Thick and fast

Share this article

Mike Anthony and John Moss consider some of the practical issues of auto-enrolment encountered by advisers

Key Points

What is the issue?

More than one million employers are due to register a scheme in 2016/17 and begin to operate it. Many will look to their advisers to guide them through the process

What does it mean to me?

At present, businesses using HMRC Basic Tools for administering their payroll lack the function to produce the data in the format required by any of the pension providers

What can I take away?

Opt-out rates are relatively low, with the number of workers participating in new schemes higher than employers had expected

From a slow start, auto-enrolment registrations are progressing thick and fast. To put it another way, registrations will become fast and furious as we move into 2016 and 2017.

The timetable for auto-enrolment started in 2012 and for all employers at that time registration will continue until 2017. Initially registrations were on a size basis, with the larger organisations having to register in the first 12 months. The few that missed their staging date suffered well-publicised fines.

Since July 2015, all employers with 50 or fewer employees have been preparing for their staging date that could be any time from now until August 2017. It is expected that new businesses set up after 2012 will have a staging date towards the end of 2017.

However, The Pensions Regulator (TPR) has been using the media to urge employers to think about arrangements well in advance of their staging date. TPR is pressing employers to register primary and secondary points of contact and make them aware of the fines they face should they miss the deadlines. TPR is also providing information online and on its website.

When the government launched auto-enrolment, it did so on the basis that employers could introduce a scheme for their workforce themselves without professional advice.

As long as the employer offers its workforce a scheme that complies with the legislation, it will have carried out its legal responsibility.

The offerings of professional advisers have been mixed, with some trying to guide clients towards a specialist pensions adviser and others offering a complete advisory service to clients. It is important that a tax adviser is familiar with the legislative requirements of auto-enrolment to guide the client through the decision-making process. Once cognizant, many clients will want the adviser to complete the process on their behalf.

The adviser needs to be able to run through these steps and action points:

- establish staging date;

- primary and secondary points of contact;

- eligibility rules;

- levels of contribution;

- choice of scheme provider;

- registration of scheme;

- opt-out rules;

- postponing commencement;

- software requirements;

- choice of earnings basis;

- presentations to employees;

- scheme information to employees;

- payroll advice;

- guidance on fund selection in pension scheme;

- assess workforce; and

- issuing certificate of compliance.

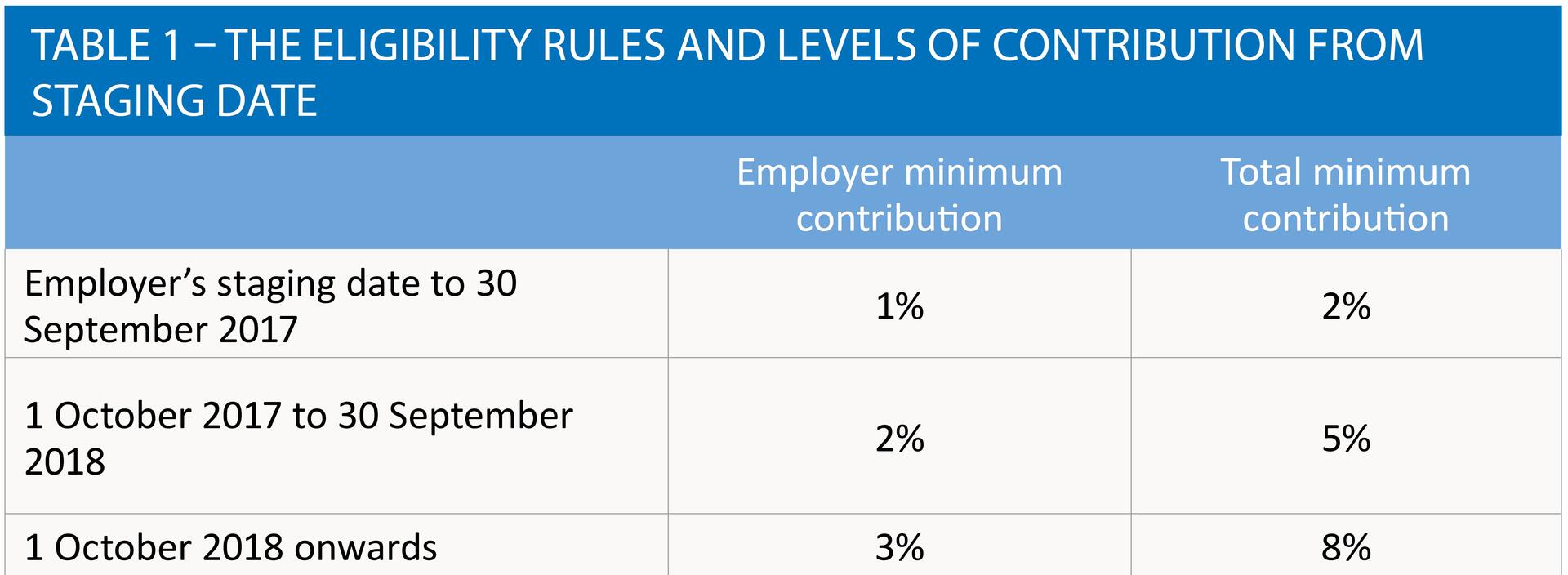

Table 1 outlines the eligibility rules and levels of contribution from the staging date to October 2018 when total contributions increase to 8%. It is important to explain the tax relief available to employees and the cost to them out of net income. Employers will receive tax relief on their contributions as a business expense.

The choice of scheme is of particular concern to employers but should not be the case since their responsibility is simply the introduction of a compliant scheme. There is a cap of 0.75% on charges for auto-enrolment schemes. That benefits scheme members, but it leaves providers waiting some time before they make a return on their investment, so much so that some large providers have chosen not to get involved with auto-enrolment while others require a set-up fee or minimum contributions. The default government scheme is the National Employment Savings Trust (NEST) and must be offered to employers, even if there is only one employee. NEST has a low fund annual management charge (AMC) of 0.3% but, because of the government loan to finance it, there is a contribution charge on top of the AMC that makes the scheme costly in the early years.

Another area of concern for employers and ultimately members is the provider’s fund selection choices. Most schemes are modelled on lifestyling, which involves gradually moving from managed funds into safer fixed interest or cash funds as members approach retirement.

All providers must offer a minimum range of funds that should meet the needs of all members. This includes three managed funds (balanced, cautious and adventurous), cash, ethical, Sharia and a pre-retirement pension fund. Although an area of concern to employers, the provider will give enough information for an employee to make their own investment decision.

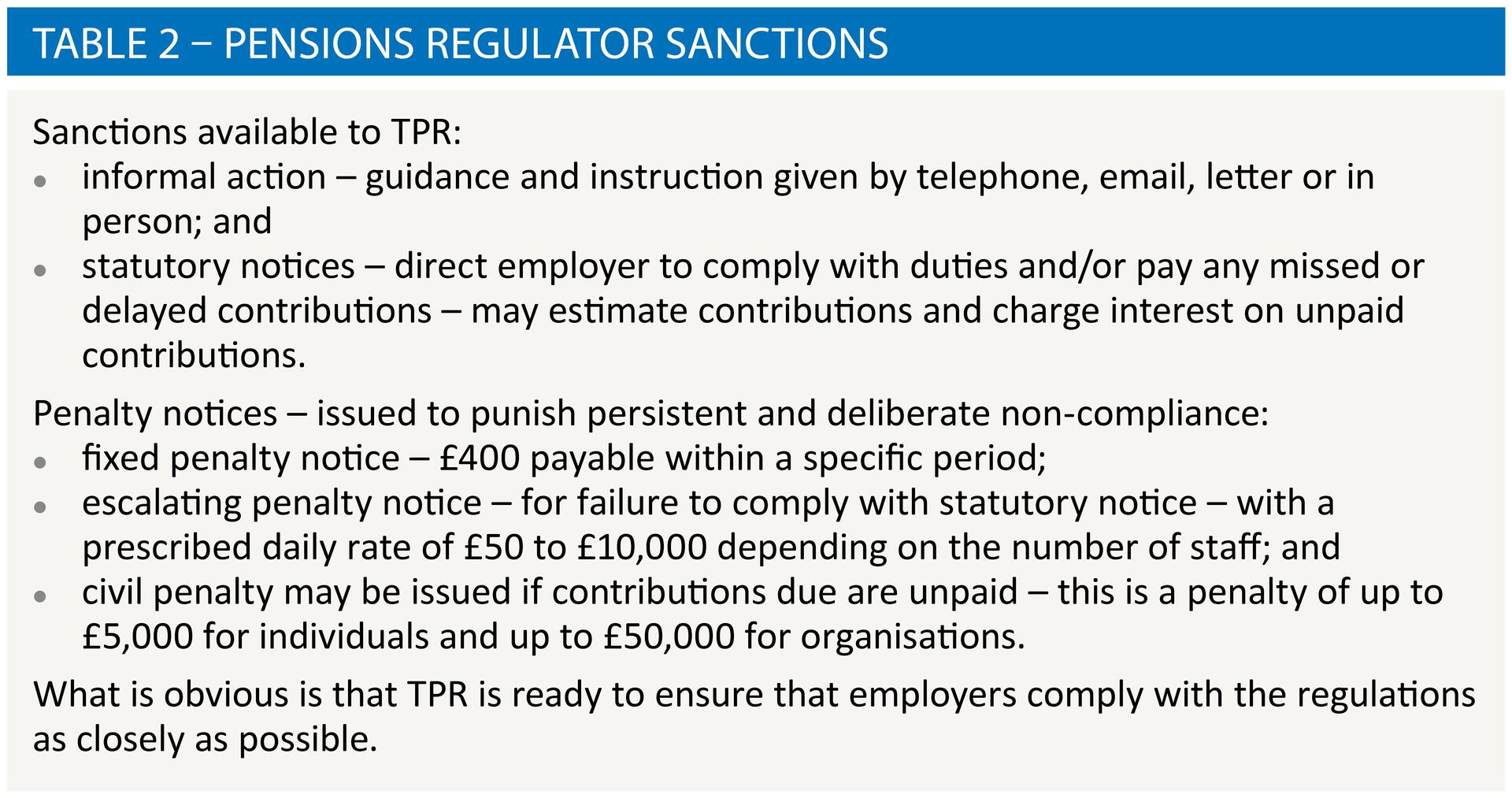

Despite the best efforts of TPR it is obvious that some employers are ignoring the publicity and not engaging with the principle of auto-enrolment. This can lead TPR to invoke the sanctions set out in Table 2.

The greatest service that an adviser can provide for a client is to encourage them to start taking action as early as possible – during 2016/17 more than one million employers are due to register a scheme and start operating it. There is, of course, the business case for planning and budgeting for the increasing costs of contributions between 2015 and 2018.

Practical issues encountered include:

- Basic misunderstanding of the requirements by some employers who think that they do not need a scheme in place because all of their employees have said that they do not want it.

- Currently, businesses using HMRC Basic Tools for administering their payroll do not have available within the payroll function a tool for producing the data in the format required by any of the pension providers. Hopefully this will be rectified before too many businesses face practical difficulty.

- Some employers with an existing pension scheme, often with contributions already in excess of the eventual minimum 8%, are forced by regulation to replace it with a new compliant one. Inevitably, members will ask what they should do with the funds from their schemes that are being closed.

- Some pension providers are unclear about whether their schemes are compliant – leading to misunderstandings on the part of businesses.

- Many businesses are finding that the provider of their scheme that has been operating successfully for many years is suddenly announcing that a monthly management charge will be payable if it is to continue under auto-enrolment regulations.

- Employer and employees that hold strong ethical investment principles are dissatisfied with the funds made available by many of the major mass-market providers. The solution in this case is to put in place a scheme with a range of ethical funds available, albeit with higher AMCs.

- Opt-out rates are relatively low, with many more workers participating when schemes start than employers expect.

- The attraction of tax benefits associated with pensions, particularly the immediate uplift in the form of basic rate tax relief, together with the pensions freedoms introduced last year are encouraging many older workers to continue membership rather than opt out.

- There is evidence that employers are recognising the historical advantages of pension schemes – recruitment, retention and reward.

Further information

More information can be found on The Pensions Regulator website.