The widening net

Share this article

John Chaplin and Sam Moore provide guidance on the potential challenges faced by MNEs with international supply chains as a result of IR35 reform

Key Points

What is the issue?

HMRC have announced that the off-payroll working regime in the public sector will be extended to large and medium sized businesses in the private sector from April 2020. A consultation document has been issued on the detailed operation of the new law which includes certain modifications to the, already enacted, public sector rules. The questions raised in the consultation document, however, do not fully account for the greater diversity and complexity of the private sector and there are still some aspects of the 2017 public sector rules which would prove highly challenging if rolled out to the private sector. The way in which the public sector rules would apply to MNEs with international supply chains is one small but highly significant example of this.

What does this mean to me?

For many organisations, skill is more important than location in making resourcing decisions. This article looks at how the public sector off payroll working rules, if introduced to the private sector with only consequential amendments, would apply to MNEs with international supply chains. As part of this, we look at some examples of how corporate structure and the individual’s residence and work location can give what might at first glance appear to be unexpected results.

What can I take away?

To meet the requirements of the new law, large businesses are likely to need significant change programmes. The absence of draft law at this stage, however, means that they will need to work with a certain amount of ambiguity. Simultaneously businesses can engage with HMRC as part of the consultation process to ensure that the impact of issues more peculiar to the private sector are flagged and that the resultant legislation is more tailored to the private sector.

In the 2018 Budget, the Government announced that it intends to extend the public sector rules for off-payroll working to all medium and large sized businesses in the private sector with effect from 6 April 2020.

The off-payroll working rules have been considered in previous editions of Tax Adviser. However, in summary, the legislation:

- shifts the responsibility for determining whether a worker (engaged via an intermediary such as a Personal Service Company (PSC)) is a ‘disguised employee’ from the intermediary to the ‘client’; and

- shifts the responsibility for operating PAYE, NIC and Apprenticeship Levy on ‘disguised employees’ from the intermediary to a ‘fee payer’ (typically a UK agency or managed services provider (MSP) – though the definition is broader and can include the client itself).

The experience of the public sector has been that this (prima facie small) change had a substantial impact on the use of the contingent workforce (in terms of contractor turnover, day rate attrition, unfilled vacancies and growth of non-compliant structures) and it is likely that the impact on the private sector will be no less profound.

The Government is undertaking a consultation over the coming months on the detailed operation of the new rules which will inform the relevant clauses for the draft Finance Bill legislation (which is expected to be published in the Summer).

The consultation document has recently been published in which HMRC acknowledge that ‘the needs of private sector organisations differ to those in the public sector and that the range of activities undertaken are substantially wide ranging and therefore some changes are required’. However, whilst the consultation document does propose some changes to the 2017 public sector rules, it is our view that these proposed changes do not go far enough in recognising the greater complexity and diversity of the private sector.

Cross-border complexity

One small example of the complexity to address in the private sector is how IR35 reform impacts multinationals in connection with cross border supply chains.

In the public sector, this issue did not come particularly to the fore, reflecting the predominantly domestic nature of the supply chains.

However, in recent years, much of the private sector has moved away from this trend as the gig economy and agile working practices have grown hand in hand. These trends have been aided by improvements in technology facilitating remote working. As a result, for many large corporates, skills are now more important than location in determining how to resource a particular role or project with workers being drawn from across the globe.

For example, an IT contractor may work from his home in the UK for a client based in Germany. Another may be based in India, travelling occasionally to see his client in the UK.

This article looks into how the 2020 reforms would apply in these situations, assuming the public sector legislation at ITEPA 2003 Chapter 10 Part 2 is introduced to the private sector with only consequential amendments as well as taking into account any published guidance available at the date of writing.

Territorial scope of small companies exception

The Government had previously announced that small businesses in the private sector will not be subject to the changes and will continue to be subject to the existing ‘intermediaries’ regime in ITEPA 2003 Chapter 8 Part 2. For this purpose, the government has explained that they intend to use similar criteria as in Companies Act 2016 to define ‘small businesses’.

The consultation document elaborates on HMRC’s thinking, focussing particularly on the need for an expanded definition to cover non-corporate entities as well as pointing to a need for anti-avoidance provisions ’to ensure that parties connected to, associated with, or controlled by the client cannot take advantage of the provisions to exclude small private sector clients from having to consider the status of their off-payroll workers’.

Whilst the details of the small companies exception is likely to be expanded upon during the course of the consultation exercise, key questions for multi-national groups are likely to focus on the application of the small companies exception to non-UK entities and groups – including the application of the exception to UK branch operations and representative offices.

Residence, domicile and workplace of the worker

Where the rules do apply, it is worth noting that it is likely not all disguised employees will be brought into income tax in full.

In particular, the public sector rules contain provisions (under ITEPA 2003 s 61R(4)-(5)) which ensure that a worker is not subject to more tax than he would otherwise be liable to if he were an employee of the client having regard to his residence, domicile and work location.

A practical question arises in this instance as to the level of due diligence required of clients in relation to their workforce. The nature of the statutory residence test, in particular, requires an understanding of the worker’s personal factors which would not normally be known to any corporate client.

HMRC already recognises this challenge in relation to short term (employed) business travellers coming into the UK, allowing corporate data to be used as a proxy for an individual’s residence status, only requiring additional evidence as the individual’s physical presence in the UK increases (see HMRC’s EP Appendix 4 agreement).

Multinationals are likely to need to similar practical guidelines in relation to their contractor population, albeit with a reduced evidential requirement, recognising the looser relationship between client and worker than exists between employee and employer.

Residence of client and fee payer

Beyond worker residence issues, there is a question of the extent to which the assessment and withholding obligation falls on foreign operations.

The UK’s PAYE regime is subject to a territorial limitation (see for example Clark (H.M. Inspector of Taxes) v Oceanic Contractors Incorporated [1982] BTC 417) with the result that PAYE will only be in point if the employer is UK resident or is not UK resident but has a place of business in the UK.

This is broadly mirrored in the public sector off payroll working legislation. The obligation to determine whether the worker is a disguised employee sits with the client if it is resident or has a place of business in the UK. Likewise, the PAYE obligation falls on the last on-shore payer in the supply chain before the person controlled by the worker (e.g. the PSC) or failing that the client.

Whilst this appears to some extent logical and ensures consistency with the position of employees, the practical application of the rules may be more challenging.

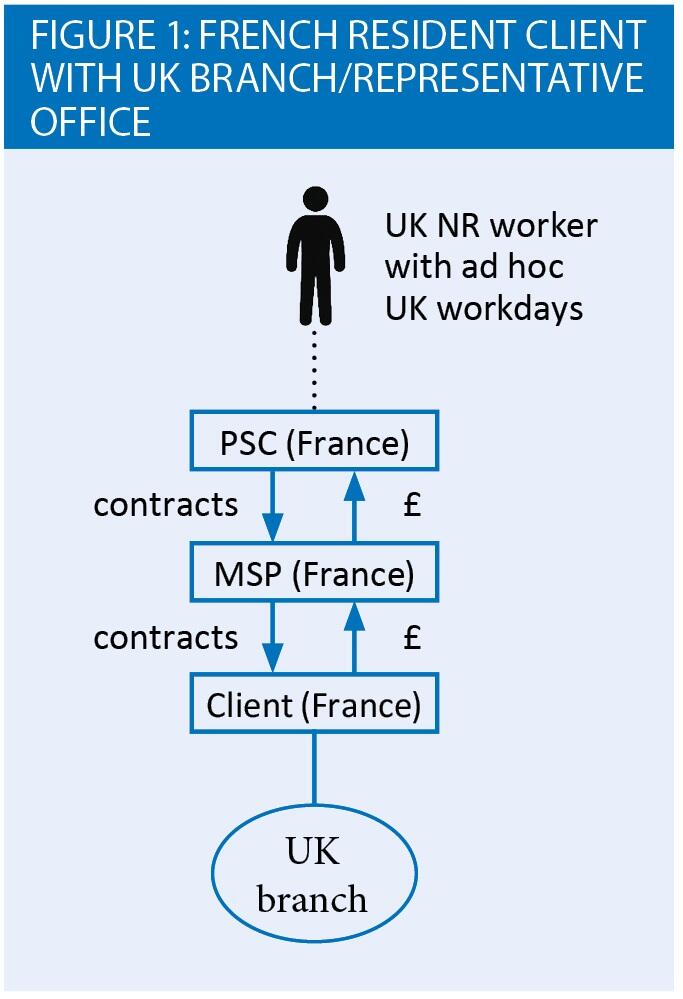

Figure 1 illustrates an extreme example of a French resident ‘client’ with a UK branch or representative office engaging with a French resident MSP, which then engages a French PSC, to provide a UK non-resident worker who works predominantly in France but undertakes occasional UK workdays.

In this example, the French resident client has a branch in the UK and the existence of this UK presence triggers an obligation on the French client to determine whether the worker is a disguised employee (and potentially operate PAYE), regardless of whether or not the work in the UK is undertaken for the benefit of the UK operation or whether UK staff are involved in the facilitation of the service.

It is clear in this example, that the UK branch needs to influence the French HQ’s processes and data flows; however, it may be difficult in practice for the branch operation to influence change over its larger HQ.

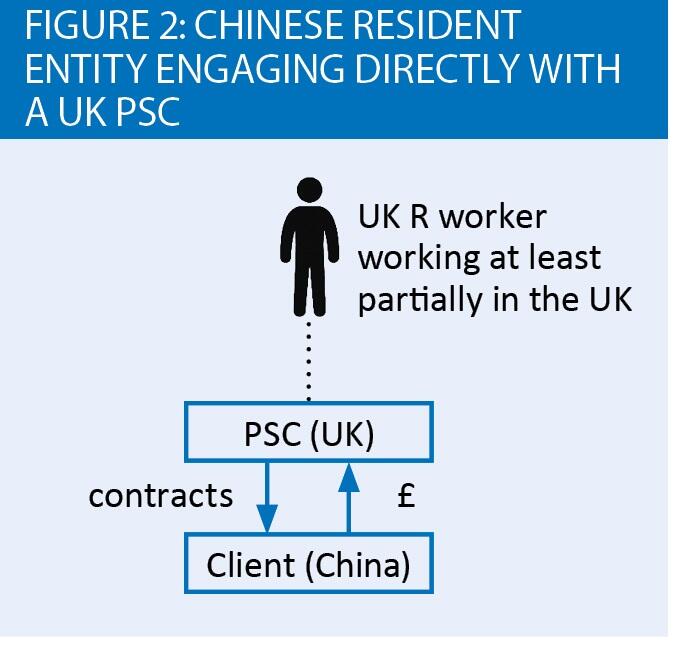

Somewhat unusually, the public sector rules also contain a ‘deemed residence’ provision at ITEPA 2003 s 61R(7). This provides that a client is treated as UK resident (even if it is not UK resident or has a place of business in the UK) if:

- it is also deemed to be the fee payer (i.e. there is no other UK payer before the person controlled by the worker);

- the individual is UK resident; and

- the individual at least spends some of his/her working time in the UK.

An example of this is set out in figure 2. This shows a Chinese resident entity engaging directly with a UK PSC for the provision of services of a UK worker who spends at least some of his time working in the UK.

In this example, the public sector rules would place the obligation to determine whether or not the individual is a disguised employee and apply PAYE on the Chinese entity.

In practice, this may be near impossible to enforce. In such a case, were the Chinese entity not to apply PAYE, it may be difficult for HMRC to assert that PAYE should be imposed on the individual under reg 72 or reg 141 Income Tax (PAYE) Regs 2003 given:

- PAYE recovery from the individual under reg 72 requires the high bar of employer taking ‘reasonable’ care with the failure to deduct PAYE being ‘due to an error made in good faith’ (Condition A) or the individual receiving relevant payments knowing that the employer ‘wilfully failed’ to deduct the correct amount of PAYE (Condition B);

- Reg 141 results in direct collection on the individual ‘in cases of casual employment’ and ‘any other case in which HMRC are of the opinion that deduction of tax by reference to the tax tables is likely to be impracticable’. Given the express deeming provisions in the primary taxing act for off payroll working, it is doubtful, that the overseas residence status of the client would be sufficient to meet this ‘impracticable’ bar and, even if this test were to be met, there is the more practical challenge that a special arrangement relies on notification from/agreement with HMRC.

As a result, the deemed residence provision could theoretically result in the paradoxical outcome of the individual being able to claim a deduction in his Self-Assessment tax return under reg 185(5)-(6) Income Tax (PAYE) Regs 2003 for the ‘tax treated as deducted’ – thus creating a loss to the Exchequer.

Double Tax Treaty (‘DTT’)

Thus far, we have focussed on UK domestic law provisions; however, given the breadth of the UK’s DTT network, it is worth considering whether these might limit the UK’s taxing ambitions.

A critical question is which Article under the DTT would cover the deemed income created under off-payroll working.

In the February 2019 issue of Tax Adviser, Keith Gordon looked at the Court of Appeal decision in the case of Fowler v HMRC. This addressed the question of how to approach a deeming provision in the country of source when determining the applicable Article in a DTT.

At the date of writing, no guidance has been released from HMRC setting out their views on the matter.

If the majority decision in Fowler were to be applied to off-payroll working, Art 15 (income from employment) of the OECD DTT would be in point. If this were combined with ITEPA 2003 s 61R this may then automatically deny treaty relief in some circumstances. For example:

- for UK resident fee-payers, treaty relief in Art 15(2) would not be in point (because the worker would be working for, or on behalf of, a UK resident employer);

- for UK branches of overseas residence fee-payers Art 15(2) may be in point provided that the remuneration is not borne by a UK PE (although the UK’s 59 day rule may be in point).

IR35 requires a further leap beyond ITTOIA 2005 s 15 (the deeming provision referred to in the Fowler case). ITTOIA 2005 s 15 simply treats income as being from another source (i.e. employment income becomes a trading receipt) whereas IR35 reform requires the client to construct a hypothetical employment relationship between the worker and the fee-payer and imagine that deemed income were paid from the latter to the former.

In such circumstances, it is not beyond doubt that contractors may find it difficult in practice to obtain double tax relief in the country of origin against the PSC’s corporation tax bill or dividend tax. Furthermore, resolution via the courts or through Mutual Agreement Procedure may be difficult to commercially justify. Faced with such a scenario, it is possible some contractors may choose to terminate their contracts and retreat from providing services to the UK as a practical means of protecting their bottom line.

Conclusion

It is clear that the public sector rules are in need of modification in order to ensure that they are workable for the private sector. The impact on cross border supply chains is just one such example.

It is hoped that with effective engagement, HMRC might be encouraged to minimise the extraterritorial impact of the legislation when it is introduced to the private sector, allowing businesses to focus on UK resident contractors (being the likely preponderant risk to the Exchequer).

At the very least, clear guidance should be provided by HMRC as swiftly as possible on the direction of travel of the new law, the burden of proof/due diligence required in respect of their contractor base covering information not typically held by the client and clarity over the interaction with DTTs.

For multinationals, the temptation having read this, may be to wait until the publication of the draft legislation and hope this ultimately provides clarity. However, one of the key learnings of the reform in the public sector was that waiting for the draft law to be tabled resulted in rushed implementation and challenges with the contractor base.

Instead, with approximately one year to go until implementation we would advocate a triple track approach in which:

- detailed planning is accelerated in the ‘known’/’likely’ outcomes of the reform;

- information is gathered and tentative planning undertaken over the more extreme aspects of the law not yet faced in the public sector; and

- businesses fully engage with HMRC to ensure that the new law is suitably adapted to the needs and challenges of the private sector.

Finally, it is worth noting that whilst this article has deliberately focused on how the new off-payroll working rules will apply to cross border working scenarios, there are existing legislative provisions that should be considered in determining a business’ liability to PAYE in relation to its international supply chain. A key example of this is the application of the host employer rules at ITEPA 2003 s 689 to foreign agencies or other overseas businesses involved in resource augmentation or the supply of labour. In the interests of brevity we have not considered these provisions; however, in practice multinationals should take an all-round view in assessing their risks.