment vehicle and reduce the fund value.

Which payment option to choose will depend upon individual circumstances.

What is the AA Taper?

From 6 April 2016, the AA for high earners is subject to tapering.

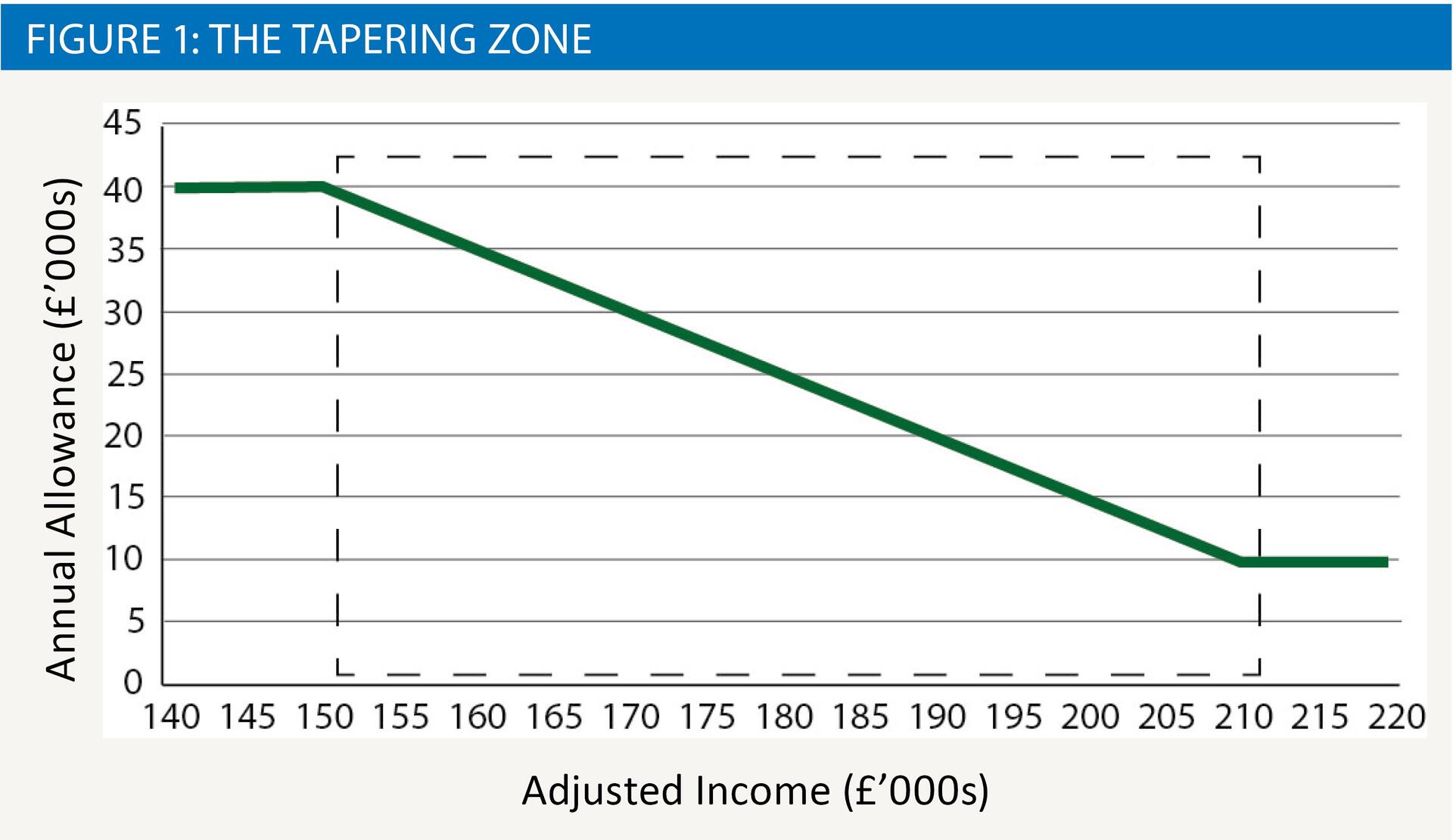

Individuals with an ‘Adjusted Income’ of between £150,000 and £210,000 lose £1 of AA for every £2 of Adjusted Income within this band: e.g. an Adjusted Income of £180,000 p.a. tapers the AA to £25,000. The minimum tapered AA is £10,000. See figure 1.

Tapering doesn’t apply if ‘Threshold Income’ is £110,000 or less. The detailed definitions of these incomes are set out in the legislation, but they can be interpreted broadly as:

Threshold Income = Total income from all sources subject to income tax.

Adjusted Income = Threshold Income plus the PIA in that year.

Inclusion of the PIA in Adjusted Income means that the employer’s contribution to the scheme is counted in the taper assessment. There are some anti-avoidance provisions for new salary sacrifice arrangements post 8 July 2015 in the Threshold Income definition.

What is the impact of AA Tapering?

Impacted individuals may not know what their total income will be until later in the tax year, particularly if they have significant variable income elements. This will mean uncertainty over their tapered AA for the year. In a DB scheme significant remuneration increases will increase Adjusted Income, tapering the AA and significantly increase the PIA in that year.

In the Tapering Zone, individuals exceeding their Tapered AA may be subject to an effective rate of tax of 67.5%.

The Lifetime Allowance (‘LTA’)

What is the LTA and what is the charge for exceeding it?

The LTA is a limit on the capital value of total benefit that can be drawn from schemes.

Taking benefits that exceed the LTA triggers a tax charge on the excess over the LTA. The amount of the charge depends upon the method of benefit access and is as follows:

a) 55% if taken as a lump sum; or

b) 25% if taken as an annual pension.

Option (b) may therefore seem preferable, but don’t forget that income tax is then charged on the pension (at 40%, the overall effective rate becomes 55%).

How much is the LTA?

The LTA is £1m. Legislation allows for CPI increases to be applied from April 2018 if the government so wishes.

How do I assess myself against the LTA?

Assessment against the LTA is made at the point of accessing benefits. (This is referred to as a Benefit Crystallisation Event or BCE and usually occurs at retirement. The legislation includes a full list of BCEs.) Upon a BCE, the scheme administrator performs the LTA assessment. LTA assessment is cumulative if you have more than one pension. Individuals should understand their position against the LTA to aid their planning.

For a DC scheme, measurement against the LTA is simply the value of the accessed amount of the fund.

For a DB Scheme, measurement against the LTA is calculated as follows:

(20 x initial annual pension at retirement) plus any lump sum

E.g. retiring on a DB pension of £20,000 p.a. with a lump sum of £100,000 uses up £500,000 (50%) of the £1m LTA.

If you also accessed DC pension worth £100,000 at the same time, then a total of 60% of the LTA would be used up.

How is the LTA charge paid?

The LTA tax charge is paid directly by the scheme. It is the responsibility of the individual to make appropriate declarations so that the correct tax is paid.

How much can I take as tax free cash at retirement?

Tax free cash lump sums can be taken at retirement from each of your schemes up to 25% of the value of your saving in that scheme (valued in the same way as used for LTA assessment). This is usually limited to 25% of the LTA.

LTA protection mechanisms

With the introduction of the LTA and at every reduction in the LTA since, the government provided transitional protection mechanisms for individuals nearing retirement who had targeted the previous limits.

These protections are not considered in detail here, except to note two things. Firstly, at the time of writing, two protections remain available. These are:

- Individual Protection 2016 (no registration deadline)

- Fixed Protection 2016 (no registration deadline – although all pension saving must have been ceased on or before 5 April 2016)

Secondly, certain protections (Enhanced Protection and Fixed Protections) require that all pension saving must have ceased at the effective protection date. Care is needed not to lose these Enhanced or Fixed protections as significant value can be at stake. Automatic enrolment and provision of life cover by your employer may inadvertently put these protections at risk; individuals will need to opt out of automatic enrolment to retain these protections.

Is exceeding the allowances a bad idea?

Exceeding the allowances leads to additional tax charges on top of income tax. This may mean being taxed twice or even thrice on some pension saving. The effective rates may be up to 75%. If you are caught in the AA Taper zone, the effective rates could be higher still.

The natural reaction is to avoid such high taxation. However, the effective rates do not take into account the circumstances nor the timing of these charges and the ultimate value of the resulting pension. Two examples illustrate this:

- An individual in a final salary DB scheme is promoted and has a large salary increase. This increased salary translates to a large ‘one-off’ AA charge. If, following the promotion, the individual does not expect to have such significant salary increases in future, the AA charge may be a one-off. Although the charge may seem significant at the time, the value of the higher benefit payable from the scheme may far exceed the AA charge payable.

- In the time between making DC contributions and/or accruing DB pension, pension savings grow in value in the tax free pension scheme ‘investment wrapper’. Pension saving made now may ultimately go over the LTA, triggering the LTA charge when accessed. This may not be for 20 years or more; tax free growth over that period may more than offset the additional charge, providing a better outcome compared with other forms of investment.

Individuals should consider their own positions carefully. Factors to consider will include the likely returns on alternative investments and their tax treatment, when the proceeds may be accessed, how long individuals expect to live and estate planning.

Importantly, in occupational schemes, individuals benefit from a contribution made by their employer. If no alternative to pension saving is offered, even though individuals may exceed the allowances and experience the higher effective rates of tax, they may achieve a better outcome by remaining in the scheme.

What does the future hold for tax relief on pensions?

This is always a hot topic before any budget statement. In the current low gilt yield environment the problem of the ‘one-size-fits-all approach’ is exacerbated. Consider the following:

- In a DB Scheme, a 55 year old retiring on an inflation-linked pension of £50,000 p.a. (and a spouse’s pension on death) remains within the LTA.

- To provide the same pension to that individual from a DC Scheme may require a fund of circa £3m presently.

Putting this aside, we consider below the potential future of a number of the elements of the current system:

- The AA: The direction of travel has been downwards. There have been calls for the standard AA to be lowered to the national average income, circa £28,000. For the average person even this may be seen as very high; it would still be significantly more than the full Automatic Enrolment contribution requirements.

- The LTA: The direction of travel has been downwards. The potential of CPI increases from April 2018 may suggest that we have reached the bottom. However, continued reduction of the AA makes it increasingly unlikely that individuals will ever reach the LTA. There are some calls therefore to abolish the LTA.

- The ‘tax free cash lump sum’: ‘Tax free cash’ maybe a misnomer; the legislation calls it the ‘Pension Commencement Lump Sum’ which is taxed at a rate of 0%. The mechanics to increase this tax rate may therefore be easy but the government may find it politically difficult to levy a tax on such a popular benefit. The Centre for Policy Studies have estimated that scrapping tax free cash could save c£4.5bn p.a. and this figure could rise with more people saving for pension through Automatic Enrolment.

- The rate of tax relief: There have been calls to restrict the actual rate of relief to one rate for everybody.

- EET or TEE? The previous Chancellor consulted upon whether upfront tax relief on pension saving should be removed, with the resulting benefits being tax free when accessed. However there was widespread support for retaining the current system, as changes could put at risk automatic enrolment and it was decided that it should be retained.

These issues, along with the challenges of an ageing population may well mean further and perhaps radical changes are required.