Spotlight on construction

Share this article

Patrick Crookes and Jimmy Davies look at the introduction of the VAT domestic reverse charge for building and construction services

Key Points

What is the issue?

The introduction of the VAT domestic reverse charge (‘reverse charge’) for organisations working in the construction industry has brought tax back into the spotlight within the sector.

What does it mean to me?

Although very much a change to VAT legislation, this introduction also increases the importance of an organisation’s existing Construction Industry Scheme (‘CIS’) processes.

What can I take away?

The impacts of these changes are wide-ranging; it is crucial for organisations operating in the construction industry to start planning now, to ensure they are ready for the changes from 1 October 2019.

The introduction of the VAT domestic reverse charge (‘reverse charge’) for organisations working in the construction industry has brought tax back into the spotlight within the sector. Although very much a change to VAT legislation, this introduction also increases the importance of an organisation’s existing Construction Industry Scheme (‘CIS’) processes.

CIS has been in operation since the 1970s in its many guises, as a successful mechanism for HMRC to combat a sector perceived as high risk for fraud and the evasion of tax. CIS enables HMRC to increase the likelihood of tax being collected on payments made between businesses within the construction industry, especially further down the chain where payments were historically more likely to be made in cash (although over the last five years this has become less common).

The new reverse charge legislation, announced at the Autumn Budget 2017, has been designed based on technical consultations between HMRC and various stakeholders which took place during June and July 2017. In the construction industry, the new legislation means that the customer (i.e. the one making payment for construction services) in the transaction will now become responsible for accounting for VAT. Further detailed guidance is expected from HMRC before this legislation becomes effective on 1 October 2019.

Although the rationale behind CIS is understandable, its operation – including the entities and payments to which the scheme applies, is less clear. As a result, errors often arise in its compliance. This complexity for the sector is now set to increase, as the scope of the reverse charge will be aligned to the definition of construction operations for the purposes of CIS.

Why is the Government making this change?

The construction industry is seen as a high-risk sector for fraud and the evasion of tax. In recent times there has been an increase in organised crime groups setting up businesses with the intention of fraudulently failing to pay VAT and making incorrect tax deductions through CIS, through ‘phoenix trading’. Knowingly fraudulent businesses use similar techniques to those used in Missing Trader Intra-Community fraud. For these reasons HMRC has stepped up its activity in the sector and continually invests in resource to reduce the losses caused by this type of fraud.

CIS has been in place to help counter any evasion of direct taxes (income tax and NIC). However, there has not been a similar mechanism for indirect taxes (VAT). By introducing the domestic reverse charge in the sector, the Government is looking to counter any loss of VAT to the Exchequer by stopping the fraud at source, following existing mechanisms in place in the telecoms and energy sectors. A reverse charge mechanism in the construction industry is also common in other EU member states.

What is the impact of the domestic reverse charge?

The Government has confirmed the following:

- To prevent the provider of the goods or services from disappearing or failing to pay the VAT due, the purchaser of the goods or services (the customer, not the supplier) will account for the VAT due to HMRC by declaring the VAT due as output tax on its VAT return. The purchaser will also be able to reclaim the VAT as input tax under the normal rules.

- The domestic reverse charge will apply from 1 October 2019, to give time for businesses to incorporate the new rules into their existing processes, including accounting and IT systems.

- Sales to an end user (a business that does not make supplies of construction services) or a domestic customer will be outside the scope of the reverse charge.

- To prevent anti-avoidance, there will be no threshold to exclude any business, widening the scope of the changes.

- Affected businesses will have statutory invoicing and reporting requirements similar to other reverse charges.

- Organisations will not be required to operate the reverse charge on exempt or zero rated supplies.

What is the role of the end-user?

Under the new legislation, end-users will be the recipients who use the construction services or building for themselves, and do not sell the services on as part of their business operations. This will include landlords and tenants connected to the end user.

An end-user for the purposes of the reverse charge is likely to be considered a deemed contractor for CIS, i.e. a supermarket, retailer, property investment company which will not sell its services as part of its business operations.

If an organisation considers that it is an end user for the reverse charge, it should make the contractor aware of this fact to ensure VAT is charged in the normal way. HMRC guidance suggests that the end user should inform the contractor in a written form which should be retained for future reference.

If the end user does not provide its supplier with confirmation of its end user status it will still be responsible for accounting for VAT under the reverse charge.

What payments will be included within the domestic reverse charge?

As part of its revised scope, the reverse charge will be applicable to what are regarded as construction operations for CIS purposes. As a result, this complex area has been brought back into the spotlight.

‘Construction Operations’ are considered by HMRC to include any of the following activities which are undertaken in the UK and within 12 miles of its territorial waters:

- construction

- alteration

- repair

- extension

- demolition

- dismantling

However, there are a number of exclusions to the term ‘Construction Operations’, including:

- Anything that is clearly not construction related – i.e. running of canteen, hostel, medical, safety, security or temporary office facilities

- Professional services in a purely consultative capacity, i.e. inspection and testing

- Minor repairs of systems

- Replacement of integral systems

- Installation of door entry systems (consisting of no more than electronic lock and voice communication system)

What complicates matters within CIS is that there is a fine line between the above exclusions being outside and within the scheme. Any of the above work may be excluded on a standalone basis, but when undertaken under a contract which includes works which are within the scheme, the ‘mixed contract’ rules apply, and the entire works fall within the scheme.

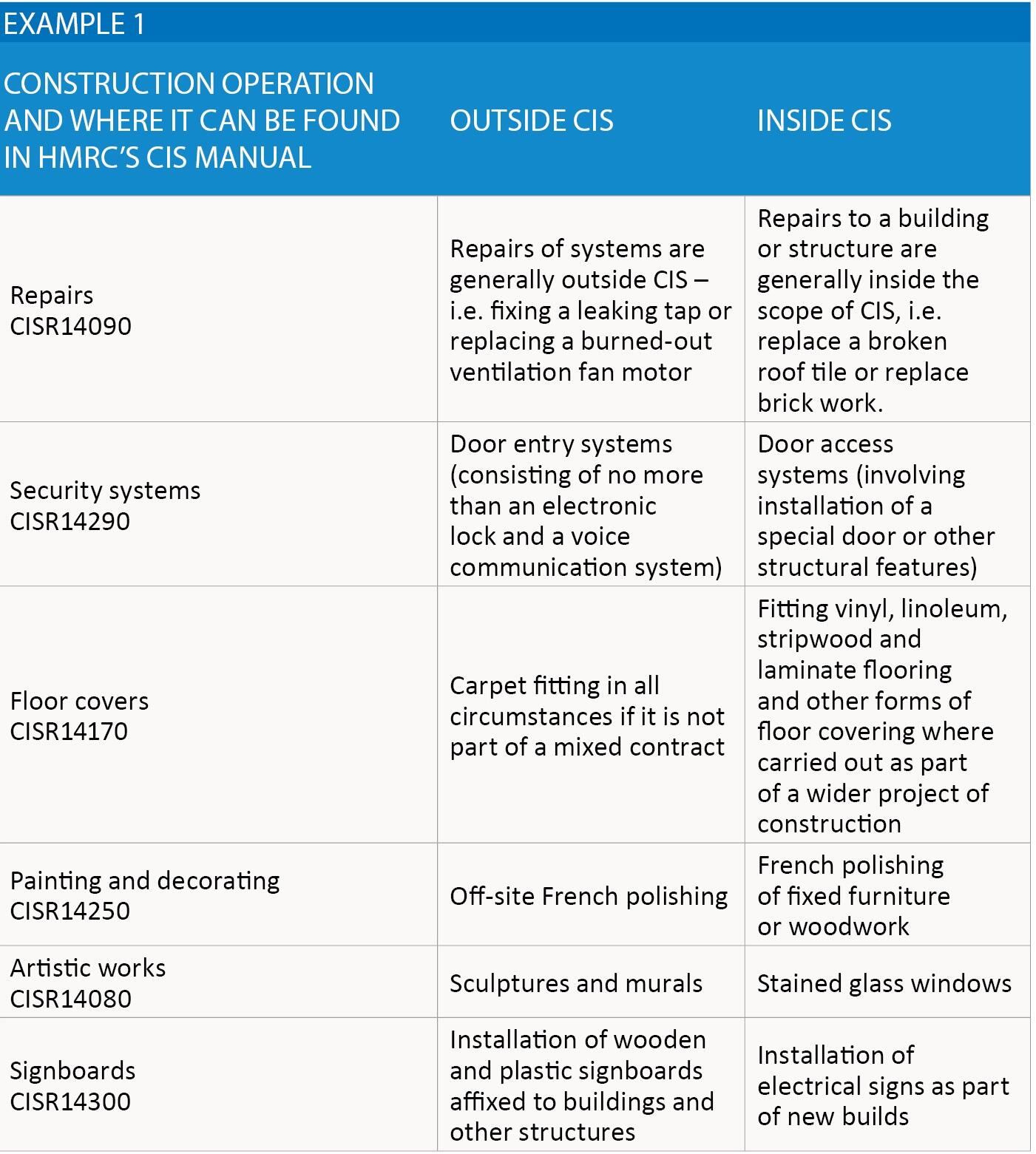

Even before we consider the mixed contract rules, there are anomalies in HMRC guidance which can bring a perceived excluded construction operation within CIS, as set out in example 1.

Organisations which are required to operate as contractors within CIS are required to understand these variances in order to correctly operate the scheme. A misinterpretation of the above rules can lead to underpayments to HMRC, and a large cost (including penalties) to the contractor.

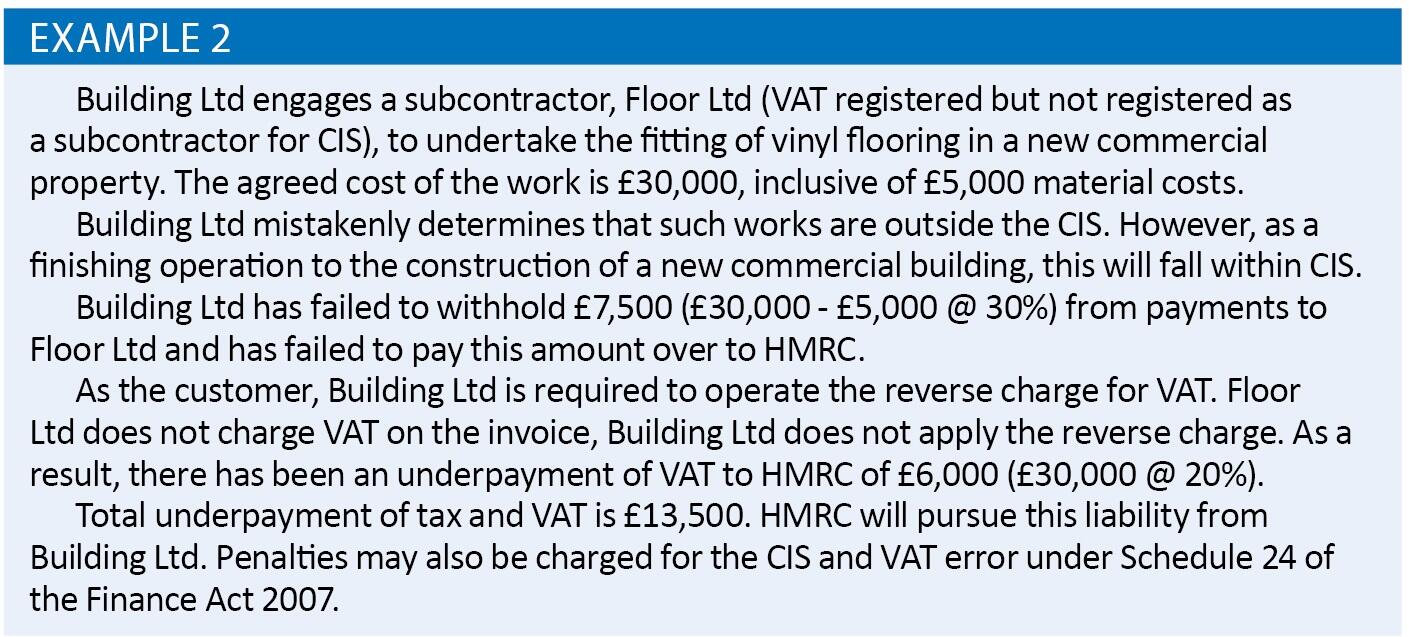

Such potential costs will be compounded from October 2019 where any VAT errors are also made by the supplier of the works, as set out in example 2.

In the above example, any underpayment is the responsibility of the contractor for CIS and customer for VAT (the contractor and customer are one and the same here). Although for CIS purposes, HMRC can apply concessions to offset the CIS liability under Regulation 9(5) SI2005/2045 if they believe there is a reasonable excuse under Regulation 9(3) SI2005/2045 or they are satisfied the subcontractor has included the income in their own self-assessment tax return and paid the tax due under Regulation 9(4) SI2005/2045, such reliefs are not automatic.

In reality, contractors often find themselves making an underpayment in a tax year in which the subcontractor has not yet been required to file a tax return and pay the tax due. In this situation HMRC does not pursue the subcontractor, and would leave both parties to settle the matter themselves.

If the subcontractor agrees to reimburse the contractor for the amounts paid to HMRC on its behalf, which it is not obliged to do under tax legislation, the subcontractor can obtain a repayment from HMRC by providing evidence of making good the amount to the contractor and also including the income in its own self-assessment tax return.

What are the reporting and invoicing requirements?

Affected businesses will have reporting and invoicing requirements that may, at first, seem counterintuitive to those who have no experience of the reverse charge. The supplier is still required to issue a valid VAT invoice, and this must include all of the information normally required on a VAT invoice. This should include reference to the amount of VAT liable on the supply; however, the supplier must not charge this as VAT on the invoice. Instead, the supplier must directly reference that the VAT reverse charge applies to the supply. HMRC have confirmed that the following reference will meet the invoicing requirements:

‘Reverse charge: VAT Act 1994 Section 55A applies’

Unlike standard VAT accounting procedures, businesses making reverse charge supplies must not account for the amount of VAT subject to the reverse charge in the box 1 figure on the VAT return. Instead, the customer will account for the amount of VAT due under the reverse charge in its box 1 figure. The amount of VAT payable as output tax will also be reclaimable as input tax in the customer’s box 4, subject to the normal partial exemption rules. The supplier should account for outputs (net sales) in box 6, and the customer should account for inputs (net sales) in box 7 using the usual accounting procedure.

Will there be any changes to the Construction Industry Scheme (CIS)?

During the consultation process for the reverse charge, the Government discussed the potential to change the criteria for subcontractors looking to obtain gross payment status (i.e. receive payment without deduction of tax). However, as this could impact compliant businesses adversely, this change has not been enacted. Instead, HMRC has stated it will increase its review of the compliance test to look for evidence of fraudulent activity.

Despite no legislative changes to CIS we have seen increased activity from HMRC within the sector, including compliance visits where a number of common errors have been identified by HMRC.

Typical compliance errors which often arise in CIS include:

- Failure to determine that a construction contract is within CIS;

- Incorrectly excluding activities from CIS;

- Subcontractors overstating material elements or including the cost of their own plant or their own scaffolding as a deduction;

- VAT registered subcontractors including VAT as part of their material costs; and

- Failure to apply CIS to certain recharges between entities within an organisation.

Summary

The impacts of these changes are wide-ranging; it is crucial for organisations operating in the construction industry to start planning now, to ensure they are ready for the changes from 1 October 2019.

Key action points include:

- Training key internal stakeholders with responsibility for aspects of your existing CIS processes – typically Finance, Accounts Payable, Procurement, Quantity Surveyors and Payroll staff.

- Ensure the organisation is clear on the operations which are within the scope of CIS and the reverse charge.

- System reviews – update VAT accounting and invoicing procedures / policies to ensure the domestic reverse charge is applied correctly.

- Determining if an organisation is an end user for the reverse charge, and if so ensuring the correct VAT treatment is applied.

- How to apply the reverse charge if you are within the Flat Rate Scheme.

Although HMRC has stated that it will operate a light touch period for errors made in the first six months from implementation for the reverse charge, preparation is key to ensure a smooth transition into the new rules from 1 October 2019.

CIS rules remain the same, and organisations within the sector should use this opportunity to revisit processes in this area to minimise exposure to underpayments and penalties.