Time to share

Share this article

David Hammal and Adrian Rudd consider the impact of the UK’s participation in the EU Mandatory Disclosure Regime, known as DAC 6

Key Points

What’s the issue?

The EU Mandatory Disclosure Regime requires intermediaries based in the EU and, in certain circumstances, taxpayers, to make disclosures of ‘cross-border arrangements’ satisfying one or more hallmarks to an EU tax authority. Whilst intended to target aggressive tax avoidance, the hallmarks have been deliberately set very broadly and many entirely commercial transactions will be disclosed.

What can I take away?

The Directive starts from the principle that it is most appropriate for advisers (‘intermediaries’) to make disclosures. The definition of intermediaries is very broad and is not limited to tax advisers; it could encompass lawyers, corporate finance advisers, private equity/investment management firms, etc. If there is more than one EU intermediary, then the Directive places the obligation to disclose on every such intermediary. A 30 day reporting window will apply from 1 July 2020. Significant penalties may also be imposed by tax authorities for non-compliance.

What does it mean to me?

Identify a central team within the organisation to take ownership of getting ready for DAC6, engage early in discussions with other intermediaries, and undertake an impact assessment to better identify parts of your business which could be most affected by the rules.

The EU Mandatory Disclosure Regime (MDR), also known as DAC6, is an EU Directive implementing the recommendations of the OECD BEPS Action 12, as regards the mandatory automatic exchange of information in the field of taxation in relation to reportable cross-border arrangements. It took effect on 25 June 2018 and was required to be implemented in all 28 member states by 31 December 2019.

In this article, we consider the Directive itself and the UK’s draft regulations and consultation document released on 22 July 2019. At the time of writing, the final regulations and any updated guidance have not been released by HMRC.

It is worth noting that the government is committed to international tax transparency and we expect that EU MDR will be implemented, notwithstanding Brexit. Accordingly, we have written this article on the assumption that EU MDR will apply in full in the UK and any necessary adjustments to accommodate Brexit

are made.

EU MDR requires intermediaries based in the EU and, in certain circumstances, taxpayers, to make disclosures of ‘cross-border arrangements’ satisfying one or more hallmarks to an EU tax authority. It then requires the tax authority to share the disclosed details around all other 27 member states on a quarterly basis.

In this article, we will discuss some of the practical issues created by EU MDR, and will also briefly look at its implementation in Poland. Poland is the only member state to implement the full rules early (from 1 January 2019), and they are of relevance to UK practitioners and businesses. Poland has decided to make these rules extra-territorial and they apply equally to Polish and non-Polish advisers and businesses.

The Directive

DAC6 applies to ‘arrangements’ undertaken by taxpayers, or made available to taxpayers. ‘Arrangements’ are not defined in the Directive, other than to note that ‘an arrangement shall also include a series of arrangements. An arrangement may comprise more than one step or part’ (DAC6 Art 3 para 18). A relevant arrangement must be ‘cross-border’ and this requires that it ‘concerns’ more than one member state, or at least one member state and a third country.

Hallmarks

To be reportable, such a ‘cross-border arrangement’ must satisfy one or more of 19 hallmarks. Space does not permit a full consideration of all of these hallmarks, although we do discuss some of them later.

Nine of these hallmarks are subject to a ‘main benefit test’ which only requires disclosure if it can also be ‘established that the main benefit or one of the main benefits … a person may reasonably expect to derive from an arrangement is the obtaining of a tax advantage’ (DAC6 Annex 4 Part 1).

Whilst this approach will make the rules more targeted and therefore easier to apply, as the main benefit test does not apply to the other ten hallmarks many arrangements which do not produce any tax benefits will still be disclosable.

Focus on intermediaries

The Directive starts from the principle that it is most appropriate for advisers (‘intermediaries’) to make disclosures, with this obligation transferring to taxpayers in certain circumstances – such as where there are no relevant EU intermediaries or where such EU intermediaries rely on ‘professional secrecy’ or legal professional privilege.

If there is more than one EU intermediary, then the Directive places the obligation to disclose on every such intermediary. It does provide for circumstances in which intermediaries can rely on another’s disclosure, although in practice these may be difficult to rely on, as discussed further below.

To be an intermediary, you first have to have a relevant connection with a member state and be a person who either:

- designs, markets, organises or makes available for implementation or manages the implementation of a reportable cross-border arrangement (commonly referred to as a ‘promoter’); or

- knows or could be reasonably expected to know that they have undertaken to provide ‘aid, assistance or advice’ with respect to designing, marketing, organising, making available for implementation or managing the implementation of a reportable cross-border arrangement (commonly referred to as a ‘service provider’).

These are clearly very broad definitions and there is no limitation to those providing tax advice. In the context of a typical transaction, this could include accountants, corporate tax advisers, management tax advisers, lawyers, banks, private equity investment professionals, valuation experts and others. In a multi-territory transaction involving a number of EU territories, the number of intermediaries could be eye-watering.

Timing of disclosures

Arrangements with the first step of implementation between 25 June 2018 and 30 June 2020 are required to be disclosed between 1 July 2020 and 31 August 2020. The full regime takes effect from 1 July 2020 and requires that arrangements are disclosed within 30 days of the earliest of a number of trigger events (e.g. the day after the arrangement is ‘made available’ by the promoter).

In addition, for ‘service providers’, there is a separate deadline of 30 days from the day after they provided the relevant ‘aid, assistance or advice’.

UK draft regulations and consultation document

The draft regulations issued by HMRC on 22 July 2019 generally follow the Directive closely. There are, however, a few points to highlight.

Tax advantage

HMRC have made two extensions to the definition of ‘tax advantage’ in the Directive, one of which broadens and the other of which limits its potential reach.

Firstly, it applies to a tax advantage in any territory worldwide and not, for example, just UK or EU taxes. (The types of taxes in scope are those covered by the Directive generally, so direct taxes are in scope, but not indirect taxes, duties, etc.) Most other territories have limited the geographical reach of ‘tax advantage’ to EU taxes.

Secondly, the draft regulations limit tax advantages to tax benefits not consistent with the principles or the policy objectives of the relevant tax provisions. This approach will help focus the rules.

Hallmarks

HMRC have broadly left the hallmarks unchanged from the Directive. The one substantial difference relates to the ‘E’ hallmarks (specific hallmarks concerning transfer pricing). HMRC are proposing to exclude SMEs from the remit of these three hallmarks.

Legal professional privilege

HMRC are proposing to allow relevant intermediaries to rely on legal professional privilege (LPP). However, they have said that they consider LPP not to cover factual data such as names of taxpayers and other intermediaries, and a description of the transactions to be undertaken; and they expect lawyers to submit disclosures containing information of this nature. Whether that is a correct interpretation of LPP will surely be debated.

Penalties

The consultation paper proposes financial penalties of up to £600 per day (without limit) for failure to make a report. The initial penalty is imposed by the First-tier Tribunal, and if the daily penalty ‘appears inappropriately low’ then the tribunal can set the penalty of up to £1 million, ‘as appears appropriate’ having regard to the circumstances (draft Reg 15(5)).

The level of penalties is greater than the vast majority of other member states and will be of concern to intermediaries and businesses, particularly those who are not tax specialists.

Problems with DAC6

We now turn to some of the concerns which we have with the Directive.

Broad scope applying to purely commercial transactions

As noted above, the lack of a main benefit test for ten of the hallmarks will mean that many everyday commercial transactions will be disclosable.

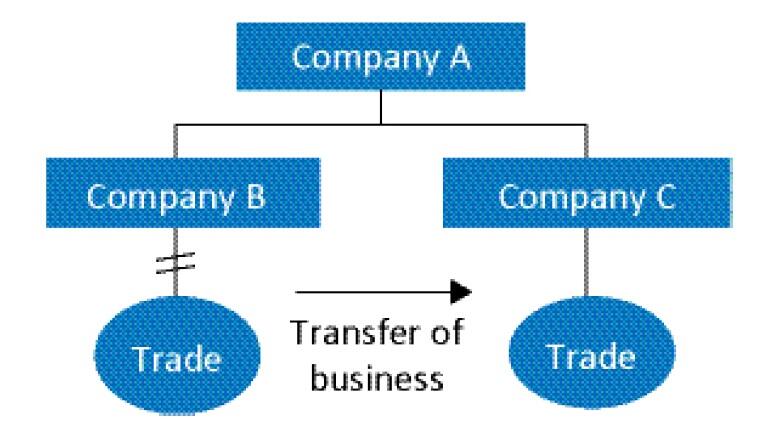

Example 1: E3 and business transfers

This hallmark applies to:

‘An arrangement involving an intragroup cross-border transfer of functions and/or risks and/or assets, if the projected annual earnings before interest and taxes (EBIT), during the three-year period after the transfer, of the transferor or transferors, are less than 50% of the projected annual EBIT of such transferor or transferors if the transfer had not been made.’

Consider the following facts:

- Company A (resident in territory A) owns Company B (resident in territory B) and Company C (resident in territory C).

- The corporate tax rate in territory C is higher than in territory B.

- Company B operates a profitable business, which is expected to continue to be profitable going forward.

- The business of Company B is transferred to Company C, following which Company B is dormant.

This would satisfy hallmark E3, as the forecasted EBIT of Company B has been reduced, notwithstanding the fact that it may result in a higher corporate tax liability.

E3 could apply to many typical corporate simplification transactions. For example, a cross-border liquidation or merger where the company ceasing to exist was expected to have positive EBIT is likely to be disclosable.

Imprecise wording leading to unintended consequences

Many of the hallmarks seem to have been written with a particular mischief in mind, but have been widely drafted, and as a result more transactions will fall within scope than might be expected.

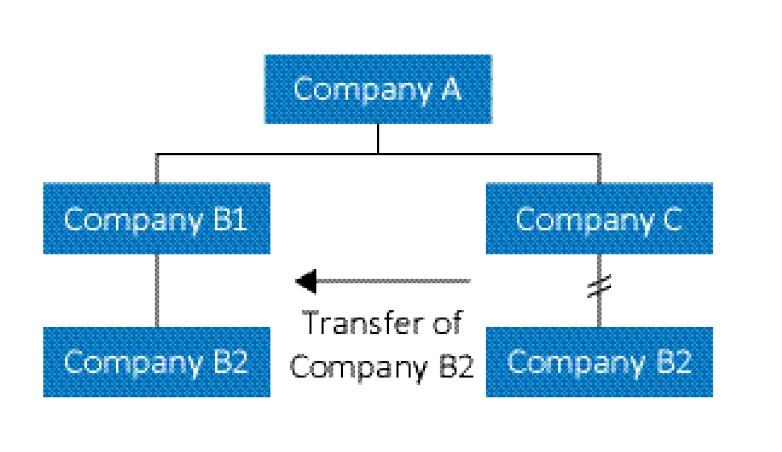

Example 2: E3 and shares

Let us again consider hallmark E3, but this time in the context of share transfers. The category E heading of ‘Specific hallmarks concerning transfer pricing’ and the focus on functions, assets and risks may make you think that this should be limited to transfers of operations or other assets producing operating income (e.g. a transfer of business as in Example 1). However, the drafting suggests that it could apply to the transfer of shares. Consider this example:

- Company A (territory A) owns Company B1 (territory B) and Company C (territory C).

- Company C is a sub-holding company, the only asset of which is shares in Company B2 (territory B).

- B2 is a profitable trading entity which pays substantial annual dividends and these dividends are anticipated to continue to be paid as Company A requires regular cash repatriation.

- Company C transfers the shares in Company B2 to Company B1 for intra-group debt.

Here we have an intragroup cross-border transfer of an asset (shares in Company B2). As a result, Company C goes from a position where it expected regular dividends (included in EBIT) but these are replaced by interest income (not included in EBIT). There are arguments that this transaction could satisfy E3 and therefore be disclosable.

If shares and dividends are within the scope of E3, then this would bring a very large number of ordinary corporate restructuring transactions within the scope of E3, regardless of the tax outcome of those transactions. In practice, however, the situations which are disclosable will be limited by the fact that it is rare that future dividends can be anticipated with sufficient certainty to be included in ‘projected EBIT’. However, there will be cases, such as where there is a consistent history of regular dividend payments and a commercial requirement for the cash in the parent, where this will be satisfied.

Differences in enactment and interpretation between territories

There are also differences in how the rules are being enacted and interpreted around the EU. One example is the definition of tax advantage in the UK’s draft regulations, which may result in arrangements not being disclosable in the UK which are disclosable elsewhere. Another relates to the UK’s exclusion of SMEs from the E hallmarks.

Example 3: Hallmark E1 and SMEs

Hallmark E1 applies to: ‘An arrangement which involves the use of unilateral safe harbour rules.’

As noted above, the UK has excluded SMEs from the E hallmarks in the draft regulations; hence, arrangements involving SMEs would not be disclosable in the UK under these hallmarks. This makes it clear that the UK’s exemption of SMEs from the main transfer pricing rules is not a unilateral safe harbour, for the purposes of UK disclosures (OECD TP Guidelines 2017 s E2 (4.102).

However, if an EU intermediary based in another member state was providing relevant services in relation to such an arrangement, then they may consider that this is disclosable.

Applying the rules to non-tax specialists

Analysing arrangements against the hallmarks is hard enough if you are a tax specialist. Advisors who are not from a tax background find it even more difficult to do effectively. For example, even tax specialists will not find it easy to determine whether the intangible asset they have helped move was ‘hard-to-value’ or whether the loan they have helped implement is creating two levels of double tax relief. It will be considerably more difficult for people who are not tax specialists to do this.

As a result, tax specialists may need to spend time developing procedures to help their non-tax colleagues comply with DAC6.

Poland

We conclude with a brief examination of the Polish implementation of EU MDR. These are of practical interest to UK practitioners and businesses. Poland has decided to make these rules extra-territorial, and as a result they can apply directly to non-Polish persons who are providing services which impact Poland.

Other concerning aspects to note:

- The rules are fully applicable now; i.e. the 30 day disclosure deadline has been in place since 1 January 2019.

- The Polish authorities interpret the DAC6 hallmarks very strictly and the Polish legislation have added four very broad hallmarks (in addition to the DAC6 hallmarks) with no main benefit test protection.

- The Polish rules primarily target individuals and the most severe penalties (criminal sanctions with fines up to about £4.5 million) apply to individuals.

- The Polish authorities consider that individuals working for non-Polish taxpayer group companies (e.g. tax and finance teams employed by a non-Polish head office) can be intermediaries and the obligations and potential sanctions in the Polish rules can apply to those individuals.

Given the above, we recommend that intermediaries and taxpayers adopt very strict protocols when providing any advice or services relating to Polish businesses

or activities.

How to cope with DAC6?

Given these complexities, how should advisers and businesses deal with DAC6? Consider implementing the following actions, depending on what is reasonable in the context of their business and/or the risks they face:

- Identify a central team within the organisation to take ownership of getting ready for DAC6.

- Undertake an impact assessment to better identify parts of your business which could be most affected

- by the rules.

- Implement governance protocols to ensure that higher risk events are identified and reported to your central team.

- Depending on the complexity of your organisation, consider whether you would benefit from software to help you track and analyse cases, manage workflow and ultimately allow you to report disclosable events.

In addition, when you are involved in a transaction with a number of different parties, you should also undertake the following steps:

- Discuss DAC6 with other parties involved in a transaction early in the process.

- Make sure you understand what role each party is performing and who is likely to be an intermediary.

- Consider whether it would be beneficial to have one party coordinate/manage DAC6 issues – perhaps monitoring trigger points, producing a central analysis for others to review and potentially making a disclosure that other promoters can rely on (if that is possible).

- Keep DAC6 on the agenda so that trigger points are not missed and any disclosures are made on time.