Turbulent seas

Share this article

Robert Pullen and Denise Yau provide an update on recent developments affecting the taxation of UK property

Key Points

What is the issue?

From 6 April 2019, UK tax is being extended to all disposals of UK property, including where held through a corporate structure. In addition, from 6 April 2020 there will be accelerated tax payment deadlines.

What does this mean to me?

The rules are complex and with such tight reporting and payment deadlines, it is imperative that owners of UK property are aware of the changes and how it affects the structures through which property is held.

What can I take away?

Disposals of UK property are now almost always subject to UK tax. Be ready to advise on the timings for reporting transactions and also the most beneficial method of calculating the gain.

Following a raft of successive piecemeal changes to the Capital Gains Tax (‘CGT’) regime over the years (see the article Over Baked in the May 2017 issue of Tax Adviser), TCGA 1992 Part 1 has finally been rewritten in an attempt to rationalise the provisions, as well as introduce the new rules which were included in Finance Act 2019.

Since 6 April 2013 UK residential property ‘enveloped’ in a corporate vehicle has been subject to ATED-CGT. In addition, since 6 April 2015 most non-UK residents have been within the scope of UK CGT for disposals of UK residential property. The provisions within Finance Act 2019 cast the net even wider. It should be noted that these rules are generally for property investments only; different rules apply for trading transactions, such as property development, which are not covered in this article.

There are two main changes. Firstly, the CGT regime for non-UK resident persons was extended from 6 April 2019 to include commercial property and ‘indirect disposals’. ATED-CGT was abolished altogether, with companies now subject to corporation tax instead. This means companies that were previously within ATED-CGT are effectively receiving a 9% tax cut and an extra two years rebasing (covered later in this article). Overall however, according to government forecasts the tax coffers are expected to be boosted by an estimated £455m from 2019/ 20 to 2022/ 23.

Secondly, from 6 April 2020 the payment date for CGT due on disposals of UK property will be accelerated for both UK residents and non-UK residents.

The government’s stated rationale behind these changes is to ‘level the playing field’ between UK and non-UK residents who hold UK property as well as to ‘simplify’ the existing tax rules. HMRC have published 45 pages of draft guidance in an attempt to explain the c.120 pages of new legislation, however the new rules are so complex that the average taxpayer will struggle to follow without the help of a professional adviser. More importantly, will those who are unrepresented even be aware of these changes?

Let us now look at some of the detail behind the headlines.

How will the capital gain/loss be calculated?

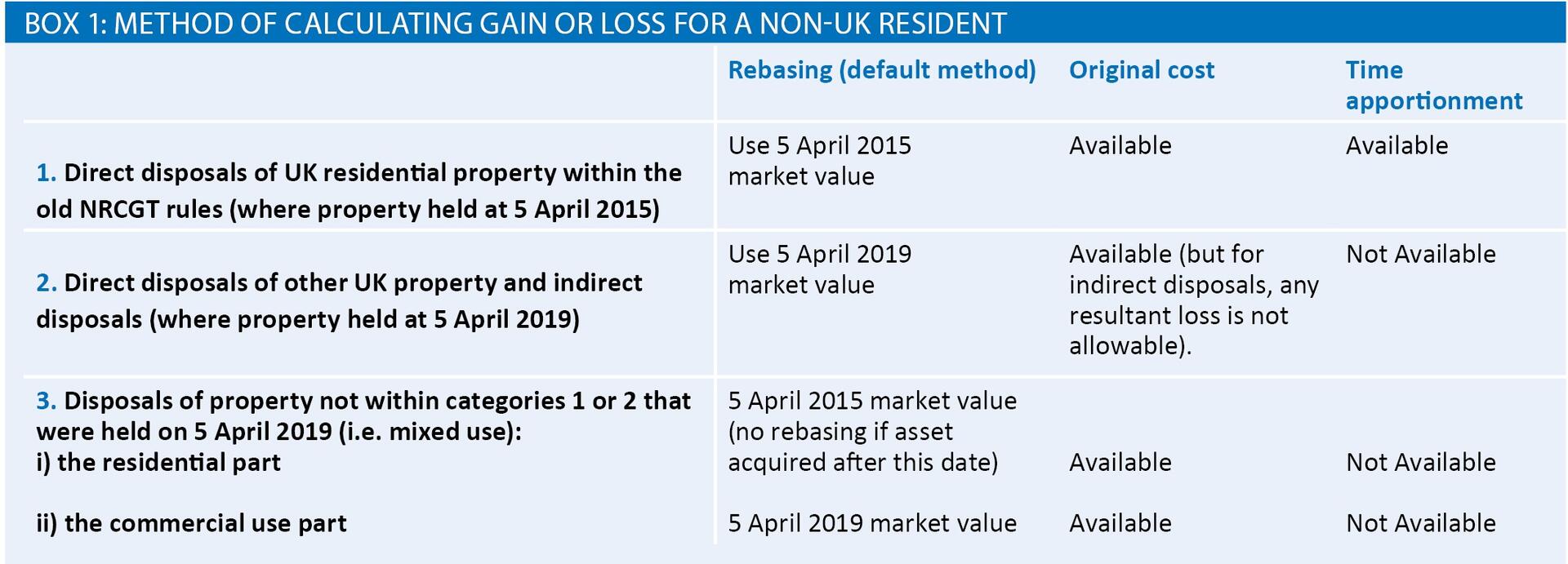

Residential property which has always been within the scope of CGT is unchanged, with rebasing available to 6 April 2015 as well as the option to elect for original cost or time apportionment methods.

For UK property brought into the CGT regime for the first time (i.e. commercial property, indirect disposals and certain non-UK resident persons who were not previously caught), rebasing is available to the market value as at 5 April 2019 (default). It is also possible to elect to use the original cost instead, but (strangely) any capital losses that arise using this method will not be allowable if realised on an indirect disposal.

The rules in relation to mixed use properties are harder to follow; however the overall effect is for the commercial part to be rebased to 5 April 2019, and for the residential part to continue to be rebased to 5 April 2015. In both cases an election is available to use the original cost.

It is important to note that the time apportionment method of calculating the gain is only available for the ‘old’ rules, i.e. a residential property owned prior to 5 April 2015. UK properties coming into the charge to CGT for the first time now are not able to take advantage of this method, and also the residential part of a mixed use property no longer qualifies.

Box 1 summarises the different ways of calculating the gain.

It should also be noted that whilst companies will be subject to UK corporation tax going forward, the gain chargeable is still calculated using the rules in TCGA, so rebasing is available as above.

To prevent non-UK resident companies being dissuaded from migrating to the UK, where UK property is held by a non-UK company at 5 April 2019 but a disposal is made after becoming UK resident, rebasing continues to be available.

What is an indirect disposal?

This is one of the most complicated and contentious areas of the new legislation. An indirect disposal is when a non-UK resident makes a disposal of a ‘property rich company’ in which they held a ‘substantial indirect interest’.

Broadly, a property rich company is one in which at least 75% of its value is derived from UK land.

A substantial indirect interest is held where a person and any persons connected with them (as defined in TCGA s286) collectively hold a 25% investment in the company at any point in the two years ending with the date of disposal.

There are some useful exemptions, including for trading companies that meet the relevant criteria.

There are also complex provisions for UK property rich ‘collective investment vehicles’ but these rules are outside the scope of this article.

When will a CGT return be required?

From 6 April 2019, non-UK residents will have to file a CGT tax return whenever there has been a disposal of UK land (directly or indirectly) regardless of whether a gain or loss is realised.

From 6 April 2020, UK residents will also be required to file a CGT return when a direct disposal of UK residential property has been made realising a gain.

In both cases, the CGT returns need to be filed within 30 days of the completion date. There are serious concerns whether this will provide taxpayers and advisers with sufficient time to prepare the calculations.

There is, however, one silver lining: taxpayers will no longer need to register and deregister for Self-Assessment just to report a disposal of UK land or property, as a CGT return is sufficient to meet the filing obligations.

Companies will need to file a corporation tax return in line with the usual deadlines.

Payments on account

Along with a CGT return within 30 days, payment of the CGT is also due on the amount ‘notionally chargeable’, although until 5 April 2020 non-UK residents can continue to defer payment where a Self-Assessment tax return is filed.

Individuals will pay tax on the gains on direct disposals of residential property at 18/ 28% and on non-residential and indirect disposals at 10/ 20%, whereas corporates will pay at corporation tax rates.

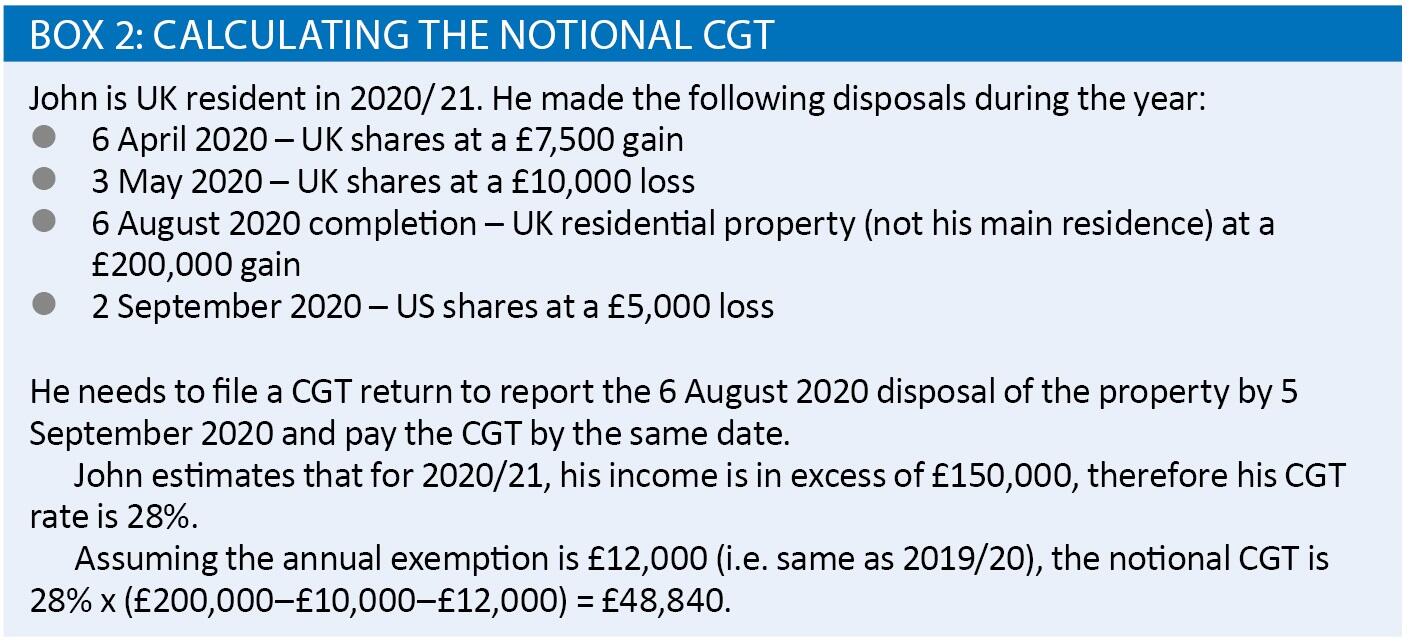

The notional CGT is the tax that would be payable for the tax year had it ended with the date of disposal. Broadly, this includes gains on disposals of UK property within the scope of CGT, and also any unused capital losses that have been realised by the completion date of the disposal – see box 2 for an example.

For non-UK residents, only previous losses on UK land or indirect disposals may be taken into account.

Inevitably, estimates of an individual’s income will be required in order to work out the applicable CGT rate. Whilst amendments may be submitted if it transpires that the estimates were incorrect, this does add to the administration and professional costs.

Furthermore, when more than one CGT return is filed in a tax year, the notional CGT will need to be recalculated each time and compared with the payments on account already made. The taxpayer will then either make another payment on account to ‘top up’ or obtain a refund as appropriate.

Some taxpayers may experience cash flow problems in cases where the CGT has to be paid substantially earlier compared to the usual Self-Assessment deadlines. There may also be allowable losses incurred after the completion date that can only be claimed in a subsequent CGT return (if there is another disposal of UK property in the year) or in a Self-Assessment tax return, which could be up to 12 months later.

Concluding thoughts

The rewritten TCGA does simplify some aspects. However, the new legislation can be difficult to interpret and apply in practice. Whilst the government may be attempting to level the field, there is separately an ongoing consultation on a proposed 1% SDLT surcharge for non-UK residents buying residential property in England and Wales. The only certainty in these turbulent times seems to be the government’s inability to stop tinkering with the rules on UK property! Will any of these changes ultimately affect the UK property market? Only time will tell.