VAT and property: clearing up myths and common mistakes

Share this article

We dispel some myths and common mistakes that are sometimes made on property deals and builder services.

Key Points

What is the issue?

The VAT rules for land and property and construction services are complex and often involve large sums of money. It is important that clients and advisers consider the relevant issues before a project starts to ensure the legislation is applied correctly.

What does it mean for me?

If a developer or property owner cannot fully claim input tax, the reduced 5% VAT rate on some builder services can save a lot of money. The article explains when 5% rather than 20% is charged.

What can I take away?

The sale of a partly tenanted building will be outside the scope of VAT as a transfer of a going concern if the rental income is earned on a commercial basis, and the other transfer of a going concern conditions are met. This will produce a saving of stamp duty land tax for the buyer because it is charged on the VAT inclusive cost of a building.

VAT and property is a nightmare topic for clients and advisers. It is also probably the most important one to get right because of the amount of tax involved in many deals. It is a classic case of when you can easily get bitten in the shark-infested waters of the nation’s favourite tax.

In this article, I will make some statements about VAT and property to clarify some of the cloudy issues that can cause sleepless nights for clients and advisers. It is important to get the VAT right before a deal takes place; it is difficult getting the greyhound back in its trap once it has started chasing the hare.

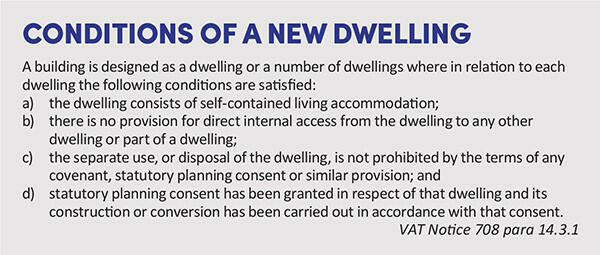

Builder services on new dwellings are zero-rated but you need to be clear about the definition of a ‘dwelling’.

If a farmer decides to build a bungalow next to the farmhouse on his farm – perhaps for a relative to live there – will builder services to construct the bungalow be zero-rated because they relate to a new dwelling?

For zero-rating to apply on construction services, the new building must meet four conditions of a ‘dwelling’, as stated in Value Added Tax Act 1994 Sch 8 Group 5 Note 2. See Conditions of a new dwelling.

However, the reality of this project is that it will almost certainly be a condition of the planning consent that the main farmhouse and new bungalow can only be sold at the same time as a single package. The third bullet point has failed, meaning that builder services are standard rated. Although the new bungalow will look like a new dwelling – and be treated as such by the farmer – it is classed as an extension to an existing dwelling as far as VAT is concerned.

The 5% rate on builder services includes residential conversions where the number of dwellings is reduced as well as increased.

The reduced VAT rate of 5% applies to construction services carried out on certain residential conversions. For example, it applies to building work carried out on a dwelling that has not been lived in for at least two years and the conversion of a non-residential building into a dwelling; e.g. a pub converted into a house. It is also relevant when a project produces a change in the number of dwellings.

I was always mystified by the fact that the law change in 2002 applied the reduced rate to a ‘change’ in the number of dwellings rather than an ‘increase’. Why would Parliament reward a project that reduces the number of dwellings; for example, by converting two semi-detached houses into a detached mansion?

In my opinion, this makes as much sense as asking a busker playing a didgeridoo to perform at a world class symphony hall but we must not complain because it produces a welcome tax saving for property owners that cannot claim input tax.

A partly tenanted property can still qualify as a transfer of a going concern when it is sold.

Imagine the following situation: you have traded from an office for seven years and are now selling the freehold of the building. You opted to tax the property when you purchased it because you sublet the top floor of your four-storey building. The tenant will remain in situ after the sale.

Advisers sometimes think – incorrectly – that the top floor will qualify as a transfer of a going concern; i.e. being relevant to a property rental business. They think that therefore no VAT will be charged on 25% of the selling proceeds, while the other three floors will be the sale of an empty building, which is standard rated because of the option to tax election. However, the good news is that the entire sale will qualify as a transfer of a going concern if the rental arrangement with the tenant is made on a commercial basis, rather than a peppercorn rent. The buyer must also opt to tax the property and meet the other TOGC conditions specified in the legislation. This outcome also produces a welcome saving of stamp duty land tax, which is charged on the VAT inclusive price of a sale (see VAT Notice 700/9 s 6).

An absorbing First-tier Tribunal case about the twists and turns of a property sale and the transfer of a going concern rules involved the Haymarket publishing company in Haymarket Media Group Ltd [2022] UKFTT 168. The company sold their offices for £80 million to a developer and tried to claim it was a transfer of a going concern because there was a small amount of rental income being earned from the building. The directors also claimed that the company had partly started the construction work to convert the building into dwellings. However, the tribunal agreed with HMRC that the commercial reality was that the company was selling an empty property with an option to tax election in place, so the sale proceeds were standard rated.

Builders will not charge VAT for work on overseas buildings, even if they invoice a customer who is resident in the UK.

Let us pretend that I own a holiday home in Spain, a nice thought. If I ask a UK builder to travel to Spain and do some work on the home – perhaps fitting a new kitchen – the place of supply for his services will be Spain. The fact that he will address his invoice to my UK address is irrelevant. The place of supply for land services is where the work is carried out. If he charges me UK VAT, he has made an error.

However, this is not the end of the story. My builder is providing services in Spain and I cannot apply the reverse charge on his invoice(s) because I am not registered for VAT in Spain. The zero-registration threshold that applies under EU law to any supplies of goods or services made by a business that is not resident in that country means my builder will need to register for Spanish VAT – even if he charges me only one Euro – and charge me Spanish VAT.

As a final twist, a builder who is not VAT registered can exclude their work on overseas properties from the £85,000 registration test. See Builder services supplies abroad.

Anti-avoidance legislation prevents a business with all or mostly exempt income from claiming input tax on a property purchase by buying it in a separate legal entity.

A booming business in recent times has been children’s nurseries. These businesses will not be registered for VAT because their income is exempt from VAT. A common VAT question from nursery owners or their accountants – and other businesses with exempt income – is often along the following lines:

‘We are buying new premises for £300,000 plus VAT. Can we buy the property in a separate legal entity, register for VAT, opt to tax the property with HMRC and then claim input tax – charging a low future rent plus VAT to the trading business?’

This question is logical and the principle of buying a property in a separate entity is well-established and makes commercial sense; i.e. protecting the asset from any potential financial problems incurred by the trading business. However, anti-avoidance legislation means that any option to tax election is disapplied if the following conditions are relevant:

- The property purchase price exceeds £250,000 excluding VAT; i.e. it comes within the capital goods scheme.

- The property owner and tenant are connected parties – as defined by Corporation Tax Act 2010 s 1122 – and the tenant’s business has taxable income of 80% or less. In other words, the tenant is either not registered for VAT or partly exempt.

- The rent charged by the landlord to the connected party will still be exempt from VAT, meaning an input tax block – or inability to register for VAT – on the purchase of the property.

- The legislation prevents an exempt business from claiming input tax on a property purchase but only gradually repaying this VAT to HMRC with a small rental charge.

VAT Notice 742A s 13

Final tips

Here are three final snippets about builder services:

- If a builder provides services on a continuous basis, a tax point is created if either an invoice is raised or payment received, whichever happens first. A tax point is not created by issuing a document such as a fee note or application for payment.

- Most services provided by subcontractors to contractors will no longer be subject to VAT on the subcontractor’s invoices. The contractor will instead account for the reverse charge on their own returns. However, this outcome only applies if the contractor is selling on the services in question (VAT Notice 735).

- Builder services on a new charity building are zero-rated if the charity issues a certificate to the contractor(s) confirming the building will be wholly used for charitable purposes (VAT Notice 708 s 19). However, a charity can still issue a certificate if there will be non-charitable use of up to 5% in the building; e.g. a small café or gift shop.