Caught in the claw

Share this article

Neil Warren explains when input tax claimed or not claimed by a business might need to be adjusted in the future if it changes its intentions

Key Points

What is the issue?

Many business owners are unaware that if they claim input tax based on an intention to make future taxable supplies, this claim might need to be reduced or repaid if there is a change in trading plans so that the expense instead relates to actual exempt use. The rules work both ways: a non-claim of input tax because of a link to intended exempt use can be adjusted with a future claim if the first actual use is for taxable purposes.

What does it mean to me?

The payback and clawback rules are particularly relevant to construction projects. So it is important that clients alert advisers to any changes in their intentions, which changes the VAT liability of their income from taxable to exempt or vice versa, e.g. a decision by a developer to rent out rather than sell the units in a new block of flats.

What can I take away?

The time period for the payback and clawback regulations is six years after input tax was first claimed, rather than the usual four year period that applies for correcting past errors on returns. A payback or clawback adjustment is not an error correction situation – so it is always included on a VAT return.

Can you think of three situations in the VAT world when the relevant time period to consider is more than four years? The four-year period is relevant to adjusting errors on past VAT returns but it is not relevant to every VAT situation that we deal with in practice. For example, a late VAT registration can be backdated by HMRC as far as 20 years and its power to collect tax that has been fraudulently evaded also extends to 20 years rather than four. And in the case of the payback and clawback rules (considered in this article), the relevant time period is six years.

Basic rules

The legislation for the payback and clawback rules is contained in 1995 VAT Regulations, SI1995/2518, Regs. 108 to 110 and are only concerned with input tax issues:

The payback rules apply when an expense is intended to be used for exempt purposes (so input tax is not claimed) but a taxpayer’s business plans change in the future and it becomes relevant to a taxable activity (so input tax can be claimed when the decision is made to change the nature of the activity).

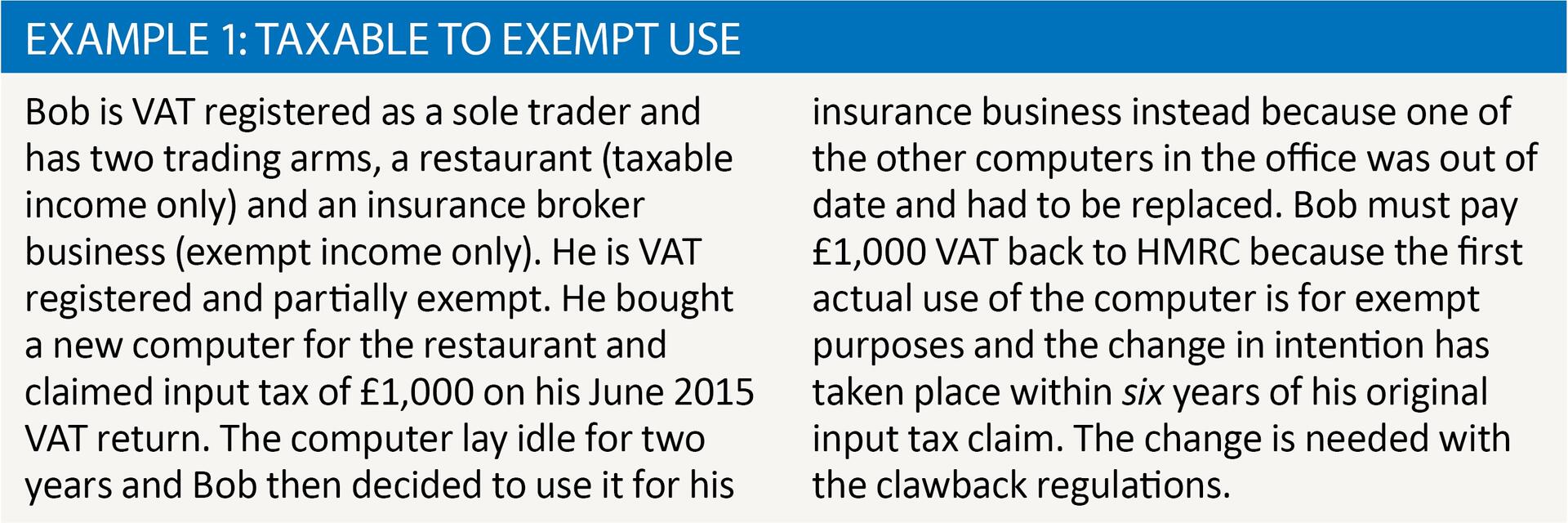

The clawback rules deal with the opposite situation i.e. input tax is claimed based on intended taxable use but then the actual activity generates exempt use so the input tax is repaid to HMRC on the VAT return that coincides with the change of plans. See example 1.

It is all about the first use of an expense or activity. The rules also apply when a mixed use outcome is evident i.e. a change of intention from generating wholly taxable or wholly exempt income to one that generates both taxable and exempt income or vice versa (so the input tax either starts or finishes as ‘residual input tax’ in terms of partial exemption).

Reference: VAT Notice 706, section 13.

Six year adjustment period

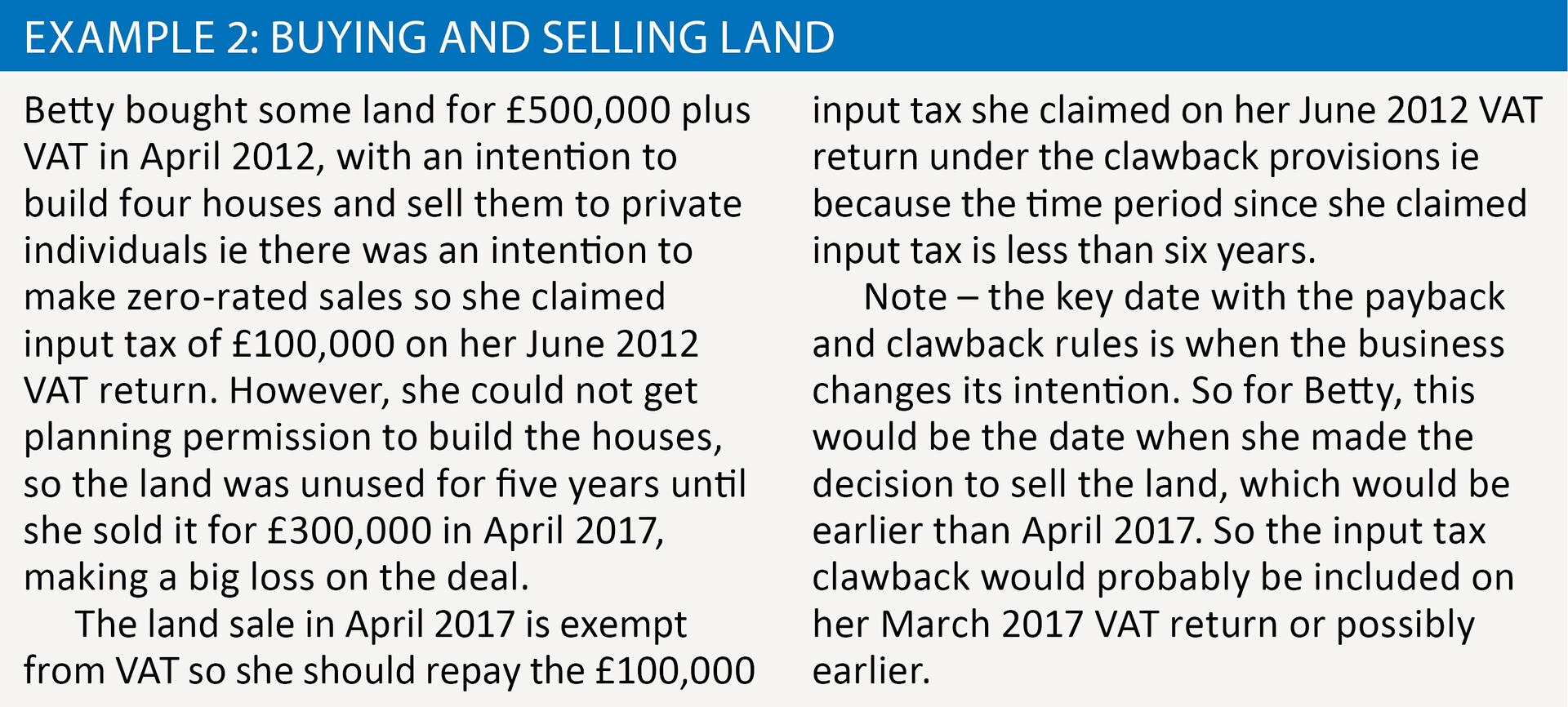

My final sentence in the example about Bob highlighted the point I made in the opening paragraph about a six-year period being relevant for the payback and clawback rules. This can sometimes be very significant – see example 2.

As you have probably guessed, a potential option for Betty would have been to opt to tax the land in question before she sold it (complete VAT1614A and submit it to HMRC before exchange of contracts), so that the sale in April 2017 was subject to 20% VAT. The clawback rules are no longer relevant because she is still making a taxable sale, so there is no change in intention from taxable to exempt activities. The input tax claimed in 2012 would not need to be repaid. Hopefully the person buying the land would be able to claim input tax, but even if this was not the case, a £60,000 output tax payment is better than a £100,000 loss of input tax.

Overall, however, the key point I am highlighting is that the advice for Betty to opt to tax the land in question before she sold it would firstly require an understanding that the time period for the payback and clawback regulations is six years rather than four. Betty did not make any error in June 2012 – she was entitled to claim input tax because of her intention to build and sell new dwellings, so the four year error correction period is irrelevant and it is all about the six year time scale that applies for the payback and clawback rules.

Residual input tax adjustments

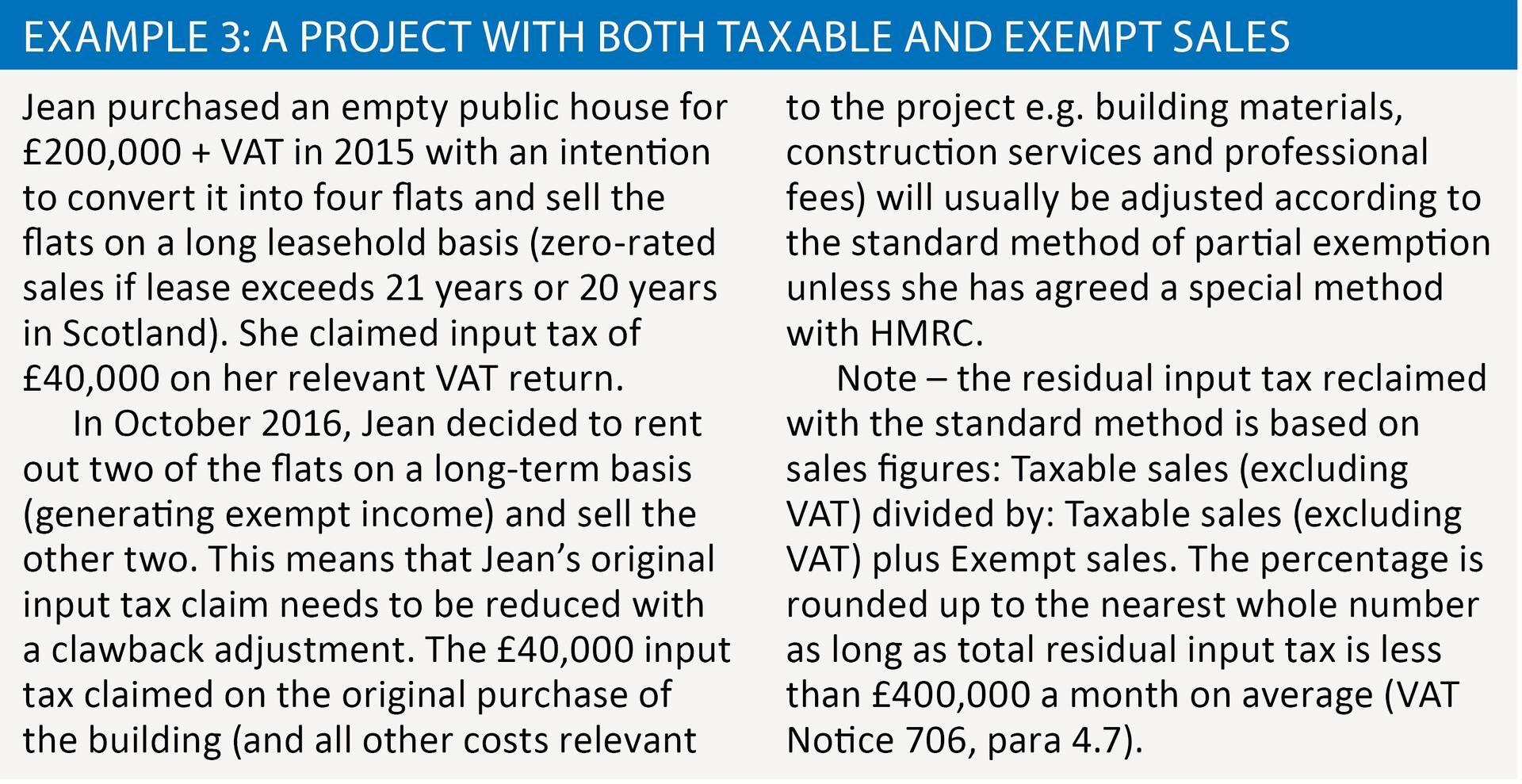

I have so far considered situations when an intention changes from making wholly taxable to wholly exempt supplies or vice versa. But how are calculations made when a mixed use is relevant i.e. where we need to adjust residual input tax? See example 3.

A useful opportunity for Jean, explained in VAT Notice 706, para 13.8, is that she can base her clawback adjustment on a ‘fair’ method of apportionment, rather than the usual standard method based on income. This assumes she did not have a special method in place when she first incurred the input tax in 2015. So she could perhaps do an apportionment based on the square footage of the flats or the number of taxable and exempt units i.e. two rented units and two that are sold would mean an input tax recovery rate of 50%.

Temporary renting out of dwellings

Most of us remember the years of the economic downturn back in 2008 and 2009, when a major problem was that building developers could not easily sell the new dwellings they had constructed. In order to generate cash flow, many of these dwellings were rented out on a short-term basis, with a view to selling them when economic conditions improved. However, this decision to generate exempt rental income rather than zero-rated sales of new dwellings created a challenge with the clawback rules. HMRC clarified its position on such arrangements by issuing VAT Information Sheet 07/08 in September 2008. The basic principle agreed by HMRC is that a business can look at the life of a dwelling over a ten-year period. So if there is an intention to rent out for 12 months and then sell the dwelling, this means a 90% taxable use of the property and therefore 90% of the input tax can be treated as taxable input tax as far as partial exemption is concerned, and hopefully the remaining 10% balance is within the partial exemption de minimis limits and can be claimed as well. I won’t extend further on these procedures but they are still relevant nearly ten years after the Information Sheet was first issued, as confirmed by VAT Notice 706, para 13.12.

Final tips

If you have any payback outcomes, then be aware that you need to write to HMRC and get their permission to include the input tax windfall on the next VAT return submitted by the business (VAT Notice 706, para 13.8). And finally, be aware that since 1 January 2011, the payback and clawback provisions must also be applied to non-business expenditure (including private use), as long as there was some intended business use (taxable or exempt) at the time it was incurred. The actual business/taxable/exempt use must then be adjusted when the item is first used (or the intention changes) and actual use is different to intended use (VAT Notice 706, para 13.16).