The winds of change

Share this article

Carmen Aquerreta and Sarah Lord consider how the UK’s popular tax regime for intangibles will need to be recast

Key Points

What is the issue?

Action 5 of the OECD/G20’s Base Erosion and Profit Shifting (BEPS) project requires that the UK’s patent box regime must be changed. The new regime will measure substance by reference to R&D activity. This is predicated on a link between past R&D expenditure and future income benefiting from the regime

What does it mean to me?

All businesses wishing to benefit from the current patent box regime should act now to secure access to the grandfathering period. Even when grandfathered it will be necessary to start tracking R&D expenditure from 2016 to ease the eventual transition into the new regime

What can I take away?

Action is needed before 30 June 2016 to ensure that benefit under the current regime is secured over the grandfathering period. It is essential to consider applying the nexus principles to specific circumstances

The OECD’s Forum for Harmful Tax Practices (FHTP) published its action 5 final report on 5 October 2015, as one of the 15 BEPS actions. Action 5 states that taxpayers should only benefit from any preferential tax regime if they can show their engagement in the substantial activities that give rise to the income or profit falling into the beneficial regime. The action 5 final report sets out the guidelines for the agreed approach for several preferential regimes – the ‘nexus approach’ – although only intangibles regimes are considered in detail.

The nexus approach

In the context of intangibles regimes, such as the UK patent box, action 5 determines that R&D activities give rise to income from patents (and similar forms of intellectual property). This link, or ‘nexus’, demonstrates the substantial activities that give rise to the income.

The nexus approach will be delivered by way of a ‘nexus fraction’ that will be applied to income in determining what proportion is eligible for preferential tax treatment.

| Qualifying R&D spend to create IP assets + 30% uplift | X Income received from IP |

| Overal expenditure on creating the IP assets |

Qualifying R&D spend:

- direct expenditure on own R&D activity; and

- expenditure on R&D activity subcontracted to third parties.

Overall expenditure:

- direct expenditure on own R&D activity;

- expenditure on R&D activity subcontracted to third parties;

- expenditure on the acquisition of IP; and

- expenditure on R&D activity subcontracted to related parties.

This nexus fraction must be determined and applied to income for each IP asset. The fraction will be cumulative. The 30% uplift will be capped at actual spend, so the nexus fraction cannot exceed a value of 1. This is not a jurisdictional test and the amounts included in the fraction are those incurred at a company level. So for groups that split R&D versus IP ownership and commercialisation activities across UK legal entities the change to nexus could have a significant impact.

The definition of IP asset for these purposes has been widened since the OECD’s action 5 interim report was published in September 2014. The action 5 final report recognises that, in many cases, it would be difficult for a business to track R&D expenditure to a level as granular as individual patents, and similarly difficult to trace this expenditure across to income. The action 5 final report therefore allows businesses to track and trace to product or product category instead, but stipulates that businesses must use the most granular level available. This means that claimants will have multiple nexus fractions – one for each patent, product or product family (depending on the level at which the claimant can track and trace).

The action 5 paper also sets out some specifics on timings:

- All current regimes that are not aligned with the nexus principles must close to new entrants by 30 June 2016 at the latest. New entrants are defined as both new taxpayers and new IP assets. Patents applied for but not granted before 1 July 2016 will be existing assets.

- Grandfathering provisions can be available until 30 June 2021 at the latest.

- IP assets transferred from related parties after 1 January 2016 must be excluded from any grandfathered regimes unless they qualify for benefits under a preferential intangibles regime in the source jurisdiction. IP assets in this category will be eligible for the current regime until 31 December 2016, in effect allowing for a six- to 12-month grace period.

Implementation of the nexus approach to the UK patent box regime

The UK consultation was published on 22 October 2015 and closed for comment on 4 December 2015. At the time of writing, draft legislation was expected to be released on 9 December 2015 with Finance Bill 2016. Work is continuing to finalise the UK legislation, with the expectation that this must be enacted as part of FA 2016 for implementation on 1 July 2016.

The BEPS action 5 final report is intended to form guidelines for member states to implement in domestic legislation as a minimum standard (rather than best practice). However, domestic legislation will be reviewed by the FHTP to ensure that it is in line with the principles set out in the paper.

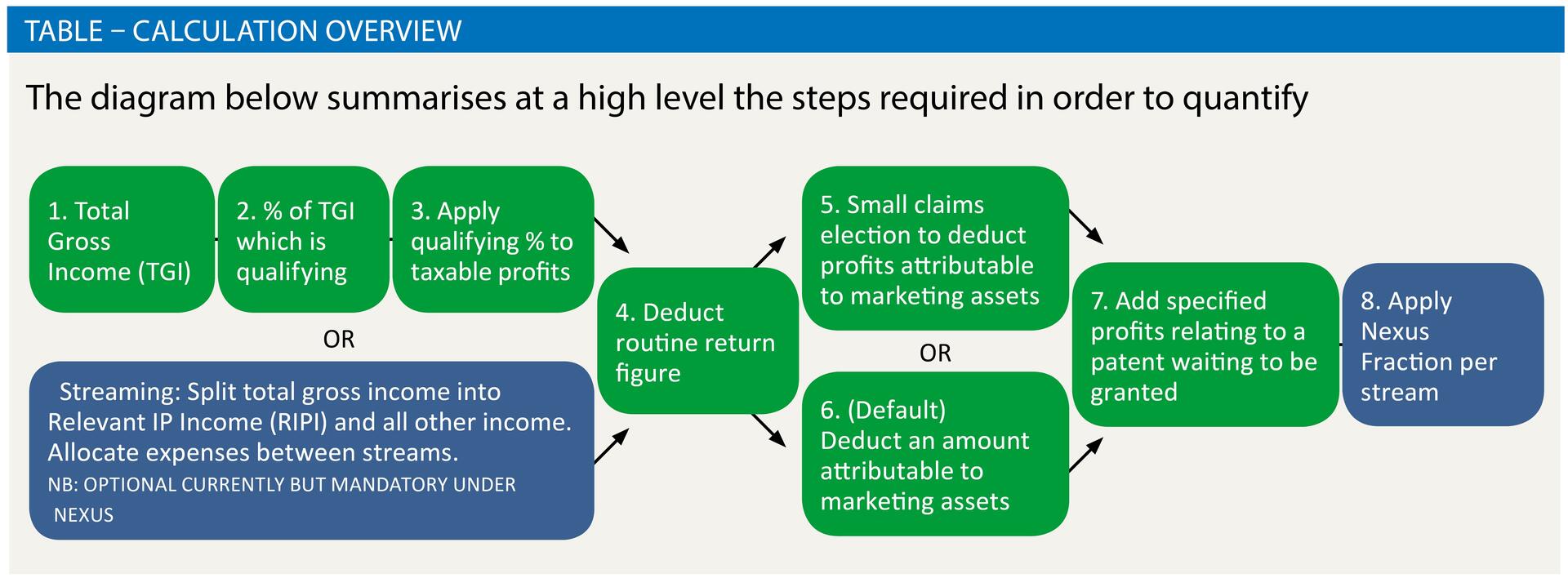

At the time of writing, the authors understand that the UK intends to retain as much as possible of the current patent box regime architecture, while modifying it to ensure it is consistent with the nexus principles. The approach, as set out in the Table, has been discussed and agreed in concept with the FHTP.

The UK regime will, therefore, retain the qualification requirements as per the current patent box regime. To qualify for the regime, a claimant entity must hold a patent granted by the UK Intellectual Property Office, the EU Intellectual Property Office, or the intellectual property office of one of 13 other EEA member states (Austria, Bulgaria, Czech Republic, Denmark, Estonia, Finland, Germany, Hungary, Poland, Portugal, Romania, Slovakia and Sweden). Pending patents will still accrue benefit in the application period that can then be claimed on grant. The development and active ownership conditions will also be retained.

The UK regime will also continue to compute the quantum of profits qualifying for benefits (referred to as ‘relevant IP profits’ or RIPP in the legislation) in the same way.

A claimant entity will still be required to determine its relevant IP income (that being revenue mapped to patents. Under the current regime a claimant entity has a choice of either the formulaic apportionment methodology (the default approach), or streaming (under a separate election). Streaming requires the claimant entity to allocate tax-deductible expenditure to either qualifying or non-qualifying income. This gives effect to determining the specific profits that are attributable to the patents.

The nexus-compliant regime will mandate that the streaming approach be used. This is to ensure that the nexus fractions are applied to patented profit at the most granular level possible (‘income’ in the fraction really refers to ‘profits’). It is expected that this will increase the compliance burden of the patent box regime for those businesses that have not currently elected to stream. Interestingly, businesses that have already elected to stream tend to be large enterprises where more detailed management information is available, and where the benefit of doing so outweighs the administrative burden.

Once patent box profit has been determined by reference to each stream, the mechanisms for removing the profit attributable to routine activities (routine return) and brand value (marketing asset return figure) will remain the same.

At this stage, a business operating under the nexus-compliant regime may have a number of patent box profit ‘streams’ that it has calculated in accordance with the above methodology. The nexus fraction relevant to each individual stream will then be applied to the respective patent box profit that has been calculated. This will then determine the proportion of streamed patent box profit eligible for benefit.

It is clear that the compliance burden for most businesses will be increased under the nexus-compliant patent box regime. Whether or not a business has already elected to stream, few will already have data available to compute streams of patent box profit at such a level of granularity.

Tracking and tracing

A key element of any nexus-compliant regime will be in ensuring there is a robust framework to allow businesses to track R&D expenditure and trace this to IP income in order to determine their nexus fractions.

Businesses will have the option to track and trace R&D expenditure and income to an IP asset, product, or product family. However, the action 5 final report makes it clear that the expectation is that businesses will only track and trace to product or product family when tracking to an IP asset is not feasible, or where this would require arbitrary splits of either expenditure or income.

The UK legislation will not define product or product family in detail. The intention is to allow businesses to determine a mechanism for tracking and tracing that is practical and achievable, and that can be supported and documented to HMRC’s satisfaction. The action 5 final report sets out an example of product family, where a company produces printers for three different uses – office use, small personal printers, and photo printers. Different printer models containing the same IP within each of these categories would form part of the three wider product families for tracking and tracing purposes.

The expenditure that must be tracked for the nexus fraction is expenditure of the claimant entity, including any permanent establishments regardless of location.

To determine each of the relevant elements of the tracked nexus fraction, the UK legislation will set out definitions of each. Direct or subcontracted expenditure for the nexus fraction must be expenditure on R&D that meets the definition at CTA 2010 s 1138, and the guidelines issued by the Department for Business, Innovation & Skills.

The starting point for most businesses will be expenditure claimed for R&D tax relief purposes, albeit there is no requirement to make such a claim for it to qualify for the nexus fraction. In any case the qualifying costs for R&D are not a perfect match for the nexus fraction.

Direct expenditure on own R&D activity will be staffing costs, software or consumable items, externally provided workers (EPWs) or payments to subjects of a clinical trial. Expenditure on related party subcontracting (that is, included in the denominator) will be defined to follow the rules set out for subcontracting in the current UK R&D scheme for SMEs. The figure used will therefore be the lesser of the amount paid and that spent on R&D by the subcontractor. Expenditure on third-party subcontracting (that is included in both the numerator and the denominator) will also be defined following the rules set out for subcontracting in the current UK SME R&D scheme, so the amount used for the nexus fraction will be 65% of that paid.

The denominator will include acquisition costs of qualifying IP assets. This will comprise any amounts paid to purchase an IP asset outright or to purchase a right to use IP, so licence fee payments for qualifying IP rights will also sit on the denominator. If a bundle of IP is purchased, a claimant company would be able to bring into the denominator only the value of IP whose associated income could eventually be in the patent box regime. The acquisition cost element of the nexus fraction is the only element that looks at value, as compared with cost. The 30% uplift is intended to alleviate some of the distortive impact of any acquisition expenditure for this reason.

The nexus fraction is cumulative, and businesses will need to start tracking and tracing on this basis from 1 July 2016, even those businesses that are grandfathered. This will then mean that, when a patent box claimant comes out of the grandfathering provisions, a suitable bank of tracked, cumulative data will be available for computing the fraction.

For a business going directly into the nexus-compliant regime, there will be transitional provisions in place. Such a business will be required to look back three years from 30 June 2016 (that is, to 1 July 2013) at overall company expenditure in the relevant nexus fraction categories as a proxy for tracked spend. This will function as a rolling fraction, with each year of tracked data identified from 1 July 2016 replacing the oldest year of historic company expenditure. Should businesses wish to look back more than three years, this will be acceptable as long as suitable justification can be given.

Rebuttable presumption

The nexus fraction is intended to be a rebuttable presumption, and a business will be able to challenge its outcome in some circumstances, allowing the fraction to be recast so that an appropriate level of income benefits from the regime. However, to invoke the rebuttable presumption, certain conditions must be met:

- the claimant entity must first calculate the nexus fraction (excluding the 30% uplift), and this must equal or exceed 25% before the rebuttable presumption can be invoked;

- the claimant entity must demonstrate and evidence that, due to exceptional circumstances, the result of the nexus fraction is not appropriate; and

- the application of the rebuttable presumption must be reviewed annually.

- The action 5 final report sets out that it is not expected that the rebuttable presumption will be used by a claimant entity regularly. Tax authorities will be required to report all use of the rebuttable presumption to the FHTP.

Actions before 30 June 2016

While the two-year time limit for electing into patent box continues to apply, new claimants must demonstrate they meet the qualifying company requirements by 30 June 2016. Therefore, businesses that have yet to consider the application of the patent box to their circumstances should undertake this exercise before 30 June 2016. It is likely that, for many businesses, the application of the nexus principles to the patent box regime will reduce their benefit compared with the current regime. In addition, the principles will increase the compliance burden of the patent box for businesses that will inevitably be a factor in considering whether to make an election into the regime.

Regardless of whether grandfathering provisions are available, businesses will need to implement a tracking and tracing methodology from 1 July 2016 to ensure that they have the data to support their nexus fractions. Thought should be given to current management information systems, patent box documentation and R&D arrangements.

If any uncertainties arise on implementation, businesses should engage with HMRC now to ensure their views are heard.