Tackling HMRC’s customer service challenge: CIOT and ICAEW joint report

Share this article

In December, the CIOT and ICAEW launched their joint report addressing HMRC’s customer service challenge, setting out ten key recommendations for improvement.

Key Points

What is the issue?

In recent years, HMRC has struggled to meet its target levels of customer service. The numerous pressures have been well documented: increasing complexity driving up demand; reducing basic customer services before digitalisation has been fully delivered; and repeated calls for HMRC to do more with less. HMRC has been pursuing a digital first strategy since at least 2012 to try and resolve HMRC customer service issues.

What does it mean for me?

HMRC customer service, effective HMRC systems and tax agents each play a vital role in helping taxpayers to get their tax right. Poor customer service and digital services that do not work properly are resulting in agents having to continually call HMRC to try and resolve their client’s queries.

What can I take away?

The CIOT and ICAEW believe that there is an opportunity to work collaboratively with HMRC and ministers to improve and strengthen HMRC customer service. We welcome and value feedback from members to inform our work, including information on any pain points in digital services, gaps in digital services andsuggestions for improvements to HMRC customer services.

In 2023-24, the UK tax system demonstrated a remarkable level of voluntary compliance, with over 95% of the £843.4 billion collected by HMRC being paid without intervention. HMRC customer service plays a crucial part in achieving this.

But in recent years, HMRC has struggled to meet its target levels of customer service. The number of taxpayers and the complexity of their tax affairs are increasing and HMRC is under significant pressure to do more with less.

The CIOT and ICAEW continue to receive feedback from our members, and hear reports of significant dissatisfaction with HMRC’s performance. It is against this backdrop that we decided to gather an up-to-date and comprehensive dataset to capture a full range of members’ customer service experiences and help to identify whether poor experiences were isolated, one-off incidents or whether they highlighted much more systemic problems.

The overarching aim was for this project to be constructive – to use our findings to inform recommendations that could make meaningful improvements to HMRC customer service that would have mutual benefit for HMRC, taxpayers and agents.

About our project

Our joint six week study from 9 September to 18 October involved 31 agent firms recording contact attempts across HMRC phonelines and webchats, followed by two workshops. This included sole practitioner firms through to Big Four firms.

Participants recorded information such as waiting times, duration of call, whether their query was resolved and their overall satisfaction with HMRC services. 634 contact attempts were recorded during the six week study, with 530 connected to an HMRC adviser. Only 79 interactions with webchat were recorded; however, what become clear was that this was not a reflection of low demand for webchat services, but because the likelihood of getting through to an adviser was low.

From 7 October 2024, there were several changes announced to the Agent Dedicated Line. Our data gathering period covered the first two weeks of these changes, but our results showed minimal improvements during this period. However, this two week period does not enable us to draw any conclusions regarding the effectiveness of the Agent Dedicated Line changes.

Key findings:

- 88% of calls connected

- 49% of webchats connected

- Average wait time: 19 minutes

- Agent Dedicated Line wait time: 27 minutes

- Only 33% of connected contact attempts fully resolved

- Average satisfaction for webchats: 1.4 out of 5 (or 28%)

- Average satisfaction for phonelines: 2.8 out of 5 (56%)

- Estimated annual HMRC staff cost for handling progress chasing: £36 million

Why were agents calling HMRC?

It quickly became clear that a significant volume of contact attempts were being driven by HMRC. Progress chasing accounted for over a third of all calls, with agents spending approximately 31 minutes per call (which includes 19 minutes waiting on hold) to only achieve full resolution from such calls 15% of the time. We estimate that eliminating progress-chasing calls could result in a potential annual cost saving to HMRC of over £36 million.

At least 11% of interactions with HMRC were attempts to correct HMRC errors or request amendments to returns. This percentage could in fact be higher if participants had noted their reason for calling as progress chasing when they were in fact following up on correcting an HMRC error. Our data also highlights that the lack of availability or functionality of digital services is a key driver of agents having to call HMRC. We discuss digital services in more detail below. A relatively small number of contact attempts were to discuss technical or complex queries.

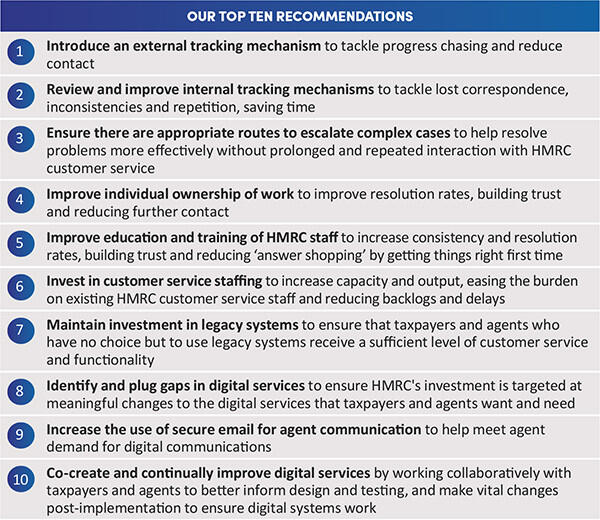

Recommendations 1, 2 and 3

1. Introduce an external tracking mechanism

2. Review and improve internal tracking mechanisms

3. Ensure there are appropriate routes to escalate complex cases

To help reduce the volume of progress chasing and provide clarity to agents and taxpayers, HMRC should introduce an external tracking mechanism. This should enable taxpayers and agents to track that HMRC has received their correspondence; identify which HMRC team the correspondence has been allocated to; and check progress, including being able to view status updates. Tracking systems should be included in the design of any new digital service. In the short term, until it is possible to have visibility of progress chasing across all taxes and digital services, the introduction of a targeted mechanism for progress chasing, such as a dedicated monitored inbox or digital form, should be implemented.

The report calls for HMRC to review its internal tracking systems and processes, and to share information on these with professional bodies. This would help professional bodies, agents and taxpayers to better understand HMRC’s current processes and possibly identify actions that could be taken to ensure that correspondence is delivered in a way that is more compatible with HMRC systems. It would also help to inform the design of any new external tracking system.

There will continue to be complex and problematic cases, and we recommend that HMRC introduces a service to help taxpayers and agents resolve them with a suitably experienced HMRC team. The current Agent Account Managers service may offer a blueprint of what this new service might look like.

Performance of phonelines and webchat

HMRC’s published target is to answer 85% of calls to its phonelines. Our data indicates that across all phonelines agents were connected to an HMRC adviser in 88% of contact attempts. Whilst it is pleasing to see that HMRC is now exceeding the 85% connection target, and agents were typically getting through to HMRC on their first attempt, connection on its own does not result in good customer service. This can be seen in the overall scores given for both phonelines and webchat.

Participants were asked to rate HMRC services from 0 to 5, with a score of 0 being the lowest rating and a score of 5 being the highest. Across all phonelines, the average score given was 2.8 out of 5.

Several factors impacted agent satisfaction with HMRC phonelines, including time spent on hold, being cut off during the call with HMRC, and resolution rates (including whether the agent needed to contact HMRC again).

While HMRC may currently be meeting its targets for connection rates, it has no published target for how quickly it should answer the phone. HMRC’s performance data for September 2024 suggested that the average wait time across phonelines was around 14 minutes. Our exercise, which had significant overlap with HMRC’s data period, revealed that agents spent on average 19 minutes on hold before being connected to an HMRC adviser, although many agents recorded call wait times of over 45 minutes. The time taken to reach an adviser on the Agent Dedicated Line averaged nearly 27 minutes.

Out of 555 attempts to phone HMRC, 45 (8%) were disconnected by HMRC before being answered and a further 23 calls (5% of connected calls) were cut off after being connected to an HMRC adviser. Participants reported being put on hold for extended periods or cut off during transfers between HMRC teams. When exploring this further through our workshops, participants provided examples of being cut off after querying the response provided by the HMRC adviser and where the HMRC adviser appeared to reach the end of their script and could offer no further support.

Resolution of queries was one of the most significant issues highlighted in our data. Across all connected calls, only 34% were recorded as being fully resolved, 24% were considered unresolved and 42% were partially resolved (i.e. the agent could progress the issue but not resolve it, or an agent calling about multiple issues had resolved one but not another).

Over the six week period, agents recorded just 79 attempts to contact HMRC via webchat – only 12% of the total contact attempts. However, this lower number of contact attempts was not necessarily an indicator of low demand. Participants told us they value the ability to save a transcript of a webchat conversation and to continue working whilst waiting to be connected. However, many have stopped trying to use webchat as they have come to expect that there will be no adviser available.

Of the 79 recorded attempts, fewer than half (39) of these webchat attempts were connected to an adviser. Of the 39 connected webchat attempts, only 8 (21%) were fully resolved and two-thirds of participants connected through webchat needed to contact HMRC again.

Recommendations 4, 5 and 6

4. Improve individual ownership of work

5. Improve education and training of HMRC staff

6. Invest in customer service staffing

Low resolution of queries is leading to low customer satisfaction and participants expressing their dread at dealing with HMRC.

Our participants told us that their positive experiences of HMRC customer service involved there being a personal touch, with an adviser taking ownership of a query. HMRC need to ensure that staff have the skills, infrastructure, autonomy and accountability to take ownership of their work and handle a matter from start to finish. This includes delivery on promised callbacks and working to, and meeting, agreed deadlines.

HMRC advisers being able to resolve queries within a reasonable timeframe helps to reduce HMRC backlogs, reduces costs for all, reduces contact volumes and promotes a positive relationship between HMRC, taxpayers and agents. HMRC needs to ensure that staff are equipped with the skills and resources to understand and answer the questions being asked.

The tax system is incredibly complex and not every HMRC customer service adviser can be expected to answer every question, so there needs to be clear avenues to escalate those queries beyond their expertise. There also needs to be a clear review process to ensure the quality of HMRC output – particularly when there are large numbers of new or inexperienced staff.

Digital services

HMRC has been pursuing a digital first strategy since at least 2012. Our participants told us that they support the development of HMRC digital services and are continually driving digital changes to their own businesses and how they interact with their clients.

During the six week period, agents spent on average 30 minutes to action relatively simple tasks such as changing a PAYE code, cancelling a filing requirement or reallocating a payment. There is a strong desire to do these type of activities online. However, most are unable to do so because digital services either do not meet their needs as they do not have the right functionality, are only available to taxpayers, or there are no digital services available at all.

Participants provided examples of difficult and prolonged interaction with HMRC because digital services were not working properly. This was then compounded by HMRC advisers saying they couldn’t help as there was now a digital service available for that request.

Agents are encountering errors, problems and inefficiencies with legacy systems, resulting in agents having to seek resolution via HMRC customer services. If HMRC does not continue to invest in and maintain legacy systems until there is a viable new alternative, this will increase the need for customer service contact. In recent years, investment seems to have focused on new systems and platforms at the expense of legacy systems – many of which are in dire need of improvement.

Recommendations 7, 8, 9 and 10

7. Maintain investment in legacy systems

8. Identify and plug gaps in digital services

9. Increase the use of secure email for agent communication

10. Co-create and continually improve digital services

We recognise the trade-off between creating new digital systems and investing in legacy systems. However, until there is an effective new digital system, it is vital to maintain investment in legacy systems to ensure their functionality, preserve an effective tax system and reduce avoidable contact with HMRC.

We asked participants what a good digital system looks like. There was unanimous agreement that a digital service should allow an agent to see and do everything that their client can. This should be a function from the outset – not built into the system at a later point in time. A digital system needs to work effectively – this is more than just design and implementation but involves a continual process of improvement. A new digital system should also have a built-in tracking mechanism.

Agents would also like to communicate with HMRC by email. Many spoke of postal correspondence being lost or attachments separated and sent to different teams within HMRC. Whilst being mindful of security concerns, the benefits of email for taxpayers, agents and HMRC are obvious.

The launch event and acknowledgements

The CIOT and ICAEW held a launch event on 11 December. CIOT’s President Charlotte Barbour opened the launch event, and we presented the key findings. Panel members from HMRC, the CIOT, ICAEW and two of the participating firms gave their perspectives and responded to attendees’ questions.

We would like to thank the participating firms who reported their interactions with HMRC over the six week period and participated in the workshops – the project could not have taken place without their efforts. The authors would also like to thank Richard Hawthorn (HMRC), Emily Nash (Litchfields Chartered Accountants) and Natalie Miller (Azets) for their participation in the panel event; and for the contributions from the CBI, Federation of Small Businesses and the CIOT’s Low Incomes Tax Reform Group.

Next steps

The CIOT and ICAEW are currently considering how we can build upon the report’s findings and discuss our recommendations with HMRC. We hope to continue working with HMRC to make meaningful improvements to HMRC’s customer service.

We welcome any discussion or feedback on improving HMRC customer service from members to help inform how we move forward with this collaborative work with HMRC.

We also look forward to working with HMRC on its digital transformation roadmap, which has a real opportunity to address some of the key frustrations that agents are facing and make meaningful change to the digital journey that HMRC, agents and taxpayers are all on.

The report can be read in full at: tinyurl.com/3hs328ey