Upcoming EU VAT changes from 2025: untangling the puzzle

Share this article

We examine the VAT changes due to be brought into play in the European Union from 2025 and how they will work in practice.

Key Points

What is the issue?

Over the next few years, the EU will be modernising and simplifying its VAT procedures for cross-border transactions.

What does it mean for me?

Despite Brexit, UK businesses will be affected by the forthcoming changes, and will need to adapt their procedures and systems to remain compliant and take advantage of the simplification opportunities.

What can I take away?

The initial changes from 1 January 2025 will be to the rules on place of supply, single VAT registration, domestic reverse charge, and the call-off stock simplification. Further ahead, wider e-invoicing and digital reporting requirements will come into effect from the start of 2028.

Readers will no doubt be aware that VAT in the UK celebrated its 50th birthday this year, having first been introduced when the UK joined the European Economic Community in 1973.

Brexit means that the UK and EU VAT systems will now evolve independently of one another, with legislative packages such as the EU proposals for VAT in the Digital Age (ViDA) (which include changes to the platform economy, new digital invoicing and reporting requirements, and movement towards a single EU VAT registration) creating growing differences in the coming years.

Despite the UK’s divorce from the EU, the European VAT system remains of significant importance to UK-based businesses, as it defines the rules of engagement with our closest trading partner.

This article looks ahead at some of the EU VAT changes on the horizon and the practical impact they will have on UK businesses which continue to trade into the EU, focusing in particular on the place of supply and single VAT registration changes coming into force in 2025. It is important to note that few of these changes exist in isolation, and those discussed in this article will need to be considered by businesses in the round, alongside the broader package of proposals.

Whilst the ViDA changes are currently proposals and still require unanimous approval of the member states to enter into EU law, they are anticipated to be implemented as proposed, albeit with some of the practical application points yet to materialise – particularly in the case of more complex scenarios which do not neatly align with the situations the proposals intend to cover. The legislative text of these changes is in the proposed Council Directive 2022/0407(CNS).

1 January 2025: Place of supply changes

Whilst the forthcoming changes predominantly impact those trading in goods, the modernisation of the place of supply rules in respect of business-to-consumer (B2C) virtual events, education, entertainment and similar activities merits a discussion.

At present, businesses providing virtual events (for example, a UK business providing live online cooking classes where the participants can interact with the instructor in real time) have three UK/EU rules they need to think about:

1. The basic rule: B2C supplies of services are taxed where the supplier belongs.

2. The electronically supplied services (ESS) rule: B2C electronically supplied services are taxed where the consumer belongs.

3. The ‘where performed’ rule: B2C supplies of entertainment, education or similar events are taxed where the event takes place.

As the example service appears to involve more than the ‘minimum level of human intervention’ required by the electronically supplied services definition, rule number two can be disregarded for now. While EU case law in Geelen (Case C-568/17) helps us to understand the concept of where an online event actually takes place, a more complex offering by this business involving both live and pre‑recorded sessions sees the service appearing to land between the latter two rules. Although taxing events where they take place was perfectly sensible at a time when you could clearly point to the physical place where they were occurring, this approach to taxation hasn’t kept pace with an increasingly digital economy.

Fortunately, the position is clarified from the start of 2025, when such services which are streamed or made available digitally will become taxable where the consumer resides. This change provides welcome clarity, and dispels the need to consider the somewhat vague and inconsistently applied ESS definition.

The immediate impact is that UK businesses – such as our aforementioned cooking tutor – providing non-ESS services to EU-based consumers, will trigger VAT registrations where their customers are based. The place of supply will be where the customer belongs, and the EU applies a nil turnover registration threshold for non‑established businesses.

This initially suggests an onerous compliance burden, but the One Stop Shop scheme allows businesses to set up a simplified VAT registration with their tax authority of choice, and to report certain sales in all EU member states through a single quarterly filing.

1 January 2025: Single VAT registration

Coinciding with the place of supply changes is the introduction of a new VAT reporting scheme (to operate in parallel with the One Stop Shop) and EU domestic reverse charges. These changes broadly aim to reduce the administrative burden of trading in the EU by reducing the number of separate VAT registrations that a business will require, with a view to increasing compliance overall.

Single VAT registration: a wider scope

Movements of a business’s own goods between two EU member states are currently a ‘deemed dispatch’ from the first country and a ‘deemed acquisition’ into the second. Even if no sales to third parties are made in either country, the business will still need to maintain active VAT registrations in both.

For businesses which commonly need to move their own goods across the EU, such as those in the manufacturing or life sciences sectors which may have complex supply chains, the VAT reporting of movements of own goods alone can represent a large compliance and administrative burden.

Under the ViDA proposals, from January 2025 a new reporting scheme will be introduced to enable movement of own goods to be reported through a single simplified return. This will remove the need for businesses to register for VAT in individual member states solely for the purposes of reporting movements of own goods.

The scheme will also begin to cover the supply of installed or assembled goods in the EU (e.g. the sale of plant and machinery which is installed at a customer’s premises) from the start of 2025. Currently, this ordinarily creates an obligation for UK businesses to register for and charge local VAT in the country where the goods are being installed, particularly with the loss of the pre-Brexit simplification that was historically available.

Although these changes represent a significant step forward towards a single VAT registration in the EU, they exclude business-to-business (B2B) transactions for the time being, due to concerns around the recovery of VAT and potential abuse.

Single VAT registration: practicalities

As with the One Stop Shop, the new movement of own goods reporting scheme is by no means compulsory; however, it offers an attractive administrative simplification for those trading in the EU.

Businesses established outside of the EU are expected to be free to register for the scheme in any EU member state of their choice and, once registered, the scheme’s simplified returns are to be filed with the tax authorities in the member state of registration on a monthly basis.

It is vital to note that there is no ability to deduct input VAT through this new scheme. This means that businesses which expect to incur local input VAT in the course of their activities may still need to consider the need for a stand-alone VAT registration as a means of obtaining VAT refunds.

The need for a stand-alone VAT registration is likely to be greater for those businesses incurring a significant amount of import VAT when moving their stock into the EU.

Domestic reverse charge

Whilst B2B transactions are excluded from the remit of the new single VAT registration reporting schemes, January 2025 should also see the mandatory introduction of domestic reverse charges across the EU.

At present, EU VAT law allows member states the option of introducing domestic reverse charges to cover supplies of goods by non-established businesses to VAT registered businesses. Member states such as France, Italy and the Netherlands have adopted these rules.

For example, for a UK business holding goods in France which it intends to sell to a French business that is VAT-registered in France, the basic expectation is that the UK business would need to charge French VAT (and become registered in France, if it hasn’t already). However, the existence of a domestic reverse charge means that the UK business doesn’t need to become VAT-registered or charge VAT on the supply, as the French VAT-registered customer will be responsible for self-accounting for VAT on their local VAT return.

Although removing the need to be VAT-registered in these member states will reduce the compliance burden for the UK business, it also removes the main mechanism by which input tax can be recovered.

In the absence of a VAT registration, input tax would need to be recovered by making refund claims directly to the relevant tax authority, where there will be a greater delay between paying VAT to a supplier and receiving the repayment.

Call-off stock simplification

The current intra-EU ‘call-off’ simplification, which allows businesses to hold stock in another member state for a specific customer without triggering a VAT registration obligation, is expected to be rescinded from the start of 2025. The introduction of the special scheme to cover movement of own goods, combined with the mandatory reverse charges, eliminates the need for such a simplification.

Businesses will have greater flexibility under the new rule set, as goods can be moved from an EU warehouse to other member states, and sold to any other VAT-registered person without triggering an additional registration obligation. Currently, the call-off stock simplification only produces this outcome where the identity of the customer is known prior to the good’s movement.

Case study: how these changes work in practice

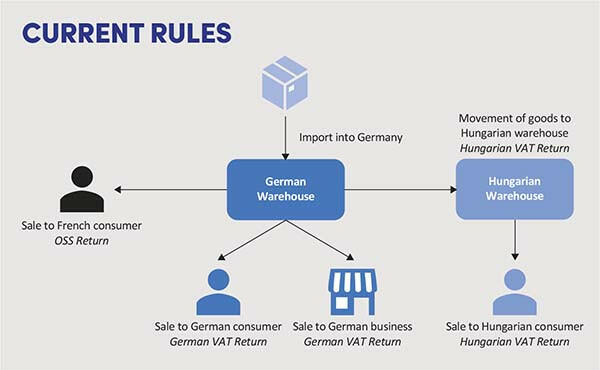

To illustrate the practical impact of these changes, let’s look at an example involving a UK-based shoe manufacturer which sells both retail and wholesale within the EU.

Our business imports the goods into Germany and stores them within a German warehouse where they are sold to German businesses, German consumers and consumers in other EU member states. It also regularly moves stock from Germany to a Hungarian warehouse to supply the local Hungarian market.

The current rules are shown above. Currently, only the distance sales directly from the German warehouse to consumers in other EU member states can be reported on the One Stop Shop return. The sales within Germany must be reported on the company’s German VAT return, and a separate Hungarian VAT registration is required to report the movement of goods to the Hungarian warehouse and sales made therefrom.

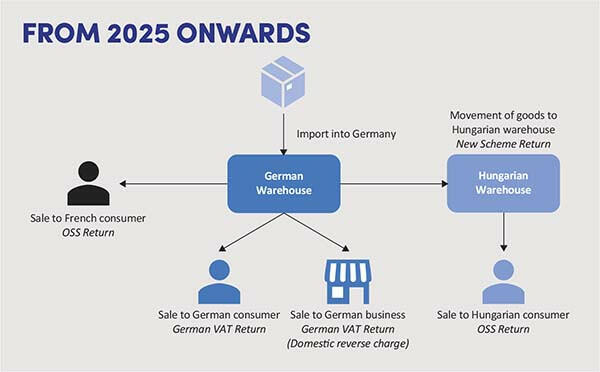

The rules from 2025 onwards are shown above. Under the ViDA proposals, from 1 January 2025 the movement of goods to the Hungarian warehouse will be reportable under the new scheme. The subsequent sales from that warehouse will be able to be reported through the One Stop Shop scheme, removing the need to maintain a Hungarian VAT registration. Assuming that our UK business is not established in Germany, it will no longer need to charge local VAT on its sales to German businesses, as its customers will become responsible for accounting for VAT. If the business needed to react quickly to demand, and move goods from either inventory to a separate Czech warehouse, it would also be able to do without any new VAT registration obligations arising, as the movement can be reported through the new scheme.

The overall picture following these changes is simpler and should be easier to manage from a compliance perspective, but the business is now carrying out sales under a number of different regimes (ordinary domestic sales, domestic sales subject to the reverse charge, movements of own goods under the new scheme, and One Stop Shop sales from different member states).

In order to prepare for these changes, our UK businesses will need to look to their tax coding and processes to ensure that their systems are able to correctly identify the right VAT treatment for each transaction type and that the transactions can be accurately identified and reported through the appropriate return.

Conclusion

Businesses trading within the EU should expect significant changes in the coming years, as the EU commission looks to modernise its VAT system whilst simultaneously tackling non-compliance. However, the developments outlined above are only part of the picture, as the single VAT registration proposals go hand in hand with wider e-invoicing and digital reporting requirements which will come into effect from the start of 2028.

The latter represent a fundamental change to how many intra-EU transactions are reported, and deserve a full discussion in their own right.