Seeing the full picture

Share this article

Wendy Nicholls and Nye Williams explain why transfer pricing documentation is more important than ever

Key Points

What is the issue?

How has BEPS increased the amount of thought everyone has to put into their TP reporting? Now that we have updated OECD Transfer Pricing Guidelines setting out clearly a three-tiered transfer pricing documentation approach, one would imagine the burden has reduced, but this is not the case.

What does it mean to me?

A centralised approach is often the best starting point for taxpayers. A risk-based approach to TP documentation, including a rolling programme of updates, can be planned in line with the size and complexity of operations in key territories.

What can I take away?

Groups have to be more vigilant than ever to set out their case in such a way as to demonstrate compliance and avoid double taxation.

Introduction

Base erosion and profit shifting (BEPS) refers to tax avoidance strategies that exploit gaps and mismatches in international tax rules to artificially shift profits to low or no-tax locations. The OECD and G20 BEPS package includes 15 Actions that aim to equip governments with the domestic and international framework and instruments needed to tackle BEPS. The Inclusive Framework was created to allow interested countries and jurisdictions to work with OECD and G20 members on this. To date 124 countries and jurisdictions have joined, committed to and collaborated on the BEPS package, expanding its reach far beyond the initial group. In areas like transfer pricing (TP) documentation, the BEPS project moved swiftly to identify and codify best practice, but as we shall see, did not impose a standardised solution, even as the countries involved all loudly professed their agreement.

This shifting landscape has led to multinational enterprises (MNEs), including the vast majority of international businesses who have never set out to avoid tax, increasing the amount of effort put into their TP. According to the November 2017 Thomson Reuters Global BEPS Survey Report, BEPS Action 13 on TP Documentation and Country-by-Country Reporting (CbCR) is the most concerning BEPS action for multinationals. Limited time and lack of internal resources are listed as key prohibitive factors.

Time and effort dedicated to TP has increased and requirements have also shifted. MNE’s pre-BEPS TP arrangements and documentation may quickly be out of date in the post-BEPS world, meaning TP documentation can no longer be relied upon for two or three years. Over a quarter of respondents to the survey indicated that their MNE has, or will likely, implement changes to their TP policies in light of BEPS.

In this article, we will explore this increased burden and changing landscape in the context of the three pillars of BEPS: transparency, substance and coherence. In doing so, we will provide you with some global practical experiences of CbCR, Master File and Local File implementation.

Transparency

Transparency is key to combatting BEPS and the exploitation of gaps and mismatches in tax rules, with tax authorities gaining greater insight into an MNE’s operations. CbCR has been the main tool here; for the first time, tax authorities have information to risk-assess TP and other BEPS-related issues. As CbCR is one of the four minimum standards of the BEPS Project, all members of the Inclusive Framework on BEPS have committed to implement these requirements, and to have their compliance reviewed and monitored by their peers. No escaping!

Businesses are required to meet the CbCR requirement by virtue of their global turnover (broadly, €750 million plus). Information on their global financials, headcounts, assets, tax and entity characterisation is available to tax authorities – only to be used for risk assessment, not for tax assessment. However, as the first reports were shared internationally in June, we await to see if countries respect this.

Tax authorities on both sides of an intercompany transaction are now able to view the financial results of all the group entities in the supply chain. Taxpayers need to be able to justify the returns made by both parties. One-sided testing is not enough (see Chapter I of the revised 2017 OECD Transfer Pricing Guidelines).

Under BEPS Action 13, CbCR is part of the three-tiered approach to TP documentation which arms tax authorities with greater insight into an MNE’s operations. In addition, the updated 2017 Guidelines recommend that MNEs prepare a group Master File and Local Country Files. The Master File is intended to be available to all tax authorities and thus is another aspect of the increased transparency required from MNEs.

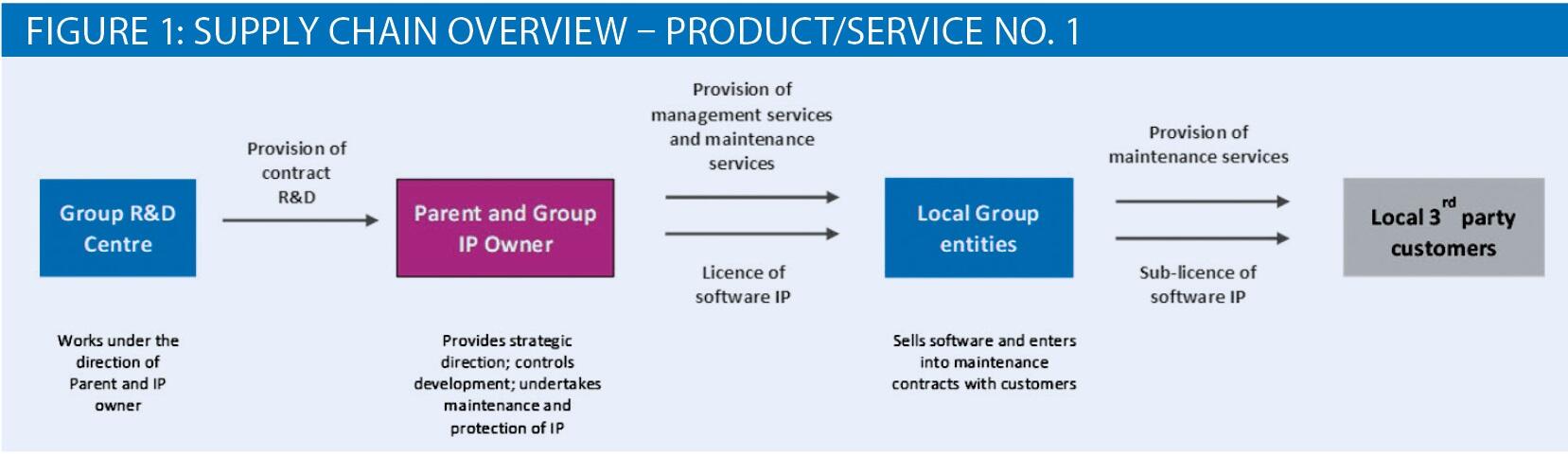

The Master File includes key information about the group’s global operations with a high-level overview of the group’s business operations alongside important information on its global TP policies in respect of intangibles and financing. One aspect of the Master File that some groups find challenging is describing their group’s supply chain for the largest five products and/or service offerings by turnover. In reality, this can be kept relatively simple and included pictorially within the Master File. Figure 1 provides an example of a supply chain in which an intangible property (IP) owner engages a group research and development (R&D) centre to perform development on software IP, and in turn on-licenses this software to local group entities.

Image

In contrast to the Master File, the Local Files should provide more detailed information and support for the arm’s length nature of the pricing of intercompany transactions with related parties in the relevant territory.

Substance

Profits should be recognised where value is created; in other words, where substance exists. MNEs must ensure that their significant people and control functions are aligned with value. Other additions to the Guidelines based on BEPS Actions (8-10) seek to ‘align transfer pricing outcomes with value creation’ and cover a number of topics, including intangibles.

Whilst MNE groups should have contracts to cover their internal transactions (as would be the case for transactions with third parties) and these will form the starting point of any analysis, the guidance requires us to probe beyond contractual allocations of functions, assets and risks in order to ensure the transfer pricing outcomes are in line with the economic activity conducted by group members. A key theme revolves around the concept that the return earned by both the legal owner of IP and by other group members is dependent on the functions each undertakes, assets used and risks assumed, and upon control of these functions by ‘significant people’.

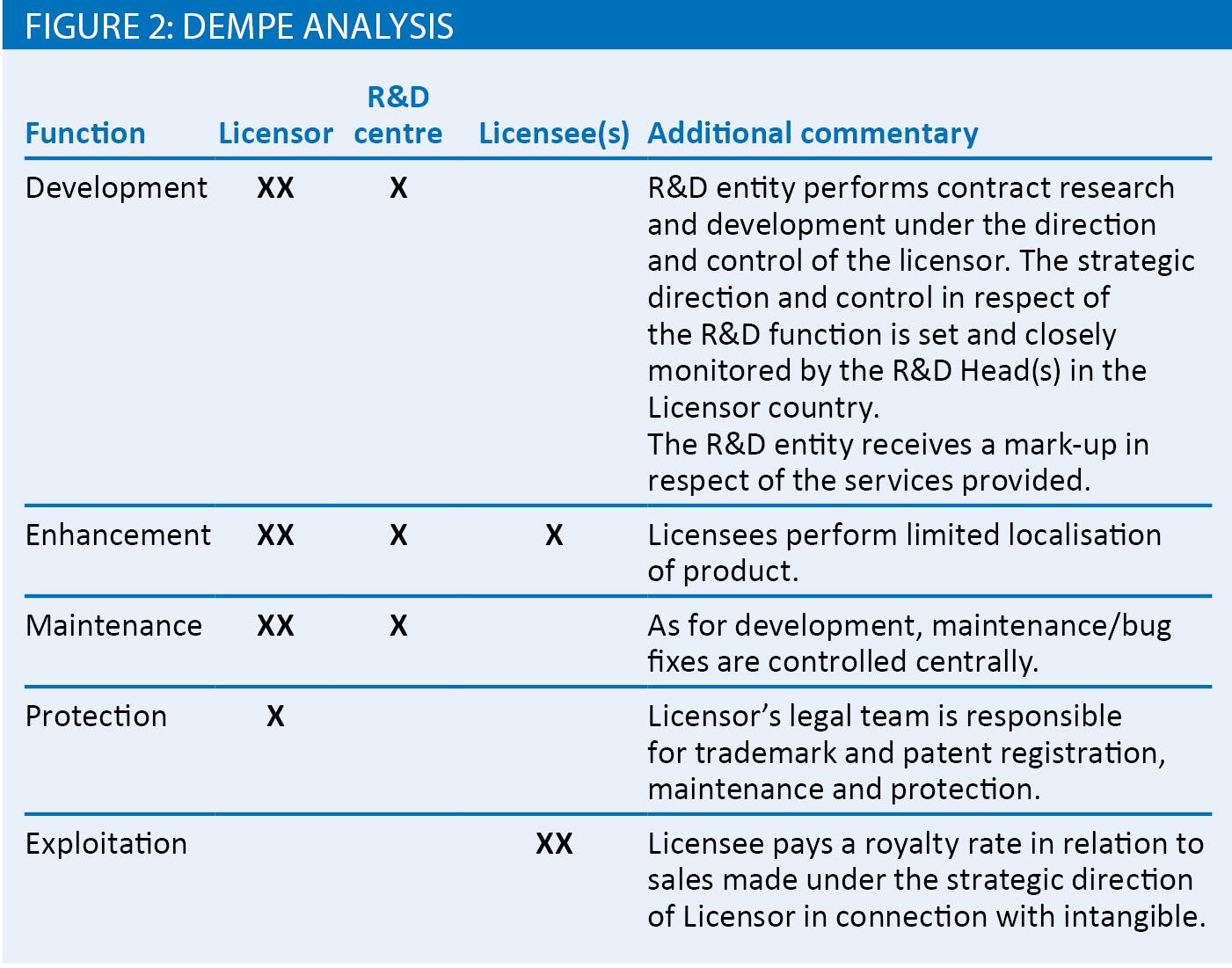

For taxpayers, this means performing a Development, Enhancement, Maintenance, Protection and Exploitation (DEMPE) analysis in respect of group intangibles and documenting this within their Master File. This analysis should identify which group members have the capability to manage economic risks and make decisions in relation to risk-bearing opportunities, and how to respond to and mitigate them. In addition, the IP analysis should determine which group members have the capability and capacity to control risk and bear the costs in the event the risk event materialises.

Whilst in theory the DEMPE analysis may seem straightforward, many taxpayers are unsure of the extent of the analysis required. How best can MNEs meet the requirements?

A functional analysis and supply chain detailing the key value-drivers of the business and significant people functions could be supplemented with a high-level intangibles section that outlines the key DEMPE functions. For example, a tick-box analysis as outlined in figure 2 can provide a high-level at-a-glance overview of group entities performing the DEMPE functions for the software transaction above, where the main development is performed in the R&D centre on behalf of the licensor and the product undergoes some localisation prior to sale in the licensees’ territories.

In this example the licensor (IP owner) controls the DEMPE functions and is likely to report much of the profit, or loss, arising therefrom.

Conversely, if in this case the TP policy results in the licensor getting a limited return and the licensee taking the lion’s share of profit or risk of loss, then there may be a misalignment, in which case the TP policy and model should be reviewed. In that event, no amount of documentation, or files generated by expensive software, will help; nor can they be assumed to give protection against potential penalties.

The classic mistake we see is people thinking TP documentation is a compliance exercise, based on getting things down on paper or into a template. When done properly, it has nothing to do with that. It is about aligning what is written with what is really going on. Businesses need to ask whether, on reading the document, their own commercial managers would recognise the business.

This work is not about producing voluminous write-ups or pages of calculations involving spurious weightings. It is about asking the right questions and standing back to see if one can demonstrate the alignment of substance and value. A lot of our work is about asking whether the documentation hangs neatly together with the reality on the ground. With tax authorities increasingly expecting to meet taxpayers themselves to check functional analyses, any disconnect between what is happening in practice and what is said in documentation will become clear very quickly.

Coherence

Although Country-by-Country reporting under BEPS Action 13 is a ‘minimum standard’ (red line), both the Master File and Local File are not. Therefore, whilst one of the pillars of BEPS was to increase coherence amongst global tax requirements, tax authorities and legislators have freedom to adopt the Local File and Master File as they deem fit. As a result, whilst countries have signed up to the OECD drafts and templates, a number then immediately departed from the consensus by requiring their own local variations. Indeed, even the introduction of CbCR has not been universally, consistently applied and some practical issues are now coming to light as the second round of filing is upon us.

Some tax authorities have used the BEPS package as an opportunity to amend and implement different or additional local rules in respect of TP documentation. This has not been limited to non-OECD members, with some of the European OECD countries like Italy and Spain also putting in additional requirements. The US has not adopted any of the BEPS 13 measures except for the mandatory CbCR in their Form 8975. However, it is many of the very large non-OECD economies who, having participated so enthusiastically in the BEPS project, later dramatically departed from the recommendations (India and China for example). On the plus side, Brazil, currently a jurisdiction that raises some major documentation challenges and tax leakage with regards to transfer pricing, is considering adopting the Action 13 format.

Far from seeing a reduction in the incidence of double taxation, there are more enquiries and challenges in obtaining relief from double taxation post BEPS. The OECD’s recently released 2017 Mutual Agreement Procedure (MAP) statistics, covering 85 jurisdictions and almost all worldwide MAP cases, highlight this issue, with new TP cases up approximately 25% in just one year.

However, we do not recommend producing documentation covering every transaction and every territory to ‘litigation standard’ as this would be disproportionately time consuming and expensive. MNE tax directors and CFOs should still take an informed, cost-benefit decision on the extent of their TP documentation.

Common fallacies

We often see groups taking a bottom-up rather than top down approach, and producing detailed documentation for the ‘squeaky wheel’ (i.e. the small subsidiary with an aggressive local tax authority). Other groups make the mistake of spending their budget on countless local benchmarking exercises when a regional approach including similar economies would suffice. Also, the OECD supports a roll-forward approach with brand new benchmarking only needed every three years, provided no major changes have occurred.

Another trap for the unwary is failing to consider the interaction of three-tiered BEPS 13 documentation and local compliance filing requirements. In some local territories, the TP information disclosed in tax returns can far exceed (in quantity and detail) that which is included in the BEPS 13 documentation. At a practical level, these requirements are extremely onerous and can potentially be used against taxpayers by tax authorities. The information included within a tax return is digitally submitted and so can easily be analysed by tax authorities to identify outliers – an immediate tax investigation flag! Therefore, it is key for MNEs to ensure that their local filings and transfer pricing documentation are aligned and coherent – but this is not always straightforward. Many groups are not even aware of the details filed in local language on their behalf. Many would be surprised to learn, for example, that Japan requires the gross margins of related counterparties, and the Chinese authorities even require details of the effective tax rate of related counterparties.

A practical approach

A centralised approach is often the best starting point for taxpayers.

As we’ve heard, local tax authorities may require additional, or different information, to that outlined in the OECD’s recommended contents, and local entities may have features that differ from the top-down view from ‘head office’. These issues will only be found by doing some work at local level. Nowadays, however, it is unrealistic to prepare documentation that will avoid any possibility of challenge in any territory.

A risk-based approach to TP documentation, including a rolling programme of updates, can be planned in line with the size and complexity of operations in key territories. Many MNEs take a cost-benefit approach, ensuring that all TP documentation provides a robust but high-level overview of operations. Their documentation is aimed towards penalty protection, rather than defence against a potential wide ranging tax audit. As a follow-up and upon any further scrutiny, additional information can be provided. However, the well prepared group which has ensured that its TP model is aligned with value creation and has implemented its policy correctly, is in a perfect position to prevail.