The UK tax rules governing the trading of emissions allowances

Share this article

Caps on the greenhouse gases that can be emitted by certain businesses encourage the reduction of total emissions. We examine the UK tax rules governing the trading of emissions allowances.

Key Points

What is the issue?

Emissions trading is a market based approach to controlling the production of carbon dioxide and other greenhouse gases.

What does it mean to me?

There are caps on the total amount of certain greenhouse gases. Affected businesses can buy or receive emissions allowances, which they can trade with one another as needed.

What can I take away?

With the exception of VAT, there are no specific UK tax rules and very little guidance covering emissions credits.

Emissions trading is a market based approach to controlling the production of carbon dioxide and other greenhouse gases. Since carbon dioxide is the principal greenhouse gas, many people speak simply of trading in ‘carbon’. Both mandatory and voluntary emissions trading schemes exist.

Perhaps the most common example of a mandatory scheme is the European Union’s Emissions Trading System (EU ETS), launched in 2005 to reduce emissions in high carbon-emitting industries. Similar systems operate in New Zealand, China, parts of the US and Canada, and the UK following the UK’s departure from the EU.

The EU and UK ETS schemes work on the ‘cap and trade’ principle. There are caps on the total amount of certain greenhouse gases that can be emitted by the businesses covered by the system and they are organised by sector. Within the caps, affected businesses buy or receive emissions allowances, which they can trade with one another as needed. The cap is reduced over time to encourage the reduction of total emissions and the use of abatement technology. Non-compliance, as a result of having insufficient allowances, results in financial penalties.

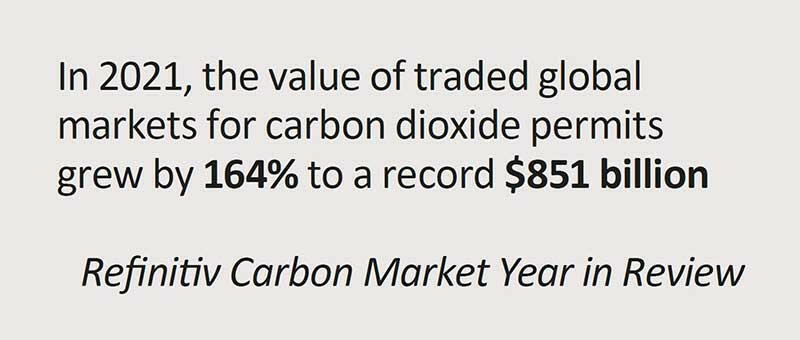

An allowance under a cap and trade scheme is equivalent to one tonne of carbon dioxide. This is an increasing priority for firms, as shown by the traded global markets for carbon dioxide permits growing by 164% to a record $851 billion in 2021 (see http://reut.rs/3iSEX1o).

Voluntary emission trading

The voluntary carbon market operates outside but in parallel to the mandatory market, and entails the creation and acquisition of verified emission reduction (VER) credits. Each VER represents one metric ton of reduced, avoided or removed carbon dioxide or equivalent greenhouse gases.

These VERs are created when a project developer establishes a relevant project such as planting trees, avoiding deforestation, direct carbon capture or community based initiatives, such as replacing old cooking equipment with more environmentally friendly alternatives.

The VERs are sold by the project developers and purchased – often through traders or exchanges – by individuals and businesses seeking to offset their carbon emissions. Because participation in such schemes is voluntary, most purchasers are motivated mainly by environmental, social and governance (ESG) and reputation management.

VERs are verified by an independent third party based on their published standards, such as the Verified Carbon Standard (Verra) and the Gold Standard.

The size of this global market is relatively small in comparison to the compliance markets, at some $1 billion (see bit.ly/3K0Fb2f). However, recent research estimates that this market is set to grow some 30% year-on-year, reaching $250 billion by 2030 and potentially $1 trillion by 2050, as more and more companies seek to fulfil net zero emissions pledges.

The UK corporation tax treatment of emissions credits

With the exception of VAT, there are no specific UK tax rules and very little guidance covering emissions credits. Therefore, the tax treatment is determined by the application of general rules and depends on the role a business is playing.

Selling emissions credits

Income derived by businesses selling surplus UK ETS allowances is taxable for corporation tax purposes. There is also a supplementary charge and petroleum revenue tax for oil and gas companies (see HMRC’s Oil Taxation Manual OT20400). Businesses selling voluntary emissions credits as part of their trade will also generate taxable income for corporation tax purposes.

Trading emissions credits

UK based commodity traders with a trade of dealing in emissions credits (perhaps as part of wider commodity trading) are likely to be subject to corporation tax on their trading profits in the usual way.

Buying emissions credits

On first principles, in order for an expense to be tax deductible, it has to be incurred wholly and exclusively for the purposes of the trade. The purchase of allowances under a mandatory scheme should therefore be deductible.

To obtain a deduction for the purchase of credits under a voluntary scheme, it will be important to demonstrate and document the business rationale for incurring the expenditure. This could be, for example, to demonstrate climate/corporate responsibility and support the brand, and for this to feature as part of the business’s customer relations communication.

In terms of the timing of any tax deduction, in the absence of any other specific tax rule, the tax treatment should follow the accounts. For example, if the emissions credit cost is included as part of the product cost, a corporation tax deduction would not be available in the period in which the purchase is made. Instead, tax relief should be available once the product is sold and the expense should be charged to the income statement as part of the cost of goods sold.

Fines incurred for failing to comply with UK or EU ETS rules are not deductible.

The UK VAT treatment of emissions credits

The VAT treatment differs between mandatory and voluntary credits:

- The sale of compliance market credits (i.e. those that are mandatory) is a supply of services which are subject to VAT.

- The sale of VERs is outside the scope of UK VAT.

HMRC’s view is that compliance market credits are considered to be capable of consumption of the type envisaged by the VAT system, whereas the latter are not. As VAT is a tax on consumption, the sale of compliance market credits is a supply of services which is subject to VAT (currently at the 20% standard rate), whilst VERs are outside the scope of VAT. HMRC’s guidance at VATSC06584 states:

‘A verified emission reduction (VER) is essentially a promise that carbon has been or may be reduced somewhere in the world. There may be a general benefit to the reputation of a business (good PR, marketing and corporate responsibility) in paying for a VER, but no particular service is rendered which can be identified as a cost component of the business. There is therefore no consumption. No service is being provided to an identifiable consumer and no benefit is being provided which is capable of forming a cost component of the activity of another person in the commercial chain.’

That is to say, whilst payment for a VER might produce a general social benefit (or, at least, the creation of the VER would be as a result of a social benefit), it might produce a specified result or it might give rise to a legal relationship with reciprocal obligations. A person’s income falls within the scope of VAT only if it constitutes the consideration for a supply of goods or services to a consumer (or a payment for consumption, as per HMRC’s guidance noted above). The mere fact that someone may benefit from making a payment (for example, through an improved public relations profile), or something is or may be done in exchange for a payment, is insufficient to bring such a transaction within the scope of the VAT system. The public at large cannot constitute a specific recipient of the kind which must exist in order to give rise to a transaction chargeable to VAT.

Missing Trader Intra-Community fraud

It is worth noting that the EU ETS has been affected by fraud involving the theft of VAT (also known as carousel fraud or Missing Trader Intra-Community fraud). In the UK, in June 2012 three defendants were found guilty of carbon trading carousel fraud and jailed for a combined total of 35 years. It is estimated that €41 million of VAT was stolen during 69 days of trading (see bit.ly/3Dy6U83).

Following EU wide consultation and the introduction of a zero-rate for commissions trading in the UK as a temporary measure, anti-avoidance measures have been introduced in the form of a domestic reverse charge, to help to remove the risk of such a fraud being perpetrated in the future.