Work or pleasure?

Share this article

Andrew Evans explores the differences between SDLT and the new Welsh LTT when determining whether grounds and gardens are for residential or commercial use

Key Points

What is the issue?

The stamp duty land tax (SDLT) and the new Welsh land transaction tax (LTT) regimes apply substantially different rates of stamp duty on residential and commercial property.

What can I take away?

There was a lack of guidance on gardens and grounds until March 2019, and there are now differences in emphasis between the guidance from HMRC and the Welsh Revenue Authority.

What does it mean to me?

Purchaser and advisers dealing with the transaction must ensure that the stamp duty return is filed correctly and the right amount of tax is paid.

The stamp duty land tax (SDLT) and the new Welsh land transaction tax (LTT) regimes apply different rates of stamp duty on residential and commercial property. Properties that have a mixture of residential and commercial use, for example a shop with flats above, are treated as mixed use transactions and qualify for the commercial rates of stamp duty. Difficulty applying the correct rates can arise when dealing with the acquisition of country estates, comprising a large house and varying amounts of land.

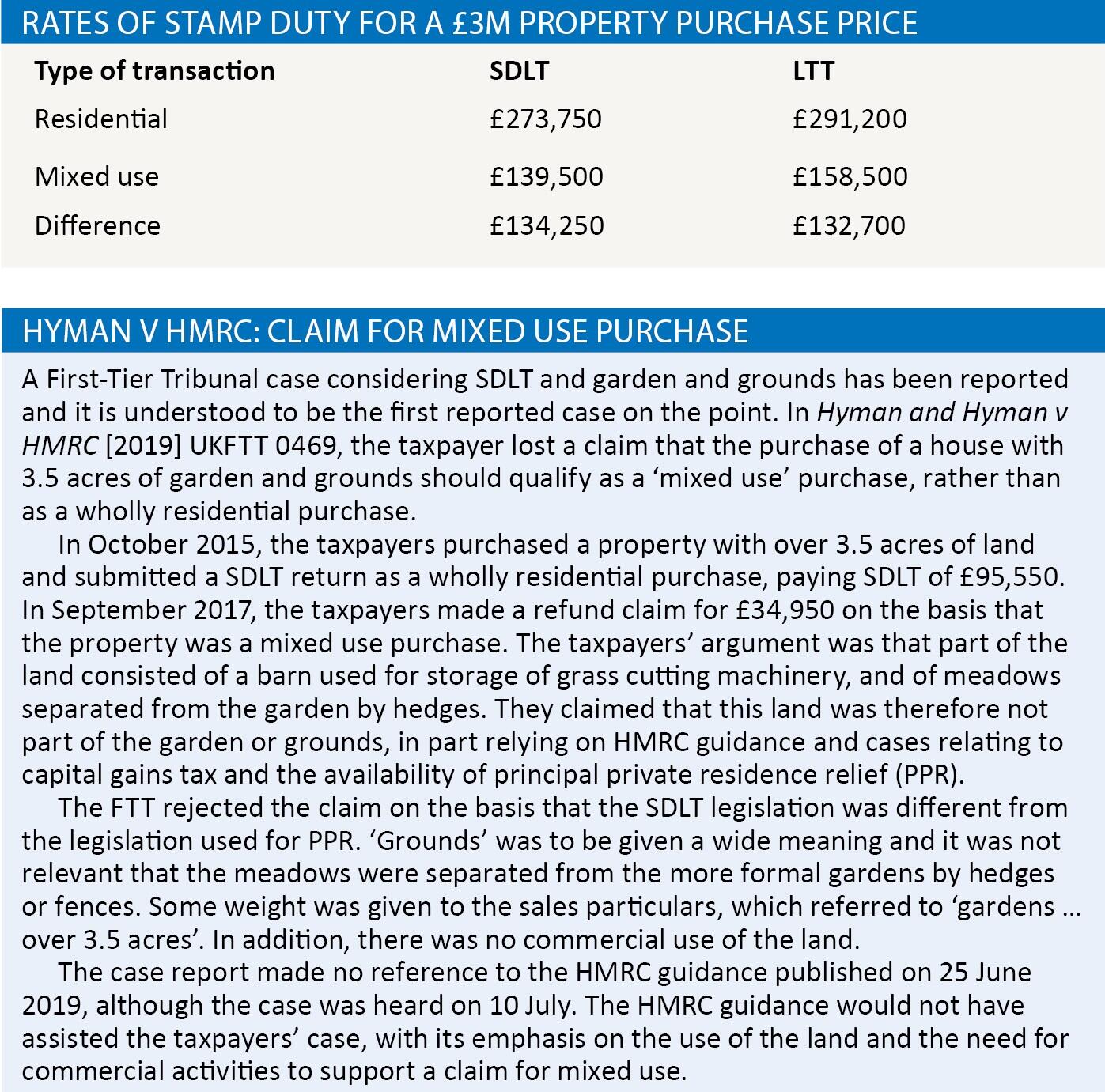

The differences in the amounts of stamp duty can be substantial, as shown in the table below (assuming a purchase price of £3m). It is very important for the purchaser and the advisers dealing with the transaction to ensure that the stamp duty return is filed correctly and the right amount of tax is paid.

Before March 2019, advisers had very little guidance on garden and grounds from HMRC in relation to SDLT and from the Welsh Revenue Authority (WRA) in relation to LTT. The WRA led the way with their new guidance being published on 30 April 2019, followed by HMRC’s new guidance being issued on 25 June 2019.

Definition of residential property

The definitions of residential property for SDLT and LTT are virtually identical and are contained in Finance Act 2003 s 116(1) for SDLT and Land Transaction Tax and Anti Avoidance of Devolved Taxes (Wales) Act 2017 s 72(1) for LTT:

‘In this Act, “residential property” means:

a) a building that is used or suitable for use as one or more dwellings, or is in the process of being constructed or adapted for such use; and

b) land that is or forms part of the garden or grounds of a building within paragraph (a) including any building or structure on such land; or

c) an interest in or right over land that subsists for the benefit of the building within paragraph (a) or of land within paragraph (b); and

d) “non-residential property” means any property that is not residential property.’

The only differences between SDLT and LTT are the inclusion of the ‘and’ and ‘or’ in the highlighted text in the case of SDLT; and the fact that the wording about non-residential property is included in a sub-section in the case of LTT.

The important question for practitioners advising on the acquisition of county estates is: when does a house cease to be a house with garden and grounds and subject to residential rates of stamp duty, and become a house with non-residential land which means a stamp tax return for mixed use can be made? Although the definitions of ‘residential property’ are very similar for both SDLT and LTT, there are a number of differences between the guidance on ‘garden and grounds’ published by HMRC and WRA.

HMRC guidance

HMRC Guidance on garden and grounds starts at SDLTM00365. The starting point is the status of the building. If there is no building which is used or suitable for use as a dwelling, or in the process of being constructed or adapted for such use, then any associated land would not be residential property. The next key point is that the actual use of the garden and grounds at the effective date of the transaction is critical. Proposed future use by the purchaser is irrelevant. Historic use of the land can be relevant when considering the status of the land at the effective date of the transaction. HMRC look for customary, continued or regular use of the land, rather than any use that appears to be part of a contrived arrangement.

HMRC consider a range of factors when considering whether land forms part of the garden or grounds of a building. They stress that no single factor is likely to be determinative by itself, although not all factors are given equal weight. The most significant indicator is the use of the land. In particular, where the land is used for commercial rather than domestic purposes, the commercial use would be a strong indicator that the land is not the ‘garden or grounds’ of the relevant building. HMRC would expect to see evidence of commercial use. Difficulties can arise where activities could be undertaken both for leisure and on a commercial basis, such as bee keeping, grazing or equestrian activities.

Other factors considered by HMRC include:

- Layout of land and buildings: Stables and paddocks used by the family for their own horses or livestock will indicate garden and grounds, while stables used for a commercial livery service would be an indicator of land not being garden or grounds.

- Proximity to the main dwelling: Land close to the house is more likely to be treated as garden or grounds, rather than land that is separated by a road or river, or other land in third party ownership.

- Extent of the land: The extent of the land would be relevant in relation to the building. A large country house may be expected to have sizeable gardens. However, large areas of fell and moorland are unlikely to be residential in nature.

- Legal factors and constraints: Restrictive covenants over the use of the land, such as prohibitions on commercial use, indicate gardens and grounds.

HMRC make it clear that receipt of the Basic Payment Scheme (the replacement for single farm payments) would be an indicator of commercial use but would not mean by itself that the land is necessarily non-residential in nature. HMRC will closely scrutinise arrangements which appear to have been put in place for the purposes of changing the SDLT residential/non-residential status of the land.

WRA approach

The WRA take a similar approach to that of HMRC by examining whether there is a dwelling on the land in the first place. The WRA guidance is found within LTTA/1050. The WRA also adopt the question of fact approach and looking at the use of the land at the time of completion of the purchase.

The WRA place a lot more emphasis on the question of whether the land is being used to conduct a business or trade and therefore classed as non-residential. The WRA guidance sets out a number of indicative factors but stresses that none of the factors are definitive tests. The factors include:

Has the activity been undertaken earnestly in the pursuit of business interests as opposed to being undertaken for pleasure, enjoyment or convenience? An example is given of a working sheep farm as opposed to a dwelling with a small number of fields which are let on a grazing licence to a farmer for the purposes of not having to mow the grass.

- Has the activity has been undertaken on sound and recognised business principles, including being registered for VAT and having contracts in place for the supply of goods and services?

- Has the activity a reasonable prospect of profit and the intention of generating a reasonable income relative to the land? An example is given of keeping a flock of chickens to sell the eggs where the enterprise is loss making. This would not be treated as a business undertaking and makes the land residential in nature.

- Has the activity been undertaken with reasonable continuity? An example is given of contract farming (business) as opposed to renting out a field for a couple of weeks a year coinciding with a festival or event (non-business).

- How is the land is viewed by other public authorities; for example, exemption from council tax or non-domestic rates or receipt of the Basic Payment Scheme?

- Has a local authority granted planning permission or other licences which are indicative of a business use of the land; for example, planning permission for a shower block linked to a camp site?

The following examples are based on real life questions which have recently come across the author’s desk.

Ambridge Hall

A six bedroom house in Berkshire with eight hectares of land is being sold for £3.5m. The land comprises seven hectares of paddocks with a stable block comprising of stabling for five horses, substantial formal gardens and associated outbuildings (garage and storage buildings). Basic Payment Scheme payments are claimed on the land, although the paddocks are used for the owner’s horses. Friends of the family may use the paddocks to graze their horses.

Brookfield Farm

A nine bedroom house in Worcestershire sold for £3.5m, with 70 hectares of land of which over 60 are operated on a contract farming basis with a mixture of arable and livestock, a fishing lake stocked with carp which produces an annual income of £40,000, two cottages located at least half a mile from the main house rented out on an assured shorthold basis, converted barns rented out for commercial storage, substantial formal gardens, garaging and other outbuildings.

In the author’s view, Ambridge Hall is likely to be considered solely residential in nature. There is no commercial activity in relation to the land. The description of the fields as ‘paddocks’ and the relatively small size area are indicators of the land being ‘garden and grounds’ and existing solely for the benefit of the house. Brookfield Farm would qualify for mixed use for stamp duty purposes. There are substantial commercial operations comprising the contract farming, carp fishery, assured shorthold tenancies of the two cottages and a commercial storage operation in the converted barns.

Conclusion

The publication of guidance by both HMRC and the WRA will assist practitioners in advising their clients on the stamp duty payable on substantial country houses and associated land. Although the legislation definitions for SDLT and LTT are virtually identical, there is a slight difference in emphasis between HMRC and the WRA in the guidance, with the WRA placing greater emphasis on the commercial use and activities associated with the land in order to justify a claim for mixed use for LTT.