Putting UK taxation in a global context

Share this article

Chris Sanger considers the tax responses of governments around the world to Covid-19 in their battle to alleviate the financial and economic turmoil

Key Points

What is the issue?

With a need in to deliver immediate liquidity, solvency and income support for the economy in response to Covid-19, tax measures which can deliver support rapidly are now even more important than they were a decade ago.

What does it mean for me?

The initial support phase has focused on successful administration and the adaptation of operational policy to fit the needs of governments. The majority of relief measures have been administrative, including filing postponements, penalty and interest waivers and tax payment deferrals.

What can I take away?

For now, in the UK we are clearly seeing the beginning of the shift from support to stimulus. This is likely to see a significant reduction in the intensity of aid, and a reoccurrence of some of the stimulus packages of old.

Governments around the world are acting decisively to protect their people and economies from the disruption being caused by the Covid-19 pandemic. Whether through tax cuts, incentives or administration changes, tax systems will play a significant part in helping to alleviate the financial and economic turmoil.

The level of fiscal intervention we have seen in recent months has been unprecedented in modern history: more akin to fiscal subrogation than fiscal stimulus, with governments stepping into the shoes of other actors in the economy. The last time the world faced a global recession, in the global financial crisis of 2008 and 2009, tax measures represented the biggest share of fiscal stimulus measures. Among OECD countries, 56% of total fiscal stimulus packages in the wake of the 2008-2009 financial crisis can be attributed to tax measures (see OECD Economic Outlook, Interim Report March 2009).

With a need in the last couple of months to deliver immediate liquidity, solvency and income support for the economy, tax measures which can deliver support rapidly have been even more important than they were a decade ago. They are also being adapted to a far greater scale; the International Monetary Fund data indicate that total global support issued so far represents some 20% of global GDP – more than ten times as much as during the 2008-2009 financial crisis, when the figure was 2% (see Policy Action for a Healthy Global Economy and Policy Responses to Covid-19).

The details of the UK's fiscal response to the crisis to date have been covered previously in detail in Tax Adviser. Instead, this article compares the UK's response to that of other countries, particularly in the G7, and considers the changes that may be yet to come.

A plethora of changes

At the start of June 2020, EY's 130+ jurisdiction Global Stimulus Response Tracker, a tool made publicly available on ey.com, identified well over 2,700 tax-focused support measures in place across the jurisdictions covered, and that number continues to grow rapidly. It is estimated that fiscal support in response to the Covid-19 crisis has reached more than $15 trillion across the 15 largest economies alone (see COVID-19: How are governments responding to the call for stimulus?), and such support had been unveiled by governments from Albania to Zambia.

The tracker, alongside eight other trackers on ey.com, provides a wealth of information that allows comparison and the opportunity to query the data. So, what can we discern from the data about the patterns of responses? What are the most favoured tax measures? What is the relative importance of tax administration measures in providing support? And how does the UK's response compare to global trends?

An international framework: support, stimulus, revenue

To answer these questions, it is helpful to consider the phases of the response to the economic crisis. The OECD report 'Tax and fiscal policy in response to the coronavirus crisis' (see Tax and Fiscal Policy in Response to the Coronavirus Crisis: Strengthening Confidence and Resilience), identifies four phases; the first two relate to 'support' and are followed by stimulus and then 'revenue [raising]'. The OECD recognises that these phases may overlap. So against this framework, where are these countries today?

Support phase

The answer is very clear: we are still strongly in the support phase. During this initial support phase, the story has not been about high tax policy but about successful administration and the adaptation of operational policy (i.e. administration) to fit the needs of governments. At a global level, the Tracker shows activity across all countries, whether in corporate tax, personal tax, VAT or other indirect taxes.

The majority of relief measures have been administrative in nature. Indeed, the most numerous measures include: filing postponements (19%); penalty and interest waivers (16%); and tax payment deferrals (22%) (see chart 1). This is expected, as tax administration changes are relatively straightforward to implement, and they provide immediate cashflow relief, whilst leaving few concerns about the long-term fiscal impact. Tax obligations are deferred but not eliminated.

Even so, we are seeing a number of tax policy measures being introduced. Primarily, these seem to be about delivering upfront cash-tax benefits to taxpayers as quickly as possible. Tax rate cuts (across the tax types) have been delivered in the form of 161 incentives across 75 countries, though it should be noted that many of these cuts are targeted in specific areas, rather than necessarily being cuts to the rates of the largest taxes. Some 47 jurisdictions have implemented 'cash incentives', albeit the mechanism by which they do this varies: some through corporate income tax measures, some through VAT/GST measures, and some through personal income tax/payroll measures.

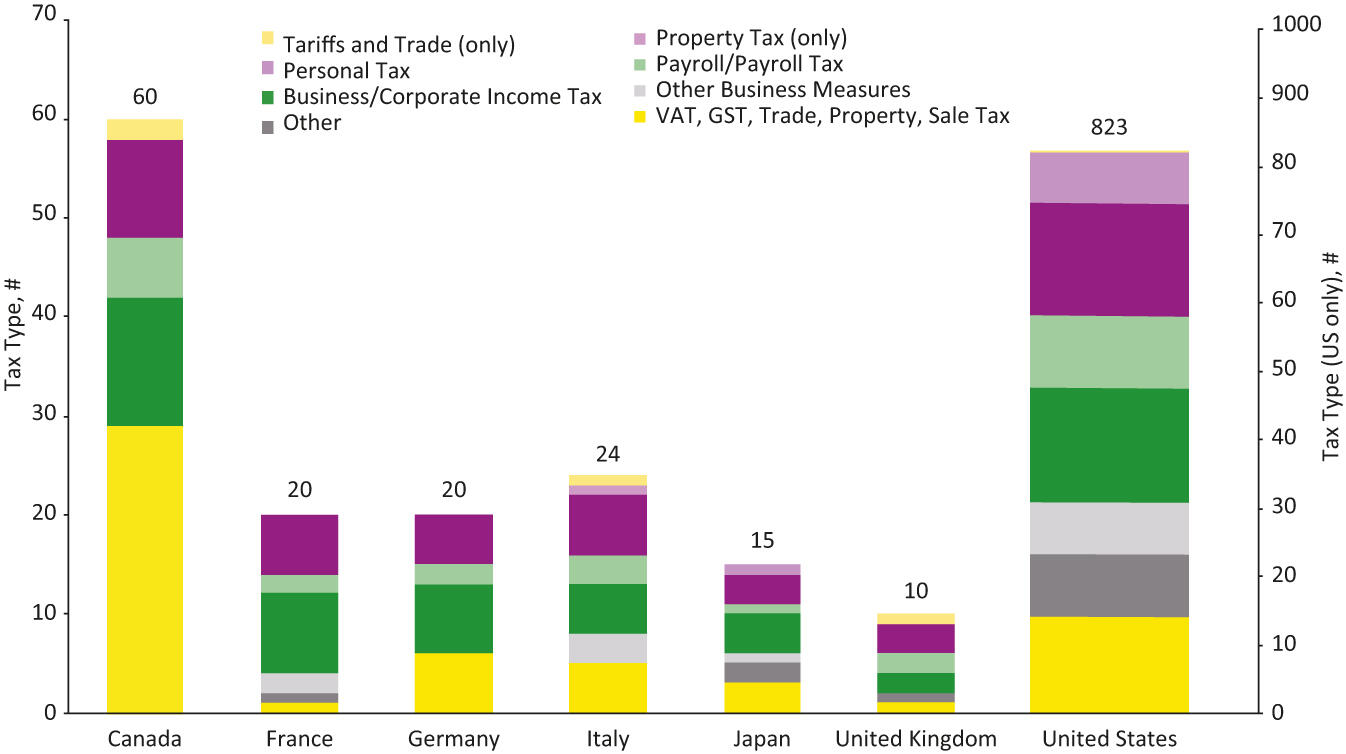

The type of tax measures introduced in the UK during the support stage has been consistent with this pattern (with deferral of taxes comprising half the measures). However, charts 2 and 3 show that the UK has introduced far fewer measures to date compared to other G7 countries. Of course, quantity is not the same as quality, nor is it a measure of fiscal impact. Federated countries like the US will clearly show many more measures as some reliefs will be introduced at the state level. Nevertheless, chart 4 shows that, consistent with US but in contrast to France and Germany, the largest part of the UK's immediate response has come through monetary rather than fiscal stimulus.

Stimulus phase

The tracker also indicates which governments have started to venture into the stimulus phase. EY research identified that fiscal stimulus following the 2008-2009 financial crisis included six key areas:

- accelerated depreciation;

- loss carryback/forward;

- corporate income tax rate reductions;

- research and development credit enhancements;

- indirect tax activity; and

- personal income tax measures.

The first of these, accelerated depreciation, has been adopted by 15 countries already, including Australia, China, New Zealand and the US. Of course, the stimulus measures of the crisis past may not be the right measures for crisis present and crisis future. However, they can be a good place to start.

Germany has announced a three percentage point cut in VAT rate from 1 July 2020, again replicating a stimulus measure of choice for the previous financial crisis, and in contrast with the VAT rise in Saudi Arabia, which is facing the twin challenges of Covid-19 and the slump in oil prices.

A third area is that of corporate loss relief. Historically this has been seen as well targeted, since it provides cash injections into businesses that, by definition, have a history of profits and paying tax. Even in the support phase, Germany introduced a specific measure for small businesses, which can claim a refund for tax amounts already paid if they are expecting a loss in 2020. In the US, under the CARES Act, a loss from 2018, 2019 or 2020 can be carried back five years. Loss-relief measures would seem like a valuable precedent from the last crisis that could be of benefit again.

Revenue phase

What is clear is that, wherever we get to with the stimulus measures, the scale of fiscal impact will be staggering. Returning to the UK, public sector net borrowing in April totalled £62.1 billion, up £51.1 billion on last year, and the largest in any single month. The Office for Budget Responsibility estimates public borrowing of almost £300 billion this year. At 15% of GDP, it will be the biggest deficit since the Second World War, and lead to public sector net debt surpassing 100% of GDP for a period of the 2020/21 fiscal year (see https://obr.uk/coronavirus-analysis). As we move to revenue phase of cycle, there will be calls to utilise all this change as a chance to recraft our tax system. It may be easier to change our tax system today amidst all this disruption than it has been for decades.

A key question, however, will be: when is the best time to enter the revenue stage? The OECD's advice is that: 'The best way to boost tax revenue will be to support solid growth, including through sufficiently strong and sustained stimulus.' It also notes that 'efforts to restore public finances should not come too early'. What exactly constitutes 'early' will depend on the factors in each country. The ability to borrow at near nil or even negative interest rates may mean that some governments, such as the UK, can defer significant and potentially disruptive changes until it is clear what the post-Covid-19 landscape looks like. Nonetheless, despite this ability, the temptation to seize the moment may be hard for policy makers to resist.

Conclusion

For now, in the UK, with the transition from the first Coronavirus Job Retention Scheme into the new 'Furlough 2.0', we are clearly seeing the beginning of the shift from support to stimulus. This is likely to see a significant reduction in the intensity of aid, and a reoccurrence of some of the stimulus packages of old.

Environmental tax reliefs will likely play a part in any future stimulus, but beyond this there is much to consider. When people emerge from the lockdown, it is already clear the high street will look very different. Similarly, the use of commercial real estate (whether manufacturing, offices or other) may be heavily affected by the two metre (or potentially one metre) rule and attitudes to commuting.

All this points to the eventual recovery being different to others we have experienced and it will be important that the UK looks again at the tools at its disposal and identifies what type of economy it wants to create. That is a discussion in which we all should participate as, together, we shape a distinctive future for the UK.

The views expressed here are Chris Sanger's own and are not necessarily those of the organisations listed.

The EY Global Stimulus Response Tracker is part of a global suite of related Trackers. These include Trackers addressing the force majeure clause; global mobility-related issues; global trade considerations; global immigration policies; labour and employment law; tax controversy issue; transfer pricing; and US state and local stimulus responses.

Chart 1: Global tax measures by type

Chart 2: G7 tax measures across all tax types

Chart 3: G7 business/corporate income tax measures

Chart 4: 15 largest economies' stimulus repsonses to Covid-19