The Tax Gap: small company compliance

Share this article

The 2023-24 Tax Gap figures highlight issues in the compliance yield for small companies.

HMRC published its estimate of the Tax Gap on 19 June 2025 – covering the 2023-24 tax year, with revisions of estimates for previous years (see tinyurl.com/5wxmky5c). The Tax Gap requires that HMRC statisticians and economists estimate the total tax due for the year; consider how much tax has been or will be brought in by HMRC’s compliance activities; and then seek to allocate the missing amounts by taxpayer class and type of behaviour. Despite being calculated a year in arrears, estimates abound. HMRC has sought to measure the Tax Gap for 20 years and during that time has refined significantly its understanding of how to estimate the missing cash.

The 2023-24 Tax Gap is estimated at 5.3% of the total tax due, at £46.8 billion. The tax gap for 2022-23 has been revised upwards from the originally estimated 4.8% (£39.8 billion) to 5.6% (£46.4 billion), due to improvements in data quality, the availability of more up-to-date information and methodology changes.

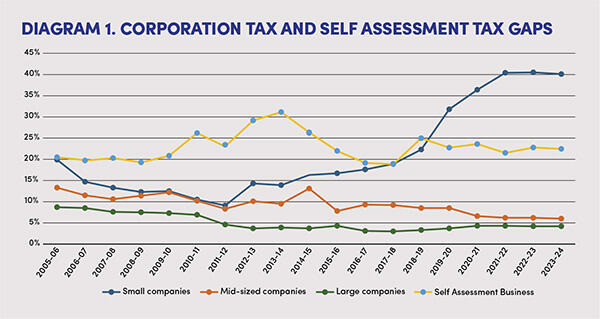

The small company tax gap

The headline this year is on the size of the small company tax gap, which has grown significantly over the last 12 years. Interestingly, the small business tax gap is due more to small companies, with a 40% tax gap, rather than to under-reported self-employment income (which at 23% is the largest component of the 12.5% Self Assessment tax gap). Small businesses are defined for 2023-24 as those with sales up to £10 million, and up to 20 employees.

The Tax Gap figures show that HMRC’s compliance yield over the last five years from small companies is a very small percentage of the gross tax gap – around 1% in 2022-24) (see tinyurl.com/mtn2t2sh). The compliance yield from medium sized companies is higher at 8% to 13% (and 13% in 2023-24). The compliance yield from large companies is much more significant at 44% to 55% (and 47% in 2023-24). No doubt this will be seen as demonstrating the value of HMRC’s customer compliance manager model. HMRC’s data from the random enquiry programme (the basis for estimating some of the tax gaps) shows that in 2021-22 53% of small companies had errors in their returns, with errors in 43% of Self Assessment business returns.

One of the more challenging parts of the report is estimating the different behaviours behind the Tax Gap. HMRC’s data attributes the largest (and growing) part to failure to take reasonable care (31%), with error the next most significant category (15%). Avoidance is the least significant category (1.5%) – and has been so for the last five years. Evasion continues to increase and is the third most important category. HMRC estimates that criminals managed to steal some £4 billion in 2023-24, through a combination of alcohol and tobacco smuggling and repayment fraud.

A global problem

The United States also produces a Tax Gap analysis. It isn’t as up to date as the UK but its 2022 analysis showed a much larger Tax Gap and, like the UK, a large small business gap (see tinyurl.com/3e3mkvn8). The estimated Total True Tax Liability for 2022 was $4,635 billion and, after enforced and other late payments of $90 billion, the tax not collected was $606 billion – a gap of 13.1%. Individual business income was $194 billion, with self-employment tax amounting to $71 billion and small company corporate tax $19 billion – meaning that small business accounted for about half the US tax gap.

In many ways, it is inevitable that the small business tax gap will be significant in most countries. Historically, it is the part of the tax system where only the taxpayer has the detailed information – unlike employment, for example. However, new business opportunities through platforms also mean new sources of third-party data for tax authorities, and this is being taken forward internationally.

HMRC’s recent Third Party Data consultation (see tinyurl.com/xn5xja6a) also highlighted the value of tax authorities receiving more data from processors on credit/debit card payments to suppliers.

Making Tax Digital for Income Tax is expected to reduce errors through requiring better record keeping, although some tax agents point out that this will include missing expenses, as well as missing income. The scale of the small business tax gap shows the need to focus on a wide range of approaches.

© Getty images