A sustainable future: the role of environmental tax strategies

Share this article

As the scale of the challenge needed to tackle climate change reaches unprecedented heights, we share a personal view on the role that tax strategies could play in building a sustainable future.

Key Points

What is the issue?

Part of the transformation required by the need to build a sustainable future leads us to ask some fundamental and difficult questions about the role of business and tax in society and the very nature of our tax systems.

What does it mean to me?

In the UK and EU, the majority of tax revenues come from labour taxes, whereas only about 6% come from environmental taxes.

What can I take away?

Tax functions will need to learn a new sustainability lexicon to enable tax’s essential role in supporting environmental mitigation and adaptation efforts.

In my experience working in the tax functions of FTSE 100 companies, in professional service firms and speaking to other tax professionals, the average tax function has tended not to dwell on the existential questions posed by our need to build a sustainable future. However, I believe we are all starting to recognise the scale of the transformation required of us as a society. Part of that transformation requires us to ask some fundamental and difficult questions about the role of business and tax in society.

We must put the scale of the challenge in perspective. During Covid lockdowns, when personal freedoms were severely curtailed, CO2 emissions fell only by about 5.5%. Moreover, NASA reported that atmospheric levels of CO2 actually continued to grow that year, not fall. Yet to reach Net Zero by 2050, we need to reduce global emissions by about 7% every year between now and then. Just think about the scale of disruption needed to deliver this existential goal.

A tax strategy shift

CEOs are increasingly factoring environmental, social and corporate governance (ESG) into their strategic decision making. In a recent outlook survey, over 80% of CEOs ranked ESG factors as more important even than revenue growth, return on capital or costs. Perhaps this is not surprising, as they will increasingly be held to account for their NetZero commitments and science-based targets. Every business will need a new holistic strategy infused throughout with sustainability. This strategy will shift capital to catalyse business model transformation at a pace and scale not seen before.

These issues now need to feature in tax teams’ thinking. Tax functions will need to learn a new sustainability lexicon and will need to be mindful of over 3,000 environmental taxes and exemptions that that have been introduced globally – with no doubt many to come.

I will make the case for tax to be at the centre of efforts to meet the existential challenges that come from building a sustainable future. Understanding how a business fits within the socio‑economic landscape will help tax functions provide essential support to the adaptation and mitigation efforts needed.

The Great Acceleration

The Great Acceleration covers the complex set of human-driven changes which have intensified dramatically since 1950, leading scientists to consider that earth has left the uniquely stable geological Holocene era, which lasted for around 12,000 years. It can be illustrated through the research of the International Geosphere-Biosphere Programme showing both Socio-economic and Earth System trends (see tinyurl.com/28jp972c).

Looked at another way, Earth Overshoot Day – the date in the year when our collective demands on the planet exceed its biocapacity to replenish itself – has been getting earlier each year. In 2023, Earth Overshoot Day is 2 August – which means that as you read this, as a species we have already extracted more this year than the planet can sustain.

Climate scientists have tried to map this territory across nine planetary boundaries, which define the environmental limits of the critical earth systems within which humanity can safely live. By 2015, scientists had established that four of these had already been breached: climate change, biodiversity loss, land-system change and biogeochemical flows (nitrogen and phosphorus). In 2022, the boundary for novel entities (pollutants such as plastics and chemicals) was also found to be outside the safe zone. The boundaries for freshwater, ocean acidification and ozone levels are still within safe operating limits, while the boundary for atmospheric aerosols has not yet been quantified. Human actions in the next few years could have lasting impacts on the planet for centuries if not millennia.

Humanity can still make a positive difference on a planetary scale, with a plan based on the 17 Sustainable Development Goals published by the United Nations in 2015 and developed with input from governments, business, academia and non-profit organisations. The Sustainable Development Goals seek a sustainable future by ending poverty, fighting inequality and tackling climate change. They define the agenda for inclusive economic growth to 2030.

The role of the tax system

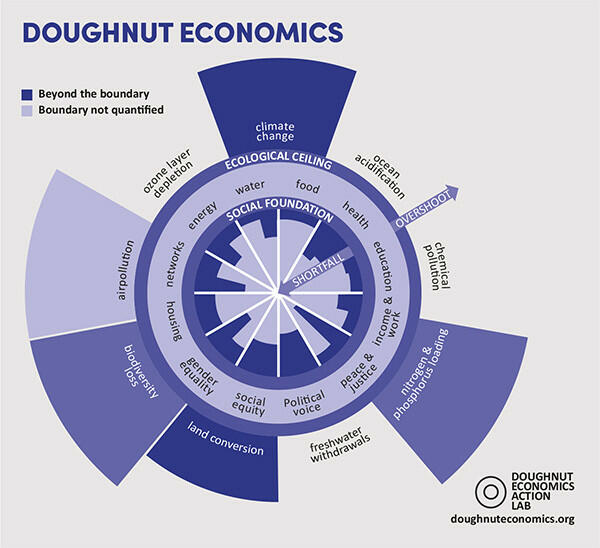

It is in the interaction between the 17 Sustainable Development Goals and the planetary boundaries that tax’s role becomes clear. Economist Kate Raworth describes this interaction as part of Doughnut Economics. The doughnut consists of two rings – a social foundation (below which people will fall short of life’s essentials) and an ecological ceiling (beyond which the planetary boundaries are breached). Between these two boundaries lies the doughnut-shaped space in which humanity can thrive.

Tax has a key role to play at both edges of the doughnut. It is a major contributor to our global social foundation through redistribution. It also catalyses investment and innovation, which supports the regeneration of earth systems by driving behavioural change towards clean technologies and disincentivising polluting activities.

There are ten years of investment incentives offered by the US Inflation Reduction Act. $369 billion of tax credits are available for ‘green investments’. Hundreds of companies have announced additional US investments since the law passed in 2022.

The EU – which wants to be the first carbon-neutral continent – is already responding through its Temporary Crisis and Transition State aid Framework (TCTF), which is aimed at incentivising and retaining clean tech investments in Europe. The Framework will operate until the end of 2025 and loosens EU state aid rules to allow EU states to offer ‘matching aid’ to companies where it is likely they would otherwise relocate outside the EU due to foreign subsidies.

EY tracks nearly 2,000 sustainable incentives globally – encouraging a mix of mitigation and innovation. This number is likely to increase as the OECD’s Pillar Two initiative will restrict countries’ ability to compete through low headline tax rates. Above-the-line incentives that are qualifying refundable tax credits (QRTCs) will have limited dilutive impact on GloBE (global anti-base erosion) rates and will therefore become increasingly effective levers for countries to encourage inward investment.

The levels of investment needed are colossal, with some estimates of around $200 trillion in capital investment needed by 2050 just for Net Zero. This equates to around $7 trillion per year. (As a marker, during 2020 central banks increased their balance sheets by about $7 trillion globally to support their economies through Covid).

Accounting for investment

Huge upfront capital investments with long-term paybacks do not play well to the net present values (NPVs) of investment cases. Many green investment cases may be uncompetitive or marginal on a purely financial basis – even with tax incentives. This has led to calls to overlay qualitative non-financial measures, but if the financials are unattractive, short-term pressures will usually militate against qualitative overrides.

Discount rates are essential to arriving at NPVs. They are used to express future financial costs and benefits at their present value. A discount rate of 2% means that a project which would yield a benefit to society of $1 million in 50 years has a present value of about $371,500 today. At a discount rate of 5%, the present value would be around $87,000.

In effect, this means when evaluating the project’s benefits, Person A alive today is treated more favourably than Person B living 50 years from now. In fact, Person A’s needs today are treated as 2.7 times as valuable (at a 2% discount rate), or 11.5 times as valuable (at a 5% discount rate) as those of Person B living in the future. To put it more starkly, is a human life today really worth 11.5 lives of humans living 50 years from now?

So some investors are considering whether to use lower discount factors in their financial models to try to make some adjustments for intergenerational equity. Others argue that we should be adopting a different paradigm entirely – one that embodies seventh-generation decision making; i.e. decisions based on their impact 200 years or more into the future. Is now the time for humankind to think of itself as ‘stewards of creation’ for our descendants?

A question of tax

Whether or not such a paradigm shift is likely, there are still questions regarding what should be taxed in transitioning to a sustainable, thriving society. In the EU, the majority of tax revenues come from labour taxes, whereas only about 6% come from environmental taxes. At a time when generative AI is predicted to automate huge swathes of the labour market, is it sustainable long-term tax policy to incentivise investments in automation at the expense of employment? Femke Groothuis of Ex’Tax, in a report supported with contributions from all the Big Four accounting firms, has advocated for a Tax Shift. The basic principle is to lower the tax burden on labour and increase taxes on pollution and resource use. This approach is supported in the EU Green Deal which commits to ‘create the context for broad-based tax reforms … shifting the tax burden from labour to pollution’.

This thinking is being put into practice. We are seeing more taxes on pollution as packaging taxes and recycling levies proliferate. The EU Carbon Border Adjustment Mechanism (CBAM) comes into effect on 1 October 2023, and there are now around 70 national or sub-national jurisdictions that are pricing or taxing carbon – with many more regimes anticipated.

I will explore these regimes, other specific environmental taxes and the circular activities that the Tax Shift seeks to encourage in future articles.

The author’s views are his own and not necessarily representative of those of EY.