Residential conversions: VAT saving opportunities

Share this article

We consider how can you minimise the VAT bill when you are converting a non-residential building into dwellings.

Key Points

What is the issue?

Residential conversions are expected to increase in the coming years, so it is important that developers utilise the VAT saving opportunities in the legislation.

What does it mean to me?

Developers should be clear that a change in their intentions – for example, deciding to rent rather than sell the converted units – will have an impact on input tax claimed in the previous six years because of the payback and clawback rules.

What can I take away?

Timing is important. Form VAT1614D must be issued to the property owner before the deal takes place; otherwise the developer must pay VAT on the buying price if the seller has opted to tax the building, which will create cash flow challenges and extra stamp duty land tax costs.

The brainchild of this article came when I visited a pub near my local theatre, only to discover that it had permanently closed its doors and will be converted into apartments. A quick question to the impressive new AI link on my mobile phone revealed that pubs in England, Scotland and Wales are closing at a ‘rate of more than three per day, an alarming increase compared to 2023’.

In this article, I will consider the VAT issues of a developer buying a pub – or any non-residential building – and converting it into dwellings, focusing on the VAT saving opportunities of these arrangements.

Buying the building: form VAT1614D

Let us call our imaginary developer Marple Developers Ltd, which will purchase the freehold of The White Swan in St Mary Mead from Poirot Brewery and convert it into six apartments, which will then be sold at a profit.

The first challenge is to check whether Poirot Brewery has opted to tax its interest in the building; i.e. will it charge 20% VAT on the sale proceeds? Even if Marple can claim input tax on the project costs – see Input tax below – there are two benefits in not being charged VAT:

- Stamp duty land tax: SDLT is charged on the VAT inclusive price of a deal, so there will be an extra 5% cost on the VAT element.

- Cash flow: There is a cash flow challenge in paying VAT on the completion date and waiting up to three months to claim input tax from HMRC on a return.

There is an escape route for Marple: if a director completes and signs HMRC’s form VAT1614D to confirm the company’s intention to convert the pub into dwellings, the purchase will be exempt from VAT; i.e. the brewery’s option to tax election is overridden:

- The form must be given to Poirot before the price is legally fixed, usually before exchange of contracts.

- It should be signed by a responsible person.

- The form will not be sent to HMRC but retained by Poirot in the event of a future compliance review.

A question I was sometimes asked when I was on the speaking circuit was whether planning permission had to be in place to convert a non-residential building into dwellings before form VAT1614D could be issued to the seller. The answer is ‘no’ because the form is only certifying a buyer’s intention to convert it into dwellings. However, a buyer should retain commercial evidence to prove that this ‘intention’ is genuine, such as surveyor reports, marketing data about future sales, and business plans.

Note: Form VAT1614D can also be used when the buyer intends to convert a non-residential building into a building which will be used for a ‘relevant residential purpose’, such as an elderly care home or student accommodation (see VAT Notice 742A para 3.4.1).

Builder services: 5% VAT

Marple Developers is now the proud owner of The White Swan. Its building contractors are standing outside the building with their spades and are ready to start work:

- Construction services that relate to the conversion of a non-residential building into a residential building – including dwellings – are subject to 5% VAT. This reduced rate also applies to materials supplied by builders as part of their work.

- For dwellings, contractors do not require any certificate from the developer to confirm the 5% rate (see VAT Notice 708 s 17).

- The 5% rate applies to all construction work, such as that carried out by electricians, plumbers, bricklayers, decorators and so on. However, it does not apply to the professional services of, say, architects, project managers or surveyors, which are always standard rated.

- The exception with professional fees is when a contractor agrees a ‘design and build’ contract with the property owner, so that the professionals will supply their services to the contractor. In this case, the 5% rate will extend to professional services.

See Value Added Tax Act 1994 Sch 7A Group 6.

Input tax

Marple Developers has paid 5% VAT to builders and 20% VAT to professionals. It has also paid 20% VAT to builders merchants for materials that it has purchased without labour. The challenge is to reclaim this VAT as input tax, which will be possible because of its intention to sell the completed dwellings on either a freehold basis or with a lease exceeding 21 years (or 20 years in Scotland), in which case the sales will be zero-rated.

Note: I have assumed in this case study that The White Swan was wholly used as a commercial building and was not partly residential.

Change in intention

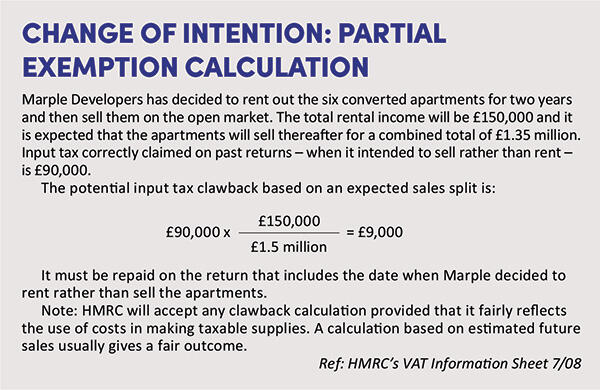

Let us put a spanner in the building works. The property market has slowed and Marple has decided to rent out the completed apartments on a buy-to-let basis. It intends to sell them in the future when the market will hopefully be stronger:

- Buy-to-let rental income is exempt from VAT and input tax is therefore blocked by partial exemption (see VAT Notice 706).

- The starting point is that input tax previously claimed by Marple – on the basis of its intention to make zero-rated sales – must be repaid to HMRC on the return that includes the date when it changed its plans; i.e. deciding to rent rather than sell. This outcome is known in VAT speak as the ‘payback and clawback rules’. The time window for adjusting past input tax claims is six years.

- The payback and clawback rules work both ways: if Marple did not claim input tax because it intended to make exempt supplies, this tax could be subsequently reclaimed if it changed its intentions and decided to sell rather than rent out the completed apartments; i.e. making taxable sales instead.

- It is all about the first supply as far as the payback and clawback rules are concerned.

Two solutions

The input tax repayment to HMRC with the payback and clawback rules will be as welcome to Marple as a police sniffer dog with a heavy cold but there are two possible solutions:

- Solution 1: Marple could sell the completed dwellings to a connected party; e.g. a separate limited company or different legal entity to the one that has converted them. The sales will be zero-rated and so avoid an input tax problem; and the connected party will generate the rental income. This strategy is accepted by HMRC as legitimate tax planning but the impact of other taxes must be considered.

- Solution 2: The company could make a dual purpose input tax calculation if the rental arrangement is intended to be a temporary measure (see Change of intention: partial exemption calculation).

Final twist: part commercial use

Imagine that we have an Agatha Christie twist to the tale. Before buying the building, Marple decided to retain, say, the ground floor of the pub for commercial use, perhaps a shop, and only convert the two upper floors into dwellings. The VAT position has changed:

- Form VAT1614D can still be issued to Poirot Brewery but it will only apply to the parts of the building that will be converted into dwellings. It will be logical on a floor-by-floor basis for two-thirds of the selling price to be exempt, and that 20% VAT will be charged on the one-third element for the ground floor.

- The builder services will be subject to 5% VAT for work on the two upper floors but 20% VAT will be charged for work on the ground floor.

- If construction services are relevant to all parts of the building – such as roofing work or ground floor foundations – the VAT charged by the builders must be apportioned on a fair and reasonable basis.

- To claim input tax on the ground floor building work, it might be sensible for Marple to opt to tax its interest in the building, so that future rental income or other supplies earned from the ground floor shop will be standard rated. The partial exemption challenge has gone away.

Conclusion

The legislation is intended to encourage the construction of extra dwellings in the UK, hence why the generous VAT concessions considered in this article are so important.

An annual government target of 1.5 million new UK homes means that residential conversions will be an important part of this ambitious target. To complete the loop, I have summarised the key issues (see VAT saving tips: residential conversions).

VAT saving tips: residential conversions

- Ensure that form VAT1614D is issued to the owner of the commercial property if they have opted to tax their interest in the building; i.e. so that the purchase is exempt rather than standard rated.

- Builders should only charge 5% VAT on their services, including the materials they supply as part of their work.

- Developers can claim input tax on all project costs if they intend to sell the dwellings when they are completed on either a freehold or long leasehold basis; i.e. because they are making taxable sales.

- If a conversion project is part commercial and part residential, the developer should consider making an option to tax election with HMRC so that VAT is charged on income it earns from the commercial unit(s), therefore avoiding a partial exemption problem. The election is overridden as far as residential units are concerned. (See VAT Notice 742A s 3.)

- If a developer changes their intention from selling to renting when the conversion has been completed – or vice versa – they should consider the implications of the payback and clawback rules to adjust input tax claims for the last six years.

© Getty images