CBAM in 2025 and beyond: what you need to know

Share this article

As the EU’s Carbon Border Adjustment Mechanism (CBAM) and its UK counterpart near full implementation, importers must be prepared for the imminent changes relating to carbon emissions.

Key Points

What is the issue?

The EU has been refining its CBAM framework during its transitional phase, which continues until the end of 2025. Importers are required to submit quarterly reports on the greenhouse gas emissions of their imports, though certificate purchases – the actual mechanism for payment – are deferred until 2027. Following its departure from the EU, the UK has developed its own similar CBAM, set to commence on 1 January 2027.

What does it mean to me?

At the UK-EU Summit on 19 May 2025, both parties committed to linking their ETS systems and exploring mutual exemptions to avoid double taxation. This includes harmonising reporting and verification methodologies, addressing differences in carbon pricing, and ensuring compatibility between the two regimes.

What can I take away?

Businesses importing into either the EU or the UK need to prepare for robust reporting requirements on embedded carbon emissions. Immediate priorities include establishing robust systems for tracking imports, collecting accurate emissions data, and engaging with suppliers.

The Carbon Border Adjustment Mechanism (CBAM) has developed rapidly from a policy concept into a central pillar of climate and trade regulation in Europe and is on its way to becoming the most high-profile ‘carbon tax’ implemented to date.

At its core, CBAM is the European Union’s response to the risk of ‘carbon leakage’: the scenario where companies shift production to countries with weaker climate rules, undermining the EU’s efforts to reduce greenhouse gas emissions. By placing a carbon price on certain imported goods, CBAM ensures that these imports face a cost comparable to that paid by EU producers under the Emissions Trading System (ETS). Ultimately, the mechanism aims to make things fairer, encourage cleaner global manufacturing, and help the EU to achieve its ambitious climate targets.

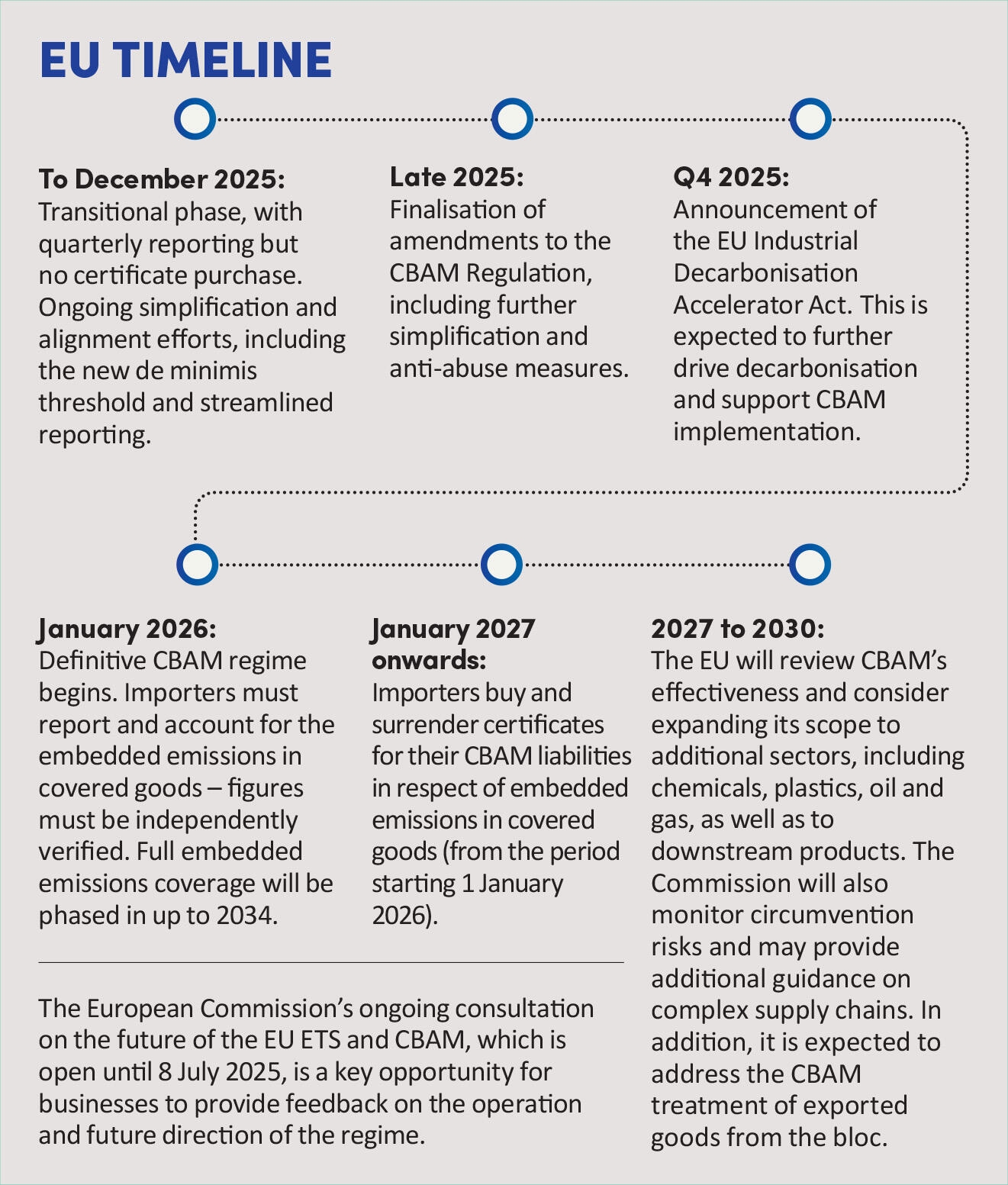

The EU CBAM’s transitional (or reporting) phase began in October 2023. During this period, which runs until the end of 2025, importers of high-carbon goods – such as iron and steel, cement, aluminium, fertilisers, hydrogen and electricity – are required to submit quarterly reports detailing the greenhouse gas emissions embedded in their imports. However, they are not yet required to purchase CBAM certificates (the means by which payment of the new carbon tax is to be made in the EU). This ‘soft launch’ gives businesses and regulators time to adapt before the full, financially binding regime comes into force from the start of 2026.

Meanwhile, the UK has developed its own CBAM. The UK’s version will start on 1 January 2027 and closely mirrors the EU’s approach in many respects, although there are differences in scope, timing and administration. Both systems remain under active consultation and refinement, reflecting the complexity and significance of this new tax and regulatory landscape.

Recent EU Updates

The EU has been actively refining CBAM in response to feedback from businesses and the practical lessons learned from the collation of data (or the lack thereof) during the transitional phase. In early 2025, the European Commission launched a major simplification package, which included a new de minimis threshold: importers bringing in less than 50 tonnes of CBAM goods per year are now exempt from reporting. This move should remove about 90% of importers from the reporting burden while still capturing the vast majority of emissions, thus making compliance easier for smaller businesses.

The Commission has also streamlined the authorisation process for CBAM declarants, simplified emissions calculations and introduced stronger anti-abuse and anti-circumvention measures. For example, EU-origin precursors are now de facto excluded from CBAM reporting, as they are already covered by the ETS. The reporting threshold is now based on annual tonnage rather than value per consignment, providing greater clarity and predictability.

From 2026, the definitive CBAM regime will require importers to report the embedded emissions in covered imports and calculate their consequential CBAM liabilities, with the purchase and surrender of CBAM certificates for every tonne of CO₂ equivalent embedded in their covered imports beginning from the start of 2027. The EU will peg the price of these certificates to the weekly average of the EU ETS allowance price. Notably, the deadline for CBAM declarations and certificate surrender is being extended from 31 May to 31 August each year, giving more time to gather data and reducing the risk of non-compliance due to tight deadlines.

However, penalties for non-compliance will be significant. During the transitional phase, fines can range from €10 to €50 per tonne of unreported emissions; however, from 2026, failing to surrender enough certificates will result in a penalty of €100 per tonne, adjusted for inflation. The EU may bar persistent offenders from importing CBAM goods into the Single Market and could publicly name and shame them.

The European Commission is currently running a public consultation on the future of the EU ETS and CBAM, open until 8 July 2025, which is gathering stakeholder feedback on the effectiveness of the existing regime and potential changes. Separately, the expansion of CBAM to new sectors and products remains under consideration. The Commission has also announced plans for an EU Industrial Decarbonisation Accelerator Act, expected in late 2025, which will further support the implementation of CBAM and drive decarbonisation across European industry.

Recent UK updates

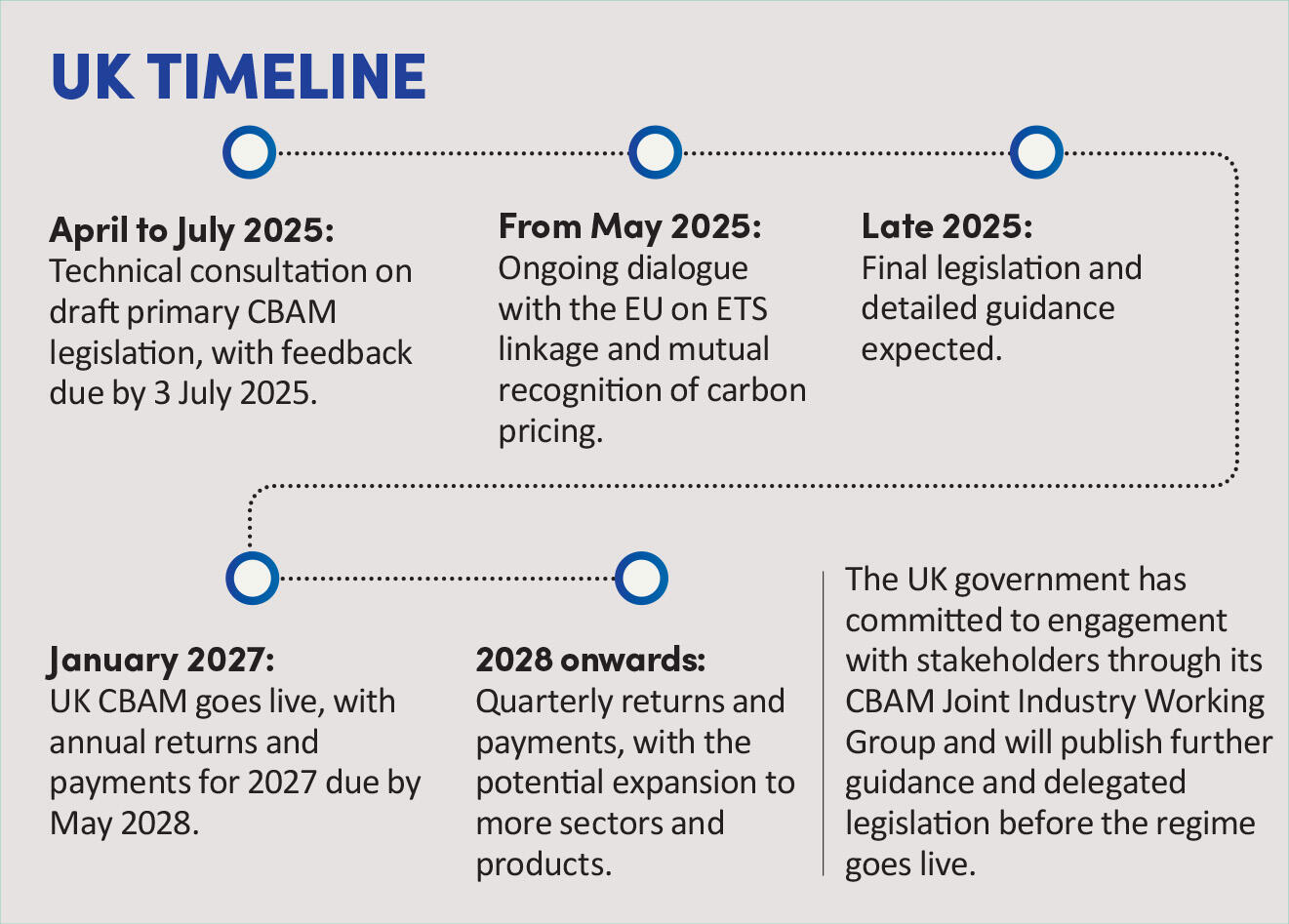

The UK government has taken significant steps in 2025 to advance its own CBAM. On 24 April 2025, HMRC and HM Treasury published draft primary legislation for technical consultation – this runs until 3 July 2025. This technical consultation is not a further review of the policy design itself; rather, it is an opportunity for stakeholders to ensure that the legislation accurately delivers the government’s policy intent.

The government has also published a CBAM policy update, setting out key decisions taken following the response to the 2024 policy consultation.

The UK CBAM will apply from 1 January 2027 to imports of aluminium, cement, fertilisers, hydrogen, iron and steel. Notably, electricity, glass and ceramics are not included in the initial phase but may be added later. The minimum registration threshold has been revised upwards and is now set at £50,000 of CBAM goods imported in a 12 month period, meaning that only larger importers are required to register and comply. There are also detailed provisions for group treatment, allowing connected companies to register as a group and share liability for CBAM payments.

UK importers will need to submit annual CBAM returns for 2027, with payments due by May 2028. The first return will cover the entirety of 2027 in one 12 month period, before the system moves to quarterly returns from the start of 2028 onwards. Emissions data must be verified by an accredited body, and default values will be used where such data isn’t available. The UK also confirmed that it will exclude imported scrap products from the aluminium and iron and steel sectors from CBAM during its initial phase.

Penalties for non-compliance in the UK are expected to mirror those which already exist for VAT, with the possibility of additional administrative or criminal sanctions for deliberate fraud or evasion. The government has established a CBAM Joint Industry Working Group to engage with affected sectors and an International Group to co-ordinate with other governments. And the UK government will also publish further detailed guidance and delegated legislation before implementation.

Closer EU-UK alignment: the 19 May 2025 Summit

The UK-EU Summit on 19 May 2025 marked a turning point in CBAM alignment. Both sides publicly committed to working towards linking their respective Emissions Trading Systems, which would pave the way for mutual exemption from CBAM charges for UK-EU trade.

This would be a win for businesses operating in both markets in respect of reducing double compliance and administrative costs, but there will also be a need to address the divergence in the current carbon prices between the two different ETSs (currently around €70 per tonne under the EU ETS and £40 per tonne under the UK ETS). One can envisage a scenario where if the UK price aligns upwards to meet the EU price, certain sectors of UK industry may view the previous noted ‘win’ as somewhat of a pyrrhic victory (agriculture being one such example).

The summit also highlighted joint efforts to harmonise reporting and verification methodologies, develop robust default values and streamline the authorisation process for importers. Both the EU and UK are working to ensure that their CBAM frameworks are compatible, thus making it easier for businesses to comply, whilst also reducing the risk of trade friction.

While formal linkage and mutual exemption are not yet in place, the intent to make this so is very clear. The EU and UK actively continue negotiating these points, and further steps toward formal alignment are expected in late 2025 and into 2026. One key area of focus is likely to be the differing start dates of the respective live (or definitive) regimes. A failure to align these could result in no exemption being in place between the UK and the EU for 2026, thus placing an additional administrative burden on UK suppliers into the EU, and both additional administrative and cost burdens on EU declarants who are importing affected goods from the UK.

Practical implications for businesses Immediate priorities

For businesses, the most pressing task is to comply with the EU’s transitional reporting requirements. If you import covered goods into the EU, you must submit quarterly CBAM reports detailing the embedded greenhouse gas emissions in your products. From 2026, these reports will require to be independently verified, and businesses will need to buy certificates from the start of 2027 to cover their emissions liability for the period starting 1 January 2026.

UK importers should prepare for similar requirements from 2027, including annual and then quarterly online returns, verified emissions data and online payments in respect of their CBAM liabilities.

Both regimes require robust systems for emissions data collection, supplier engagement and compliance reporting. All the signs are that the use of estimated emissions data in both the UK and EU is likely to be more expensive for businesses than obtaining and reporting actual emissions data. From a commercial perspective, a proactive approach to managing the new tax could involve renegotiating or updating contracts with suppliers to ensure that emissions data is provided and verified, investing in carbon accounting technology and ultimately switching to suppliers who are more advanced in their decarbonisation approach.

Supply chain and data challenges

CBAM compliance is not just a finance or tax issue – it’s a cross-functional challenge. The data needed to comply is often scattered across procurement, operations, sustainability and IT systems. Businesses must work across departments to track imports, collect emissions data and ensure timely, accurate reporting. For many, this means identifying data gaps, training staff and working closely with suppliers, especially those in jurisdictions with less developed carbon reporting systems.

Financial planning

The cost impact of CBAM will depend on the carbon intensity of your imports and the prevailing carbon price – this has fluctuated over recent years (sometimes markedly) whilst steadily ticking ever higher. Businesses should run scenario analyses to estimate their CBAM liabilities and consider supply chain adjustments – such as sourcing from lower-emission suppliers – to manage costs. Taking steps to reduce carbon emissions can lower costs and improve competitiveness.

Penalties and risks

Non-compliance carries significant risks. In the EU, penalties for failing to surrender enough CBAM certificates will be €100 per tonne from 2026, and similarly stringent penalties are expected to apply in the UK. Persistent non-compliance can result in exclusion from the EU Single Market and the UK Internal Market, as well as public ‘naming and shaming’. There are also reputational risks, as customers and investors increasingly expect transparency and climate responsibility from business. In some cases, criminal sanctions could apply for deliberate fraud or evasion.

De minimis threshold

Small importers will benefit from a de minimis exemption: if you import less than 50 tonnes of CBAM goods per year into the EU, you are exempt from reporting and certificate obligations. The UK’s threshold is based on import value (£50,000 per year). However, businesses should keep accurate records to prove that they are under the threshold, as exceeding it – even slightly – will trigger full compliance.

In conclusion

CBAM is more than just another compliance requirement – it’s a major shift in how carbon costs are managed in international trade. For businesses importing into the EU or the UK, the message is clear: act now to get your systems, data and supplier relationships in order. The penalties for non-compliance are steep and the reputational risks are real but there are also opportunities for those who get ahead.

By investing in decarbonisation, strengthening supply chain transparency and engaging with policymakers, businesses can not only avoid pitfalls but also position themselves as leaders in the new low-carbon economy.

The recent UK-EU summit and ongoing regulatory updates signal a future of closer alignment and, potentially, smoother cross-border trade for compliant businesses. However, this new environmental indirect tax landscape – and carbon taxes in particular – will keep evolving, with more sectors likely to be brought into scope and reporting requirements set to become more stringent. We will all have to become used to the idea that carbon accounting will be as central to business operations as traditional financial accounting has been. However, by staying informed, investing in robust compliance systems and pro‑actively managing the new carbon tax, businesses can turn CBAM into a competitive advantage.

© Getty images