The temporary workplace: applying the intention or expectation test

Share this article

We consider what constitutes a temporary workplace and the significance that expectation plays in determining whether related expenses attract tax relief.

Key Points

What is the issue?

If an employee attends, or expects to attend, a workplace for 40% or more of their working time at a particular workplace over a period of more than 24 months (the ‘40/24’ test), it cannot qualify as a temporary workplace.

What does it mean for me?

Employers often feel that the intention or expectation test cannot be easily operated or proven in practice.

What can I take away?

Undertake a review and record where employees are based for the purposes of travel and subsistence, including any secondments or temporary assignments.

The travel and subsistence rules are complex and can be difficult for employers to apply on a consistent basis, particularly given the context of changing work patterns and mobility of workers.

As explained in our previous article, ‘The long and winding road’ (June 2022), a workplace that an employee attends for the purpose of performing a task of limited duration or for some other temporary purpose is potentially a temporary workplace under the Income Tax (Earnings and Pensions) Act (ITEPA) 2003 s 339(3).

This and the associated criteria are all important points to consider because when a journey qualifies for tax relief, employees are also entitled to claim tax relief on subsistence expenditure that is incurred on that journey. This includes:

- any necessary subsistence costs incurred in the course of the journey;

- the cost of meals necessarily purchased whilst an employee is at a temporary workplace; and

- the cost of the accommodation and any necessary meals where an overnight stay is needed as part of the journey. This will be the case even where the employee stays away for some time.

In this article, we explore more on the 24-month rule at ITEPA 2003 s 339(5), which forms part of the test of whether a workplace is a temporary workplace. This could result in more challenges than normal following the Covid pandemic and the move to hybrid working patterns in the UK and international employment situations.

What is a temporary workplace?

Remember that the test which prevents a workplace from being a temporary workplace is where an employee attends it in the course of a period of continuous work that lasts more than 24 months, or where it is reasonable to assume that it will be in the course of such a period that will last more than 24 months. This is known as the 24-month rule or is often described as the detached duty rule. This means that where the employee has spent, or is likely to spend, 40% or more of their working time at that particular workplace over a period of more than 24 months (the ‘40/24 test’), it will be a permanent workplace.

In terms of the 40% rule, ITEPA 2003 s 339(6) states: ‘For the purposes of sub-section (5), a period is a period of continuous work at a place if over the period the duties of the employment are performed to a significant extent at the place.’ The word ‘significant’ is not defined in statute, but it is covered in HMRC’s Employment Income Manual at EIM32080, which states that anything less than 40% is not significant.

The significance of expectation

One of the key problem areas is the words ‘reasonable to assume’. Note that there is no reference to either the intent of the employer or employee. Although this is often described as intention, it is also sometimes referred to as expectation.

The rule is not just about the amount of time being less than 24 months for relief to be given, but the intention or expectation of the parties at the time the period was originally agreed and at any time subsequently.

On first inspection therefore you would think that if an assignment or secondment to a different location was for less than 24 months, the employee would meet the temporary workplace conditions for that period. If the employer extends the assignment to more than 24 months, then the workplace is only temporary up until the date that the assignment is extended. If at the outset it is known that it was going to be for longer than 24 months, then relief is not due from the start.

Problems can arise where the outcome does not match the original intention. If a full-time assignment is expected to last more than 24 months (and is therefore not eligible for relief) but unexpectedly finishes early, no deduction is allowable even though ultimately the assignment lasted for less than 24 months. Because the initial expectation was that the assignment would meet the 40/24 test, the workplace would be considered to be permanent even though, in practice, that turned out not to be the case.

To further complicate matters, an employee does not need to have a permanent workplace to go back to in order to be entitled to tax relief for travel to a temporary workplace, if they meet the criteria.

More points to consider

It should also be remembered that a fixed term appointment or contract prevents a workplace being a temporary workplace where an employee attends, or is likely to attend, it in the course of a period of continuous work for all or almost all of the period that they’re likely to hold the employment, as stated in ITEPA 2003 s 339(6). This adds a further layer of complexity:

- A period of continuous work for this purpose has the same meaning as it does for the 24 month rule – that is, it’s a period during which the employee spends or is likely to spend more than 40% of their working time at a particular workplace. A period of continuous work can remain continuous even where there is a break in attendance (see HMRC guidance at EIM32108).

- For the purpose of determining a period as being all or almost all of the period that the employee is likely to hold the employment, HMRC considers that period is more than 80% of the likely duration of the employment.

This does not take into account that when the employment intermediaries travel expense provisions apply (ITEPA 2003 s 339A), it should be remembered that each engagement will be treated as a separate employment for the purposes of the travel expenses rules (see ITEPA 2003 ss 338, 339 and 339A of ITEPA, and the corresponding NICs disregard in the Social Security (Contributions) Regulations 2001 Sch 3 Part 8 paras 3, 3ZA and 3ZB).

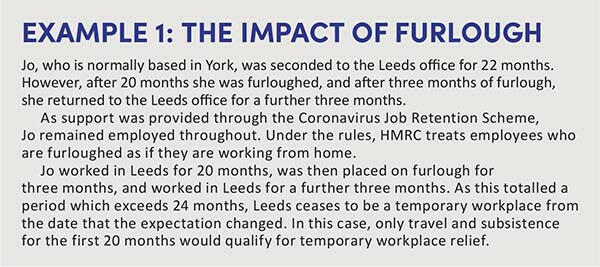

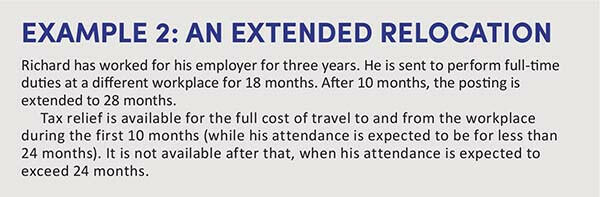

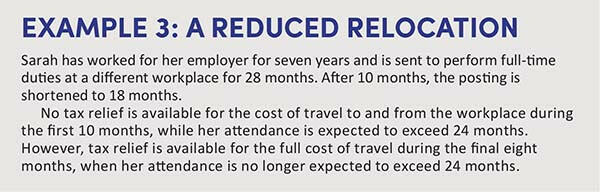

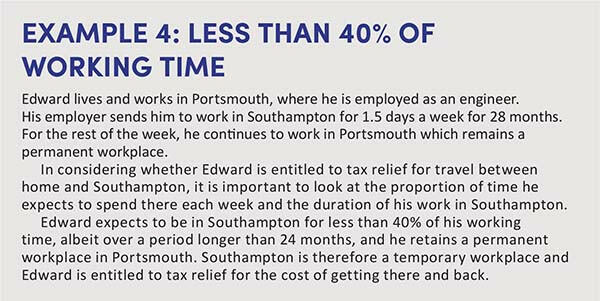

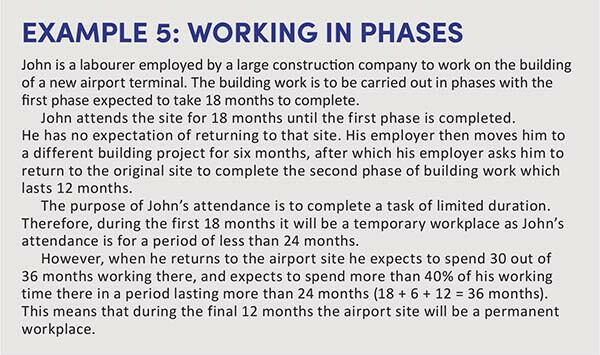

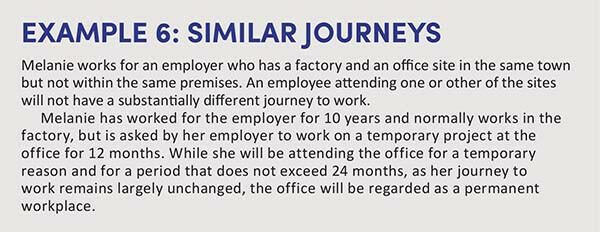

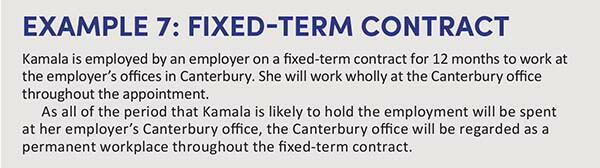

These rules and the interaction are often best illustrated by examples. We have detailed a few above.

The need to be alert

Employers often feel that the intention or expectation test cannot be easily operated or proven in practice. This is because the person who has to make the decision about whether or not to treat an expense payment as taxable is often a long way removed from the details of the individual’s case and working arrangements. Mistakes can be made if the decision maker does not have access to any contracts or side agreement (such as visas or other official documents) which might help to demonstrate any argument that it is ‘reasonable to assume’ that the temporary workplace will be for less than 24 months.

There is therefore a danger that employers do not pick up expenses that should be liable to tax and NIC, either by placing them through the payroll where they are reimbursed, or on a P11D if arranged and paid directly and where there is no PAYE settlement agreement in place. If this issue is identified by HMRC or the employer at a late stage, it can be costly. As well as the tax and NIC that is due, the employer can also face interest and penalties.

We expect that HMRC will be looking carefully at these rules when undertaking compliance reviews over the next few years, due to the various changes to place of work as a result of the Covid pandemic.

How can employers get it right?

- Undertake a review and record where employees are based for the purposes of travel and subsistence, including any secondments or temporary assignments. Make sure to track any changes to these.

- Consider adding extra checks of expenses claims to pick up any patterns.

- Make sure that key people in the organisation understand the rules based on knowledge of their own workforces.

- Make sure that policies are clear on what employees can claim and that any individual agreements are tracked. Also, when any changes to the rules are made, make sure everyone understands the costs and payroll or P11D implications.

- Ensure that adequate information is provided when expenses forms are completed, so that the correct tax treatment can be applied.