An unintended pitfall?

Share this article

Cassandra Graham considers the legislative oversight for business asset gift relief on a transfer of shares

Key Points

What is the issue?

When gifts of shares in a trading company are considered, there are two restrictions which impact claims for business asset gift relief under TCGA 1992 s 165. The first restriction is in relation to the trading status of the company/group. The second restriction and focus of this article is that where a trading company owns non-business assets, relief can be restricted but this only takes into account chargeable assets.

What does it mean for me?

Where a company owns non-business chargeable assets and assets which are not chargeable assets such as intangible assets, care needs to be taken when calculating the gain eligible for gift relief as the application of the non-business asset restriction can result in unexpected tax charges.

What can I take away?

When considering the gift of shares in a trading company and the application of s 165, ensure that the asset base of the company is considered in detail.

There are many reasons why a shareholder may give shares away, including as part of a succession plan to provide continuity for the business and its management in the future, to pass the business ownership on to the next generation in the family or as part of a wider inheritance and estate planning exercise.

Business asset gift relief is available to defer the capital gain on gifts of qualifying business assets between parties through a joint election. Its effect is to defer the capital gains tax due on the gift until such time as the recipient disposes of the asset. This prevents dry tax charges on gifts otherwise assessed at market value and is a useful tax planning tool in every tax advisor’s armoury, provided the pitfalls are known.

The relevant legislation is the Taxation of Chargeable Gains Act (TCGA) 1992 s 165. Qualifying business assets include shares (or securities) in a trading company or holding company of a trading group. As specified by TCGA 1992 s 165(2)(b), the company has to be an unlisted trading company or the transferor’s personal trading company. Personal trading company in this context is where a shareholder holds at least 5% of the voting rights. As unlisted companies are included, shares in most privately owned trading companies fall into these provisions. For the purposes of simplicity, references to ‘shares in a trading company’ within this article include all of the definitions above.

Other assets qualify as well as shares but for the purposes of this article the focus is on the transfer of shares in a trading company and a specific consequence that arises due to the way the legislation is drafted. In particular, this article focuses on a company which has ‘hybrid’ trading and investment activities and assets.

Gift relief restrictions

When gifts of shares in a trading company are considered, there are two restrictions that impact relief claimed under s 165. It is important to highlight that these restrictions do not apply when considering gift relief under TCGA 1992 s 260 for transfers into and out of a trust. This may lead to the use of trusts as an alternative means of transferring shares where the following restrictions are in point.

Firstly, the company has to be a qualifying trading company (or the holding company of a trading group). A trading company is a company carrying on trading activities which do not include, to a substantial extent, activities other than trading activities. A trading group of companies is one where at least one of its members carries on trading activities; and, if the activities of all of the group members are taken together, they do not include, to any substantial extent, non-trading activities.

HMRC’s view is that substantial for these purposes is taken to mean 20% or more. Broadly, a company cannot carry on investment activities that represent more than 20% of the overall company activities. However, a notable caveat to this is that 20% is not defined by the legislation and given recent case law this 20% test is now under question. This 20% test was considered in two recent (non-binding) First-tier Tribunal cases, both in relation to business asset disposal relief. In Potter & Anor [2019] UKFTT 554, the judge decided that the company was substantially a trading company despite significant investment assets, which could have been used to support the business. In Assem Allam [2020] UKFTT 26, the judge did not accept either the 20% test, or a proposed 50% test put forward by the taxpayers’ counsel – but still concluded that the company had substantial non-trading activities.

Multiple indicators are considered ‘in the round’ such as gross assets, management time and expenses, turnover, profitability, overall context of the business and business history when assessing whether the company carries on non-trading activities to a substantial extent. When considering a ‘hybrid’ company, the question of whether the shares even qualify as those of a trading company is the essential starting point, as otherwise business asset gift relief is irrelevant, along with the second restriction to be considered.

The particular quirk in the legislation and main focus of this article is the second restriction, referred to as the ‘non-business asset restriction’. This is the restriction of gift relief where the trading company owns investment assets or assets not used in the trade which are chargeable assets. Confusingly, these provisions are contained in a different part of the legislation at TCGA 1992 Sch 7 Part 2 para 7 and could be missed in their entirety if it was not for the knowledge that they exist.

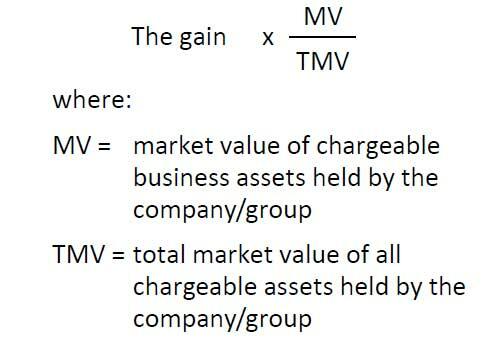

In this scenario, the gain that can be heldover when claiming business asset gift relief on a transfer of shares in a trading company is restricted by reference to the value of non-business chargeable assets held by the company. The gain eligible for gift relief is calculated as:

What is the issue?

The issue to be focused on is that the restriction only refers to chargeable assets. Therefore, where the company owns other assets and most notably intangible assets such as goodwill created or acquired after 1 April 2002 (commonly referred to as ‘new goodwill’) there can be an odd result. As the restriction includes the value of the chargeable assets, it is the market value of the chargeable assets at the date of the gift, including those which may not necessarily be recognised on the balance sheet. The impact of the issue with the non-business asset restriction is most easily demonstrated by way of examples.

Example 1: Gift of shares where company owns ‘old goodwill’

Rodney owns shares in a trading company, Trotters Ltd, which was incorporated in 1990. Due to its successful trading performance, profits have been reinvested over time in purchasing investment property, such that the company has built up a rental portfolio.

Trotters Ltd owns investment property worth £2 million and the goodwill associated with the trade has also been valued at £8 million. As the goodwill was created prior to 2002 (commonly referred to as ‘old goodwill’), it is considered a chargeable asset for tax purposes. No other chargeable assets are owned by Trotters Ltd. For the avoidance of doubt, Trotters Ltd is considered as a trading company when looking at all tests in the round.

Rodney gifts a 10% shareholding in Trotters Ltd to Derek, worth £250,000, inclusive of an appropriate minority discount. The base cost of the shares is £10 resulting in a gain of £249,990. When considering the restriction, the gift relief available is:

£249,990 x £8m/£10m = £199,992

This reduces the gain chargeable to capital gains tax to £49,998.

Example 2: Gift of shares where company owns ‘new goodwill’

The facts are same as the above but Trotters Ltd was incorporated in 2005.

As the goodwill associated with Trotters Ltd was created after 1 April 2002, it is within the intangible fixed assets regime for corporation tax purposes and it is not a chargeable asset for the purposes of the restriction. The gift relief available is:

£249,990 x £0m/£2m = £0

No gift relief will be available and the gain chargeable to CGT is £249,990 and assessed in full.

Example 3: Gift of shares where company owns ‘new goodwill’ and chargeable business assets

The facts are the same as Example 2 in that Trotters Ltd was incorporated in 2005 but instead of the £2 million of investment property, the company owns £2 million property assets used in the business (even if this business use is just at the time of the gift).

The gift relief available is:

£249,990 x £2m/£2m = £249,990

Full gift relief would be available to reduce the gain to nil and the restriction would not apply.

A complex arrangement

The above three examples are overly simplified for the purposes of demonstrating the issue in question but they do outline the absurd outcome of the legislation.

In reality, where a company has a more complex asset base and has purchased goodwill or created goodwill (or other intangibles) both before and after 2002, the implications are more complicated, but the overall impact would be the same.

In theory, a trading company which holds intangible fixed assets and no chargeable assets used in the business could technically own as little as £1 of non-business chargeable assets and no gift relief would be available for the shareholder when gifting shares in the company.

As s 165 predates the intangible fixed assets regime, it seems clear that this was not the intended result as it disadvantages owners of newer businesses. It can only be concluded that this is an inadvertent oversight when the intangible fixed assets regime was introduced which has never been rectified.

However, the implication is that it is an issue which is likely to become more prevalent in practice when shareholders consider ownership succession of ‘hybrid’ companies which have been established or purchased valuable goodwill after 1 April 2002.

A costly workaround

When considering whether a company is a trading company for the purposes of business asset gift relief, it is strictly a snapshot test at the point of the gift. This is caveated by the fact that one of the factors to be considered is the overall context of the business and its history, which may create complexities in this analysis in a borderline case.

However, provided that ‘in the round’ the company is a trading company, one possible solution to the non-business asset restriction is that all of the non-business chargeable assets could be sold by the company immediately before the gift of shares. As the non-business asset restriction is equally only applicable at the point of the gift if no non-business chargeable assets were held, no restriction would apply and the gain can be heldover in full under s 165.

However, this is not only likely to result in an expensive corporation tax bill for the company; it is also debateable whether this would be commercially viable, especially if the intention was to reacquire the assets after the gift. Given that corporation tax at 19% on the resulting chargeable gains is likely to be a marginal saving to the capital gains tax triggered on a disposal of shares, it may not be worthwhile.

It may also be that the resulting gain on the disposal of shares after taking account of the non-business asset restriction would qualify for business asset disposal relief and be taxable at 10% personally in any event. However, the capital gains tax would have to be funded personally after triggering tax on extraction, so it is likely to be more tax efficient for the company to pay the tax unless the individual has cash available to fund the capital gains tax.

Ultimately, the issue is the application and drafting of the business asset gift relief legislation. The workaround outlined above is far from ideal in most circumstances and feels somewhat of a sticking plaster rather than addressing the real issue and achieving a solution.

Call for evidence

Last July, the chancellor asked the Office of Tax Simplification to undertake a review of the capital gains tax regime and reports have been published in November 2020 and May 2021. The outcome of this review is likely to result in changes to capital gains tax. It therefore now seems more appropriate than ever to consider whether legislative issues such as this as it could be rectified as part of the overhaul.

Whatever the future may hold for the world of capital gains tax, this article highlights the importance of ensuring that the full ramifications across all of the taxes and all of the reliefs are considered when making changes to the UK tax system. Otherwise, there may be unintended consequences which have unfair and costly outcomes for the taxpayer and result in a system that ends up being more unwieldly rather than simplified.

As a member of the CIOT OMB Committee, it would be useful to know if any readers and CIOT members have come across this issue when considering the non-business asset restriction on gift relief in practice. We therefore request that any evidence is sent to [email protected] with the message of ‘Business asset gift relief, Tax Adviser (August 2021)’ in the subject line to prompt further discussion and action, where appropriate.