The spousal bypass trust

Share this article

Sam Newton considers the tax benefits of the use of discretionary trusts for spouses

Key Points

What is the issue?

An individual can place their pension lump sum death benefits into a discretionary trust, allowing the spouse to benefit without these benefits forming part of the survivor’s estate on death.

What does it mean to me?

Provided they are distributed from the pension scheme within two years of the member’s death, then any benefits should not normally be subject to inheritance tax.

What can I take away?

Using bypass trusts can therefore be an effective way to provide spousal benefits while mitigating tax on the estate.

The introduction of Pension Freedoms brought about the widening of the range of potential beneficiaries on death in the form of the beneficiaries’ drawdown, and the removal of any cap on income withdrawals and beneficial tax status. These benefits apply to defined contribution pension schemes; this article does not cover defined benefit schemes.

Using a discretionary trust for the death benefit (sometimes called a bypass trust) has some valuable characteristics, such as:

- providing capital protection, in terms of safeguarding benefits from potential divorce or the bankruptcy of a beneficiary;

- removing the monies from being counted by the local authority in any assessment for long-term care provision for a beneficiary; and

- an effective tax-planning tool.

What is a spousal bypass trust?

An individual can place their pension lump sum death benefits into a discretionary trust, allowing the spouse to benefit without these benefits forming part of the survivor’s estate on death. Provided they are distributed from the pension scheme within two years of the member’s death, then any benefits should not normally be subject to inheritance tax (IHT).

Once in trust, the trustees can make income and/or capital payments to the spouse or other beneficiaries, as well as making loans available to the spouse. These would be repayable out of the spouse’s estate on death, thus reducing the value of their estate for IHT purposes (i.e. treated as a debt on their estate).

The trust will be subject to the relevant property regime, which means it would be subject to 10 yearly periodic charges and proportionate exit charges on capital leaving the trust. The structure of the pension scheme, including any transfers-in to that scheme prior to placement in the trust, can potentially affect the timing and calculation of any charges.

How is a trust set up?

An individual can set up a trust in one of two ways:

- Create a separate pilot trust (a discretionary trust established in advance with minimal assets, intended to receive the death benefit).

- Assign the right to the death benefits under an integrated personal trust.

These types of trust can be set up during the individual’s lifetime or can be created by the deceased member’s will.

How are any pension lump sum death benefits paid into the trust?

The individual can either (depending on the type of pension scheme and scheme rules):

- draft a letter or complete a nomination of beneficiaries form letting the pension scheme trustees know of their intention for the lump sum death benefit to be paid to a separate trust; or

- give a binding nomination to the trustees (directing benefits to be paid into a separate trust).

An ‘expression of wish’ (or nomination of beneficiaries)

For pension schemes with discretionary disposal, an expression of wish form (also known as a nomination of beneficiaries form) gives the member an opportunity to set out their intentions in terms of whom they would like the benefits to be left with. However, this form is only meant as an indication of the deceased’s intentions. While the pension scheme trustees (or scheme administrator) will normally take this form into consideration when distributing benefits, they are not compelled to act on it.

One of the arguments in favour of setting up a separate trust is to ensure that the deceased’s chosen beneficiaries are catered for on their death. However, the decision as to whether any lump sum death benefit may be paid into that trust will still end up being down to the discretion of the existing pension scheme trustees (or scheme administrator).

Making a binding nomination

It’s also worth checking that the member hasn’t given the trustees or scheme administrator a written direction to make payment to a named individual, as this is a binding nomination and is not the same as an expression of wishes.

The member can also create a trust during their lifetime and assign the right to any death benefits into it, where on death any lump sum death benefits would be held by the deceased’s chosen trustees. One of the potential risks with making a binding nomination is that it can create a general power of disposal. Providing it doesn’t, then there should not be any IHT implications.

Does the type of scheme matter?

The legal structure of the pension scheme can also make a difference in terms of how any death benefit is paid. For example, most occupational defined contribution schemes, SIPPs and personal pensions are set up so that the scheme has discretionary disposal. This means the pension scheme trustees or scheme administrator normally has the ultimate discretion in who will receive any lump sum death benefit.

Some older style contracts, such as retirement annuity contracts and s 32 contracts, are set up without discretionary disposal, where any lump sum death benefit must either be paid to the deceased’s estate or where this had been assigned to trust (for example, under an integrated trust) paid to that trust.

Why bother with a discretionary trust?

In the bypass trust, the member’s chosen trustees maintain control over which beneficiaries will benefit, and when. This is in contrast to paying a lump sum directly to a beneficiary or setting up a beneficiary’s drawdown, where once the benefit is paid out to the relevant beneficiaries, they are free to do with it as they please and determine who any future beneficiary will be.

Consider the scenario where a member has children from a previous marriage. In the first instance, they would like their current spouse to benefit but want any remaining benefit to revert back to their children upon their spouse’s death. If a lump sum or beneficiary’s drawdown was provided for an existing spouse, then this wouldn’t be possible. If the spouse inherited the lump sum payment, they could do with this as they please; likewise, if the spouse inherited the beneficiary’s drawdown, they would be the owner of the plan and, in addition to having the flexibility to draw down the entire fund, would also have the flexibility to leave any remaining fund to anyone they choose, possibly their own children from another marriage. The member could express an intention for their children to benefit in addition to an existing spouse on an expression of wish form, but if the intention is for the spouse to receive the full benefit, and the trustees make that decision, then it’s too late for the children to benefit after that spouse dies.

This is just one example (and there are many others) of why an individual may seek to place any death benefit into a spousal bypass trust on death. The member can choose their own trustees, as well as the potential beneficiaries. In the scenario above, the trust could provide benefits to both a current spouse and the children from a previous marriage.

The benefits

The benefits of setting up a discretionary trust include the following:

- It creates a greater amount of control in terms of how any lump sum death benefit monies are distributed. It allows the member to select their own trustees, who would be familiar with their intentions and would be able to distribute the monies to those beneficiaries, as and when they require it; whereas the pension scheme trustees of any plan may not fully appreciate the deceased’s intentions or potential issues – for example, those with beneficiaries who may be physically or mentally incapacitated.

- It can create greater flexibility on death, in that trustees can pay capital or income to multiple beneficiaries, which may be more in line with the deceased’s intentions. They can also pay any monies out in stages as opposed to a large lump sum – for example, any beneficiary who may not have enough financial experience to handle a large sum of money.

- It enables the trust to loan monies to beneficiaries which may be repaid out of their estate on death, therefore avoiding any potential IHT.

Tax aspects and implications

The spousal bypass trust, some might argue, is no longer relevant in terms of tax efficiency, particularly where the member dies on or after their 75 th birthday. So have bypass trusts any value following pension freedoms?

Any pension lump sum death benefit would be taxed at 45% before being paid into a spousal bypass trust. Compare this with a beneficiary’s drawdown, where the benefits would be taxable at their marginal rates of income tax, but can be managed in a tax-efficient manner. Due to the fact the tax status is based on the age at death of the last owner of the plan, benefits can even potentially fall back into being tax-free on a successor (if the beneficiary were to die prior to age 75).

So, is the tax treatment where the member dies on or after age 75 such an issue that it outweighs the potential benefits of using a spousal bypass trust? Let’s examine the difference in tax treatment on any lump sum death benefits being paid into a bypass trust.

Taxation of lump sum death benefits before payment into the bypass trust

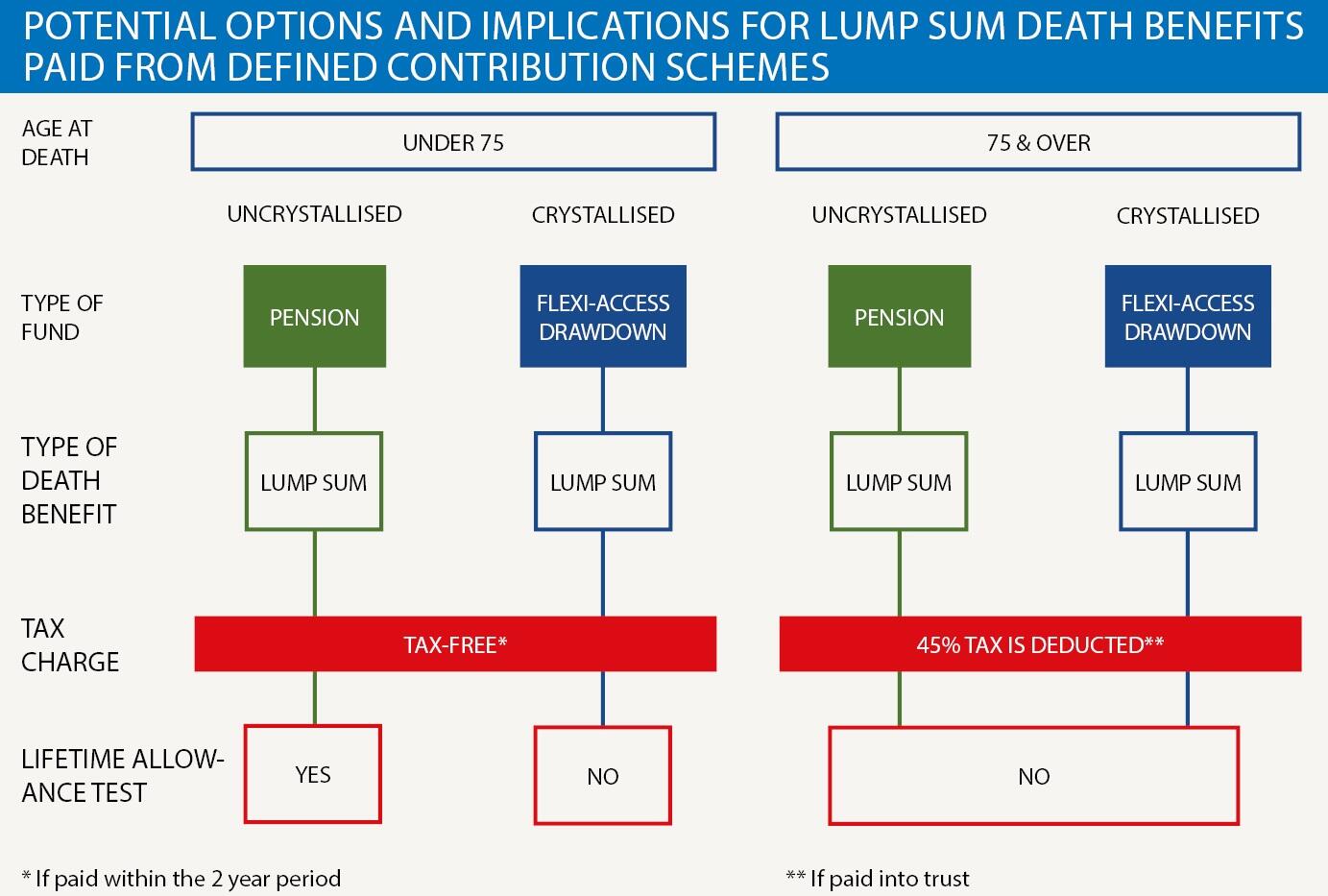

Any lump sum paid into the trust on death prior to age 75 can be paid into the trust free of income tax, but any lump sum paid on death on or after age 75 would incur a 45% income tax charge (so it is still the old lump sum death benefit tax charge of 45%, which applies to payments other than individuals, for example, a trustee).

However, where this is subsequently paid out to a beneficiary, they are able to claim a tax credit for the difference in the tax paid between the trust rate and their marginal tax rate. The diagram illustrates the potential options and tax implications for lump sum death benefits paid from defined contribution (DC) schemes.

Taxation of lump sum death benefits inside the bypass trust

Under the IHT Act 1984 s 58(1)(d), registered pension schemes are not classed as relevant property for IHT purposes. However, if a discretionary trust is set up which receives any lump sum death benefit originating from a registered pension scheme, then they will fall under the relevant property regime and will potentially be subject to periodic and exit charges.

Periodic charges

Where a lump sum death benefit is paid from a pension scheme into a trust, the timing of the periodic charge, in terms of the 10 yearly period, will depend on whether or not the scheme has discretionary disposal. So it is possible for a lump sum death benefit to be treated as a separate settlement for IHT.

What type of lump sum death benefit is treated as a separate settlement?

- For pension schemes that have discretionary disposal, for example trust based schemes, but also SIPPs and some personal pensions, where the trustee or scheme administrator has ultimate discretion these will be treated as a separate settlement.

- Therefore, the periodic charge calculation is based on the date the individual first became a member of the pension scheme and not the date the lump sum death benefit monies entered the trust. The charge will apply from the first 10 yearly anniversary of the date the individual joined the original pension scheme that falls after the lump sum death benefit has been paid to the trust.

What if the pension scheme has no discretionary disposal?

For schemes without discretionary disposal, for example some personal pensions and older style contracts such as retirement annuity contracts and s 32 buy out plans, their periodic charge calculation will be based on the date the lump sum death benefit monies are paid into the pilot trust (or the date they were assigned to the integrated personal trust).

Therefore, this will be the date used to determine the first 10 yearly anniversary to which any periodic charge calculation will be based.

Does the previous pension transfer history matter?

The tax position becomes more complicated where the deceased had a number of pensions and consolidated them into one pension prior to death, for example, transferring them into a self-invested personal pension (SIPP).

When lump sum death benefits are subsequently paid to a bypass trust originating from one pension arrangement but where there had been previous transfers-in to that pension (prior to the member’s death), this can result in the receiving trust being treated as a number of separate settlements for IHT purposes. Each will have its own 10 yearly anniversary and IHT nil rate band for the periodic and exit charges.

For example, if a member transfers their pension from one trust-based pension scheme to a SIPP, then those benefits will still be treated as in the original settlement for IHT. If further contributions were then made to the SIPP, these would in effect form part of the second settlement for IHT purposes.

Does paying lump sum death benefits into a pilot trust from more than one pension scheme matter?

Where an individual had set up a trust to receive one or more lump sum death benefit payments on their death, each lump sum may be treated as a separate settlement for IHT. Again, this depends on whether or not it originated from a registered pension scheme that had discretionary disposal.

It’s important to note that when calculating periodic and exit charges, each settlement may have a different 10 yearly anniversary date and therefore benefit from its own nil rate band.

Using bypass trusts can therefore be an effective way to provide spousal benefits while mitigating IHT on the estate. They can also be a useful way to keep some form of control around who receives any benefit. However, lump sum pension benefits within trusts can be subject to periodic and exit charges. So it is important to understand the structures of how more than one pension arrangement enters a trust (and potentially the pension transfer history) prior to payment into a bypass trust as this can impact the timing when calculating periodic charges.