The taxation of foreign exchange

Share this article

Mandipa Soni and Edward Brown consider the tax liabilities arising from foreign exchange movements and ways to manage foreign exchange volatility on tax cashflows

Key Points

What is the issue?

Foreign exchange movements create significant volatility for companies, not least from a tax perspective. Many groups only identify these matters when drawing up entity accounts, as most projections are undertaken at a group level, where amounts may net to nil.

What does it mean for me?

Foreign exchange movements arising on loan relationships and derivative contracts are brought into account as they accrue in profit or loss in most cases. Tax liabilities can arise from exchange gains, which are unrealised and therefore unfunded, which can be problematic for many businesses.

What can I take away?

There may be occasions where you will need to ensure that any computations are prepared using the correct basis. In the context of foreign exchange, this may be the difference in whether gains and losses are brought into account on an accruals or realisation basis.

The current economic climate and market conditions have presented increasing uncertainty in currency markets over recent times. This can be an issue, as foreign exchange movements create significant volatility for companies, not least from a tax perspective. In our experience, it is also common that many groups only identify these matters when drawing up entity accounts, as most projections are undertaken at a group level, where amounts may net to nil.

As a result, companies are seeking to adopt strategies to manage foreign exchange risk and corresponding volatility on tax cashflows. Many of the options require careful and upfront coordination with Finance and/or Treasury functions to ensure that the relevant steps are implemented in time and documented appropriately.

In this article, we go back to basics on the taxation of foreign exchange from a UK corporation tax perspective, and also consider some of the options available to businesses to enable certain foreign exchange volatility to be managed from a tax perspective.

All references are to Corporation Tax Act 2009 (CTA 2009), unless otherwise stated.

Overview of the taxation of foreign exchange

The general rule is that foreign exchange (FX) movements arising on loan relationships (and certain money debts and holdings of foreign currency) and derivative contracts are brought into account as they accrue under the loan relationships legislation in accordance with CTA 2009 Parts 5, 6 and 7. As such, tax liabilities can arise from exchange gains, which are unrealised and therefore unfunded, which can be problematic for many businesses.

As defined in s 302, a loan relationship is a money debt, which arises from a transaction for the lending (or borrowing) of money. Furthermore, s 306A defines those matters which are to be brought into account for these purposes as being any profits or losses of a company that arise to it from its loan relationships and related transactions. This definition is extended in s 328 to include a reference to exchange gains and losses so arising.

Where money debts do not arise from a transaction for the lending of money (for example, trade receivables, rental income, etc. and are therefore not loan relationships under the basic definition), FX gains and losses would still be taxed in the same way as those FX movements arising on loan relationships (s 481(3)(b)).

Under s 475, exchange gains and losses are defined as profits or losses which arise as a result of comparing ‘at different times the expression in one currency of the whole or some part of the valuation put by the company in another currency on an asset or liability of the company’. Where that comparison produces neither a gain nor a loss, an exchange gain of nil is treated as arising.

As such, the default position is that FX gains and losses would be taxed or relieved as recognised in the profit and loss account, in accordance with generally accepted accounting practice. For accounting periods beginning prior to 1 January 2016, FX amounts recognised in reserves may also have been brought into account for tax in certain scenarios. However, this legislative change was not subject to any grandfathering, although there were transitional rules to be considered (outside the scope of this article). As such, no tax consideration needs to be given to FX until these amounts are ultimately recycled to the profit and loss account, unless:

- an asset or liability representing a loan relationship ceases to be recognised in the accounts; and

- it is not expected that either at that time, or at a later time, matters relating to that loan relationship will be transferred from other comprehensive income to the profit and loss account (s 320A).

Accordingly, a good understanding of the accounting treatment is required as part of the tax compliance process.

In summary, debits and credits attributable to FX gains and losses on loan relationships will form part of the overall debits and credits falling to be brought into account under Part 5. These amounts will then be taxed or relieved as trading debits and credits, or non-trading debits and credits on loan relationships – depending on the nature of the underlying debts.

As readers will be aware, the presentation of financial statements can be in currencies other than sterling and therefore the consideration of foreign exchange is not limited to exchange gains and losses arising between sterling and relevant ‘foreign’ currency denominated transactions. There may also be instances where sterling or the respective presentational currency is not always the currency in which the profits are required to be computed for corporation tax purposes. We next consider the respective rules which govern the currency to be used in tax calculations.

The currency to be used in tax calculations

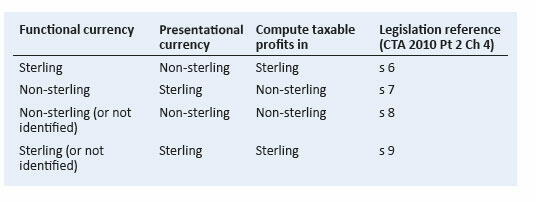

There are rules contained within CTA 2010 Part 2 Chapter 4 which determine the currency to be applied when income and gains must be calculated and therefore in determining loan relationship profits. The default position, CTA 2010 s 5, provides that for the purposes of corporation tax, the profits of a company for an accounting period must be calculated and expressed in sterling. However, this basic rule is subject to ss 6 to 9, which consider the situations where the functional or presentational currency differs from sterling as outlined in the table below.

CTA 2010 s17(4) defines ‘functional currency’ as the currency of the primary economic environment in which the company operates. The ‘presentational currency’ is that in which the accounts are prepared.

CTA 2010 ss 6-9 apply to those profits or losses that fall to be computed in accordance with generally accepted accounting practice. This means that they do not apply to the calculation of other matters. One common example is the calculation of capital gains, which will generally be calculated by reference to sterling (although Finance Act 2013 s 66 modifies this rule in relation to assets comprising ships, aircraft shares and interests in shares).

CTA 2010 ss 6-9 will apply to the calculation of trading profits, property business profits and, importantly for the purposes of this article, loan relationships, derivative contracts and the related FX calculations.

Accordingly, there may be occasions where you will need to ensure that any computations are prepared using the correct basis. In the context of FX, clearly this could be the difference in whether FX gains and losses arise in the first place.

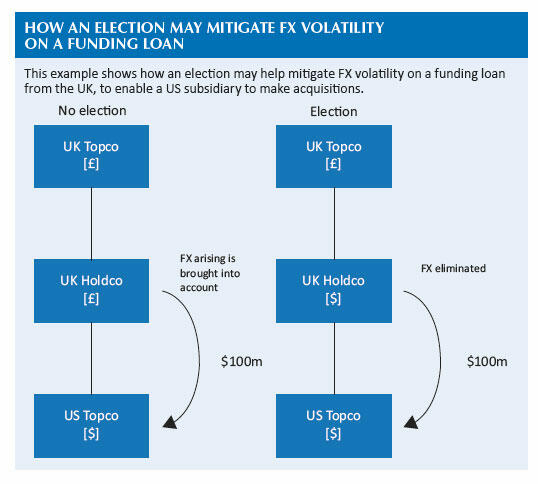

It is worth noting that in the case of a UK resident investment company, it may be possible for the company to elect for a currency to be its ‘designated currency’; and therefore the underlying accounting treatment can be overridden, which can be helpful in certain situations.

Designated currency elections

A UK resident investment company may elect to designate a functional currency for tax purposes, which may be a currency other than the functional currency of its financial statements. An ‘investment company’ is defined in CTA 2010 s 17 as a company whose business consists wholly or partly in the making of investments and the principal part of whose income is derived from those investments.

The implications of such an election is that profits and losses of that company for UK corporation tax purposes would be computed by reference to the designated currency (and not the functional or presentational currency in the accounts). To apply this election, either of the following two conditions must be satisfied (CTA 2010 s 9A):

- Condition A: A significant proportion of the company’s assets and liabilities are denominated in the currency.

- Condition B: The currency is a functional currency of another company and it is reasonable to assume that the two companies meet the consolidation condition (i.e. the companies are part of the same consolidated group in accordance with acceptible accounting practices).

With reference to Condition A above, there is no guidance in the legislation as to what constitutes a ‘significant’ proportion in this context. It will depend on the facts of the individual company; broadly, though, it will be the currency to which the investment company has the most exposure as a result of holding those assets or liabilities in the respective currency. As HMRC states in CFM64520, a common sense approach must be adopted, considering the proportion of foreign currency assets and liabilities, but also other factors, including (as it suggests) the relative exchange rate volatility.

When considering Condition B, acceptable accounting practices are considered to be IAS, UK GAAP or the GAAP of the country in which the other company is resident. It is worth noting that if the group is not required to prepare consolidated accounts, the test will still be met if the group would be required to prepare consolidated accounts were its financial statements prepared under IAS.

A designated currency election must specify the date on which the election is to take effect and must be made in advance of that date. The election then continues to apply until a future revocation event, which is when the company ceases to satisfy the relevant conditions, or another election takes effect (CTA 2010 s 9B). A brief example in the box on the left shows how an election may help to mitigate FX volatility.

It is worth noting that s 328 prescribes that where FX arises as a result of a change in functional currency, the question as to whether this should be brought into account to tax depends on whether the change arose as a result of a designation election or otherwise.

Other matters to consider

There are a number of other provisions specifically relating to foreign exchange (within the loan relationship rules) that may also be worth bearing in mind.

1. The taxation of non-arm’s length transactions

You may be familiar with the general principles on non-arm’s length loans from a transfer pricing perspective. Section 444 is the general provision that requires debit or credits to be determined in accordance with the ‘independent terms’ assumption. It is disapplied under s 445 where TIOPA 2010 Part 4 applies, such that in most cases it requires FX to be brought into account for debtor relationships on the basis of an arm’s length loan.

This can differ for a creditor relationship, which will only apply to the extent that a ‘corresponding debtor relationship’ does not exist. There will be a ‘corresponding debtor relationship’ where the debtor to the creditor loan relationship is within the charge to UK corporation tax and is required to bring into account the exchange gains and losses for tax. Therefore, the rules should only apply to a lender where amounts are being lent to a non-UK resident overseas company.

2. Connected company relationships

Under ss 354 and 358, the release or impairment of connected company loan relationships are specifically excluded from tax. However, these specific exclusions do not extend to FX and, as such, FX gains and losses may still be required to be brought into account to tax where the underlying balance requires FX to be retranslated for accounting purposes.

3. Exclusion in respect of tax debts Under s 486, a specific exclusion from corporation tax for FX arises with respect to money debts representing an amount of tax payable under UK law. This is also extended in certain situations for overseas tax matters. Accordingly, care should be taken to ensure FX arising in the P&L does not contain any amounts relating to tax debts, albeit this will be driven in part by the tax provisioning workings.

4. Overseas considerations

Whilst managing FX volatility in the UK may be important, it should not be done in isolation. In a group context, consideration should also be given to the taxation of FX overseas, as this may result in a mismatch on cross-border balances. For example, the US only taxes foreign exchange movements when amounts are realised. In addition, from a hedging perspective, international groups are likely to use foreign operations and cashflows as part of their overall hedging strategy, so FX may not be significant on an individual entity basis. As such, there needs to be consideration as to how the treatment of FX fits with the group’s overall hedging strategy and which entities ultimately bear the risk.

Hedging: an overview

The overview provided in this article has been focused on the basic taxation of FX within the loan relationships legislation. Similar rules governing the taxation of FX are also contained within the derivative contract rules in Corporation Tax Act 2009 Part 7.

Companies often adopt numerous strategies to manage FX volatility. This could be for accounting purposes or to manage economic risk, which can have tax implications and is often the responsibility of a specialist Treasury function. There are also a number of specific tax rules that apply in hedging scenarios which can assist in managing foreign exchange volatility until a realisation event. The topic of hedging is worth an article in itself; however, we have set out below the issues that are commonly seen in our experience.

Companies often adopt different strategies to manage FX risk, for accounting purposes or to manage economic risk.

Matching’ and/or ‘net investment hedging’

In this case, the hedging instrument (either a loan or derivative) must be taken out with the intention of managing exchange rate risk and have the specific intention of substantially eliminating or reducing the economic risk of the asset (or hedged item) that is attributable to exchange rate risk. Where the relevant conditions are met, the matching rules are generally mandatory and apply on meeting all the necessary conditions. The specific provisions are set out in the Loan Relationships and Derivative Contracts (Disregard and Bringing into Account Profits and Losses) Regulations – SI 2004/3256 (‘the disregards’).

For example, where a UK resident company borrows in a currency other than its functional currency to hedge its currency risk on its investment in an overseas subsidiary, FX arising on that loan (provided the necessary conditions are met) can be matched with the investment such that the FX is not brought into account until the prescribed time. Typically, this would be on the disposal of the investment. This ensures that the FX profit or loss is matched with the realisation of the asset.

Forward currency contracts

Where companies also use derivative contracts to mitigate exchange risk, the disregards can be applied by way of election, from a particular date, to apply a realisations basis for tax purposes.

A common example is the use of foreign currency forward contracts which may help manage the economic risk involving the underlying foreign exchange assets or liabilities of a future purchase or transaction. Under accounting standards, derivative contracts are required to be held at fair value, which could bring fair value volatility to the P&L. However, companies might then designate the derivative contracts as hedges for accounting purposes (hedge accounting) which may reduce or eliminate FX and fair value volatility for both accounting and tax purposes. However, where hedge accounting is not applied, or is ineffective, the disregards can rectify this position for tax purposes. Other similar elections are available with respect to commodity contracts or interest rate swaps.

Conclusion

FX volatility can be costly to businesses if not managed appropriately. Whilst the default position for tax purposes is that FX gains and losses should be brought into account to tax as it accrues to profit or loss, there may be accounting, treasury or even tax strategies available to help manage the volatility.

The key message to tax teams is not to leave FX out of the conversation and to ensure that they are working closely with Finance and Treasury colleagues to assess FX exposure and implement strategies that may be beneficial to the business.