Tax University

Share this article

Naomi Wells provides guidance on the challenges faced by wealthy students studying in the UK

Key Points

What is the issue?

Some international students have substantial overseas wealth and need to understand their obligations in terms of submitting tax returns and paying tax in the UK.

What does it mean to me?

As advisers, we have an opportunity to work with these students and assist them with meeting their obligations. There may also be the possibility of tax planning to minimise their exposure to UK tax.

What can I take away?

Students who are non-UK resident under the relevant double tax agreement will need to make a claim for treaty relief. For students who are UK resident under the treaty, a remittance basis claim and remittance planning may be beneficial.

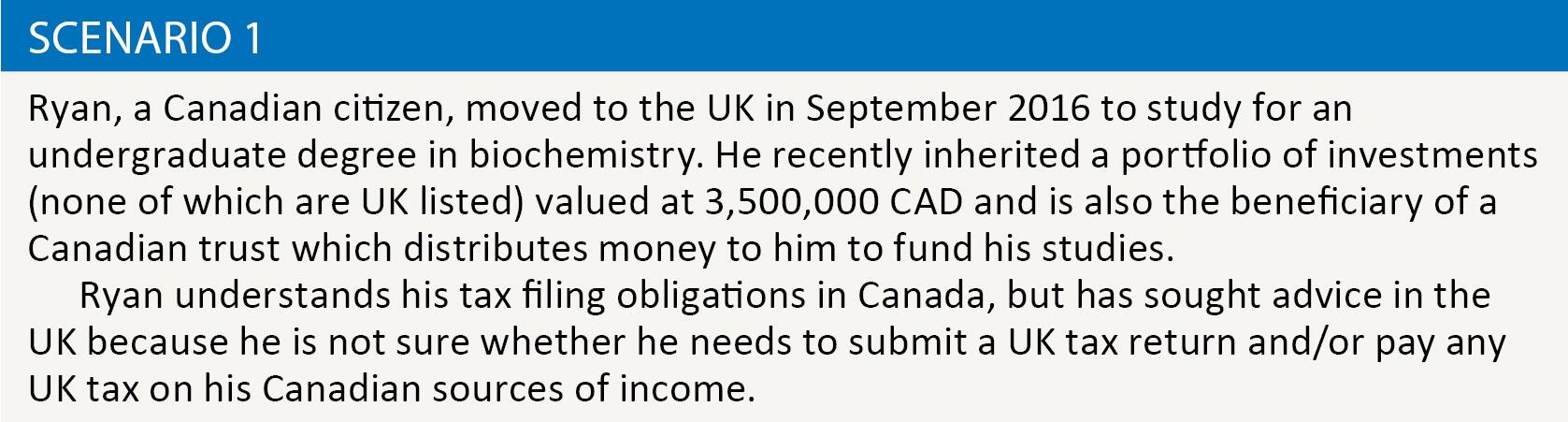

For many students, their interaction with the UK tax system is either non-existent, or limited to ensuring that the correct PAYE has been deducted from their basic earnings. However, for a minority of students, tax can be much more complicated (see scenario 1). There are a number of issues which wealthy international students such as Ryan need to consider.

UK tax residence

As a starting point, it is necessary to identify whether the foreign student is tax resident in the UK. For tax years from 2013/14 onwards, this is determined under the statutory residence test in FA 2013 Sch 45 and additional guidance can be found in HMRC’s guidance note RDR3. The tests are generally objective and depend on the student’s specific circumstances.

For many students, it is likely that they will be UK resident under the first automatic overseas test, by virtue of spending at least 183 days in the UK in the tax year. If this test is not met, provided that they do not meet any of the automatic overseas tests, a student may still fall to be treated as UK resident under the second automatic UK test (UK home) or the sufficient ties test. Assuming they are not working full-time, the third automatic UK test (full time work in the UK) should not be applicable.

Where a student is UK resident in the tax year of arrival, split year treatment may apply. For students who are not working full-time in the UK, Case 8, ‘Starting to have a home in the UK’ is the most likely to be relevant. Under this case, provided the conditions in FA 2013 Sch 45 para 51 are met, the student will be treated as non-UK resident up to the date they start to have a home in the UK, and as UK resident thereafter.

Residence status in home country

A complication for foreign students whose stay in the UK is intended to be of temporary duration and who retain connections with their home country is that they may remain tax resident in their home country for some or all of the duration of their studies.

Such students will need to take local advice in their home country to ensure that they understand their tax status there. They should also consider any foreign tax implications of ceasing to be tax resident in their home country, if this is likely to occur. For example, the home jurisdiction may levy an exit tax when residence ceases. Students coming to the UK from other EU countries should consider whether Brexit could have any impact on the exit taxes which may be charged.

Dual residence

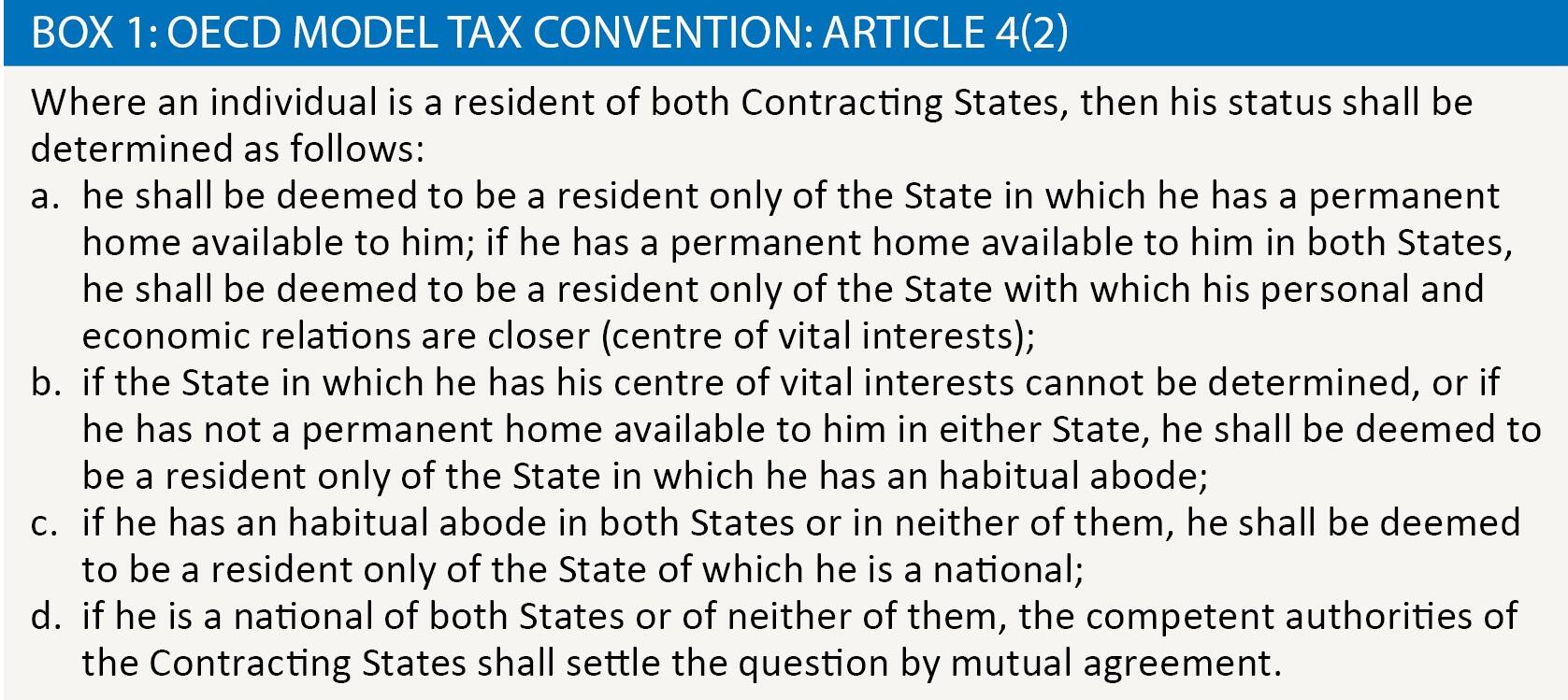

Where a student is ‘dual resident’, being tax resident in both their home country and in the UK, the ‘tie breaker’ provisions of the double taxation agreement (DTA) between the two jurisdictions will determine where the student is resident for treaty purposes. Many of the UK’s DTAs are based on the OECD Model Tax Convention and Box 1 contains the relevant extract from the Model. In the absence of such a treaty provision, a dual resident student could potentially be taxed in two jurisdictions on the same income and capital gains.

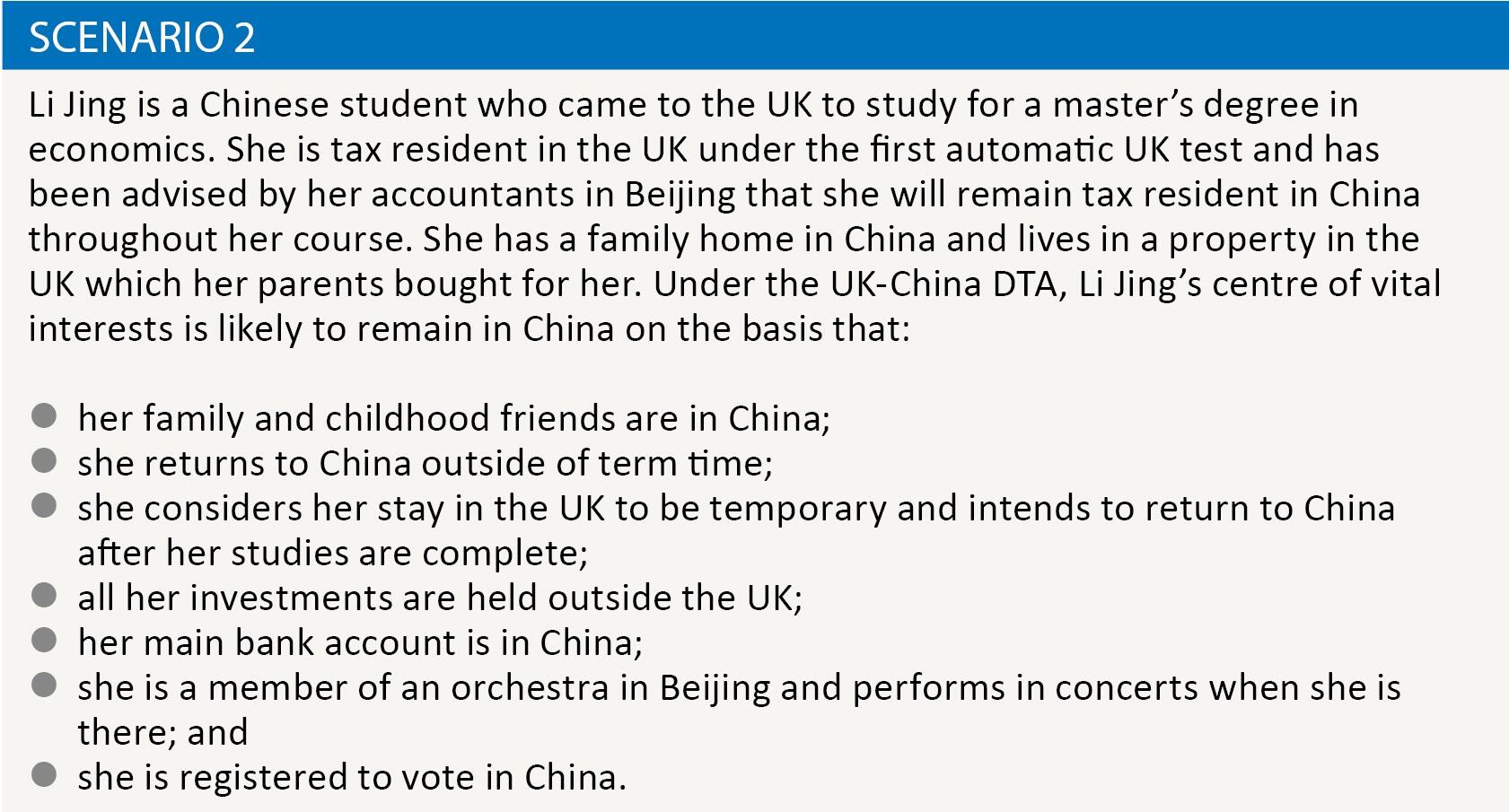

Each tie breaker test is to be considered in turn and later tests will only be relevant if earlier tests are not conclusive. Where it is necessary to determine a student’s centre of vital interests, a factual analysis of their family and social relations, their occupation(s), their political, cultural or other activities, their business activities, and so on, is required (see scenario 2).

Some students may find that their situation and intentions change over the course of their studies. Where this happens, their residence status will need to be reviewed in the UK, their home country, and under the treaty to ensure their tax position remains correct.

Domicile status

The domicile status of a UK resident student should be established from the outset, as it will be relevant to determining whether the remittance basis is available (see below). Full coverage of the UK’s domicile rules is outside the scope of this article.

In addition, if a student is a formerly domiciled resident (as legislated in Finance Act No(2) 2017 s 30), their worldwide assets will be brought within the scope of UK IHT once they become UK resident. In addition, they will not be eligible to claim the remittance basis.

Implications of being UK tax resident

If a student is found to be UK resident under UK domestic law and, if applicable, the tie breaker clause in the relevant DTA, a decision will need to be made as to whether they should be taxed on:

a. their worldwide income on an arising basis; or

b. their UK source income and capital gains and any foreign income and gains that are remitted to the UK (provided the student is not UK domiciled and makes a claim for the remittance basis).

The extent to which the remittance basis will be beneficial depends on the student’s level of overseas income, the extent to which income is remitted to the UK for purposes other than to fund maintenance, education and training (see below), the rate of tax charged in the home jurisdiction and the amount of any double tax relief available, the impact for the student of losing their personal allowance as a result of a remittance basis claim, and the student’s own preferred approach (some students may prefer the simplicity of being able to freely transfer funds between countries).

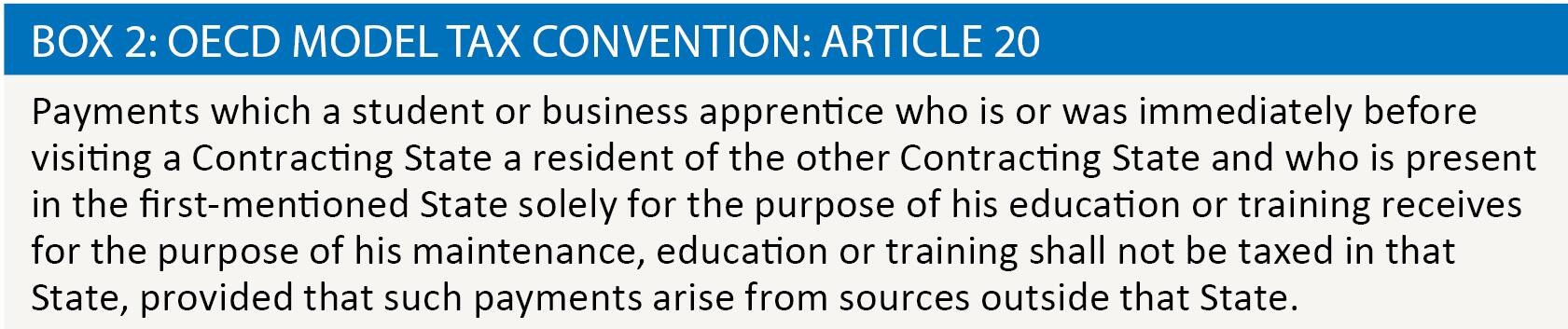

Many of the UK’s DTAs contain a provision which provides relief for overseas income and gains that are brought to the UK for the purpose of maintenance, education or training of a student (see Box 2 for the OECD Model provision).

This exemption generally covers funds which are used for normal living expenses, such as food and accommodation, as well as tuition fees and study materials. Where costs, excluding course fees, exceed £15,000, HMRC advise that they may seek additional supporting documentation.

A claim for the exemption should be made on Helpsheet HS302 (Dual Residents), together with details of the exact amount of income/gains which are covered by it.

To come back to Ryan (Scenario 1), if he is UK resident and claims the remittance basis, he should be taxable in the UK only on his UK source income and gains. Any income and gains arising in his Canadian investment portfolio will be protected from UK tax by the remittance basis claim, provided they are not brought to the UK. The income from the Canadian trust, though remitted, will be protected by the ‘Students’ article in the UK-Canada DTA as it is used to fund Ryan’s studies.

If Ryan is UK resident and does not claim the remittance basis, he will be taxable in the UK on his worldwide income and gains, but the distributions from the Canadian trust should still be protected by the UK-Canada DTA.

UK implications of being tax resident in another country

If a student is found to be non-UK resident under the treaty, a claim for treaty non-residence should be made on Helpsheet HS302 (Dual Residents) and submitted with the self-assessment tax return for each relevant year.

The student will then be taxable on UK source income and capital gains and on any overseas income and capital gains which are not covered by the treaty in the relevant years.

If Ryan (Scenario 1) is found to be non-UK resident under the UK-Canada DTA, he will need to submit a UK tax return and make a treaty claim on HS302, but provided he has no UK source income or gains he should not have a liability to UK tax.

Practical considerations

It will not always be immediately obvious to an international student that they have UK tax issues to consider and there may have been a time gap between the date they first came to the UK and the date they sought tax advice. In many cases, it will be necessary to register the student for self assessment and submit historic tax returns (including relevant treaty claims) to bring their affairs up to date. Care must be taken to bring the client into the system from the date they became UK resident under the SRT, and to submit returns within three months from the date they are issued by HMRC. If there is a tax liability in the relevant years, the student should be warned about possible late notification penalties.

While some wealthy students will be well versed in liaising with professional advisers, for others this may be the first time they have sought professional advice. Where this is the case, the adviser will need to take particular care to ensure that the advice is targeted to the client’s level of understanding and that their fee expectations are realistic.

LITRG have created a useful website for tax issues facing students: Tax Guide for Students