VAT schemes for small businesses

Share this article

Neil Warren considers how the three main VAT schemes can reduce VAT bills and help the cash flow of a small business

Key Points

What is the issue?

The use of certain VAT schemes can produce cash flow benefits and, in some cases, a reduced VAT bill for some businesses. The article gives practical tips on each scheme, including pitfalls for certain transactions.

What does it mean to me?

The flat rate scheme is less popular following the introduction of the limited cost trader category on 1 April 2017. But there are still situations where favourable rates could produce a VAT saving compared to normal VAT accounting calculations.

What can I take away?

There are strict leaving thresholds with each scheme. The article considers how a business can account for VAT on closing debtors over a six-month transition period when it leaves the cash accounting scheme, and can also remain in the scheme in some cases if the threshold was exceeded because of one-off sales that will not be repeated.

The three main VAT schemes that are available to small and medium enterprises (SMEs) are:

- the flat rate scheme;

- the cash accounting scheme; and

- the annual accounting scheme.

The initial challenge is to establish which clients might be eligible to use the schemes. The joining thresholds for the annual and cash accounting schemes are the same; i.e. taxable sales in the next 12 months are expected to be less than £1.35m excluding VAT. The flat rate scheme threshold is much lower and expected taxable sales in the next 12 months must be less than £150,000 excluding VAT.

I am sometimes asked if there will be a problem with HMRC if a business gets its expectations wrong and exceeds the thresholds at the end of the first year. The answer is ‘no’ as long as the projections were based on sensible calculations. The threshold for all three schemes is based on ‘taxable’ sales; i.e. ignoring exempt and non-business income but including zero-rated sales.

Flat rate scheme: still relevant?

I often hear agitated football supporters claim that a certain player in their favourite team has ‘had his day’ and many advisers have felt the same about the flat rate scheme since 31 March 2017. The reason is because a new category for ‘limited cost traders’ was introduced on 1 April 2017, with a draconian rate of 16.5%. The new rate applies to any scheme user that purchases ‘relevant goods’ of less than £250 in a VAT quarter or where the figure is less than 2% of VAT inclusive sales for the period in question. And as a further complication, the rules about what is classed as ‘relevant goods’ are very complicated (see HMRC Notice 731, para 4.6).

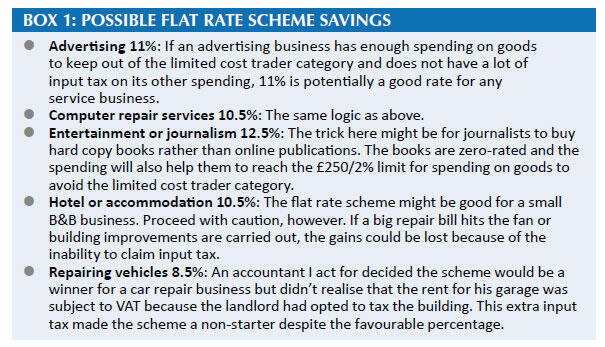

The main purpose of the flat rate scheme as far as HMRC is concerned is to save time with accounting issues. A scheme user only needs to record the gross value of its business takings and apply its relevant scheme percentage to this figure. However, the attraction for most business owners is the potential VAT savings that can often be enjoyed but are these still possible? See Box 1: Possible flat rate scheme savings. To complete the loop, see Box 2: Flat rate scheme tips.

Cash accounting scheme

The main advantage of the cash accounting scheme is that output tax is not declared on a VAT return until payment has been made by a customer, rather than the earlier sales invoice date that is usually relevant. This outcome also means that bad debt relief is automatic for scheme users because output tax is never declared on unpaid sales invoices. The downside, though, is that users cannot claim input tax until suppliers are paid.

The scheme might not be suitable for a business that has a lot of zero-rated or exempt sales where there is no output tax liability, especially if it pays suppliers very slowly. Some businesses have sales where the VAT liability can fluctuate (e.g. builders who do some zero-rated work on new houses but standard rated work on commercial properties) so the scheme’s cash flow benefits should be regularly checked.

Leaving tip

As with the flat rate scheme, the exit threshold is higher than the joining figure. A business needs to leave the scheme at the end of a VAT period if total taxable sales have exceeded £1.6m excluding VAT in the previous 12 months. This means either:

- output tax needs to be accounted for on debtors in the VAT period when the business leaves and input tax claimed on creditors; or

- VAT can instead be dealt with on these invoices in the following two quarters on a transitional basis; i.e. when customers pay and suppliers are paid. (See HMRC Notice 731 para 6.4.)

When the six month period has expired, there might be scope to claim bad debt relief on any sales invoices that are still unpaid (HMRC Notice 700/18 para 2.2); i.e. avoiding the need to declare output tax on the next return.

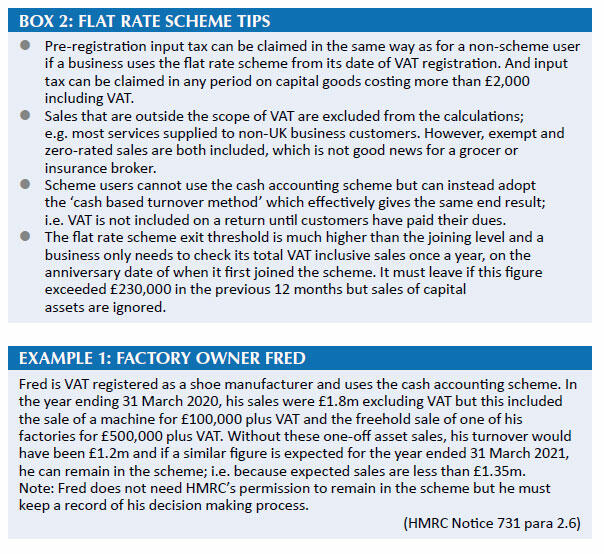

The sales figure for the exit threshold includes any stock disposals or capital assets but the good news is that a business can remain in the scheme if it expects that its total taxable sales in the following 12 months will be less than the joining threshold of £1.35m excluding VAT (see Example 1: Factory owner Fred).

Annual accounting scheme

It is easy to dismiss the benefits of the annual accounting scheme, which basically means that only one VAT return is submitted each year instead of four or 12. Many clients like to know their VAT liability on a quarterly basis and advisers encourage this as well because it gives reassurance that records are being kept up to date. But there are worthwhile benefits that might be relevant for some clients:

- Default surcharges: If a business has regularly incurred default surcharges, the annual VAT return means only one instead of four potential surcharges. The annual return is also due two months after the end of the annual period.

- Flat rate scheme users: A business can use the flat rate scheme and annual accounting schemes at the same time. A flat rate scheme user will therefore only need to carry out the ‘limited cost trader’ test on an annual basis.

- Annual accounts: It makes sense for the annual VAT accounting year to coincide with the financial year. This will make it easy to check, for example, that declared sales in Box 6 of the VAT return (the outputs box) are compatible with the declared sales on the annual accounts of the business in question.

Practical issues

A business that is registered for VAT as a group or part of a division cannot use the scheme. And once a business has left the scheme, it cannot rejoin for at least 12 months.

The other key issue is that scheme users must make monthly payments on account, which are based on the liability shown on the previous annual return. These payments can be made as nine monthly or three quarterly payments, and must be paid by direct debit, standing order or other electronic means. Each of the nine payments is equal to 10% of the previous year’s annual VAT liability. The balance owed is payable two months after the end of the accounting year. If the payments on account are too high, the overpayment will be

refunded by HMRC.

As a practical tip to help cash flow, if a business expects to pay less VAT in the current year compared to last year, which will be quite common in the current economic climate, it should write to HMRC to adjust the payments (HMRC Notice 732 para 4.7).