Closing the tax gap: government strategy on non-compliance

Share this article

The Spring Statement 2025 brought some real light to bear on HMRC plans to tackle non-compliance and the collection of outstanding debts.

Key Points

What is the issue?

HMRC is intensifying efforts to tackle initial non-compliance and the collection of outstanding tax debts by raising penalties for late VAT payments, hiring more staff and allocating additional resources to its debt management teams. Tax advisers found to be promoting tax avoidance schemes may face suspension from registering with HMRC.

What does it mean to me?

Individuals and businesses should be conscious of HMRC’s commitment to undertaking additional compliance activity, as well as the increased penalties where tax is not paid by the statutory deadline.

What can I take away?

The government is considering a range of measures designed to support HMRC’s efforts to close the tax gap, including significant investment, clearer behavioural guidelines for taxpayers and penalties that are designed to deter non-compliance. The increased investment in HMRC Compliance and Debt Management teams will result in faster action if individuals and businesses fail to meet their tax compliance obligations.

On 26 March 2025, the Chancellor of the Exchequer Rachel Reeves delivered the Spring Statement 2025, unveiling a comprehensive package of measures designed to address the UK’s persistent tax gap. The Autumn Budget 2024 had demonstrated that the government is committed to supporting HMRC’s mission to collect all taxes which are due, and there was anticipation for what may follow in the Spring Statement 2025.

Whilst the Budget announcements in 2024 outlined the measures the government planned to put in place to raise tax revenue, a major update that came from the recent Spring Statement 2025 was the announcement of a package of new measures that HMRC will implement, which are intended to reduce tax debt and close the tax gap, in keeping with the government’s pre-election pledge from April 2024.

HMRC’s most recent ‘Measuring Tax Gaps’ publication, released in June 2025, estimated that the tax gap – which is the difference between the tax which should have been paid in theory and the amount that is actually paid – stood at £46.8 billion in absolute terms in 2023/24.

The measures in the Spring Statement have a stated aim to collect over £1 billion in additional gross tax revenue per year by 2029-30.

Separately, the government estimates that by the end of December 2024, the tax debt owed to HMRC stood at more than £44 billion, of which £20 billion was over 12 months old. The Spring Statement aims to reduce this both by investing in HMRC’s Debt Management team and creating a greater incentive to pay on time by increasing penalties on those who fail to pay their liabilities by the statutory deadlines.

This article examines the four principal strategies outlined in the Spring Statement 2025 to close the tax gap: increasing prosecutions for tax fraud; expanding compliance interventions; raising penalties for late payments; and investing in HMRC debt management staff.

Increasing prosecutions for tax fraud

A central feature of the Spring Statement is the government’s explicit commitment to intensifying the prosecution of tax fraud. HMRC has announced a target to increase the number of charging decisions for tax fraud by 20% by 2029-30. This target will be met by undertaking additional criminal investigations into both companies and individuals.

In cases where HMRC suspects tax fraud, it reserves the right to progress enquiries either through criminal investigation or through its civil investigation procedures, which include cases dealt with under Code of Practice 9 (COP 9). As a result of this commitment, we can expect an increase in the number of criminal investigations that HMRC instigates, either where it is determined that a civil procedure is not appropriate or where a person offered entry into the Contractual Disclosure Facility under COP 9 does not make a full disclosure.

To support this targeted increase in criminal investigations, HMRC is formalising its approach to paying informants. HMRC has always maintained discretion about paying informants, paying £978,256 in 2023-24. The new scheme, modelled on the US and Canadian systems, will reward informants with payments based on a percentage of the tax recovered as a result of their actions.

The language used in the Spring Statement also provides an insight into where these investigations may be targeted. Specific references were made to individuals and companies who make it possible to hide money offshore, and to tax fraud facilitated by those representing large corporations. Whilst not explicitly mentioned, the latter suggests an increased focus on the Corporate Criminal Offence, brought in by the Criminal Finance Act 2017, which can lead to fines and criminal conviction for a company which fails to prevent the facilitation of tax evasion by an associated person.

Expanding compliance activity

To further strengthen tax compliance, the government is investing in additional HMRC staff and resources. The Spring Statement announced the recruitment of 500 new compliance staff, supplementing the 5,000 positions announced in the Autumn Budget. This investment, at a cost of £100 million, is projected to yield an additional £241 million in tax revenue over the next five years.

Over the same period, the government will increase the number of HMRC staff to tackle wealthy offshore non-compliance by 400, which is forecasted to return over £500 million across five years. This will involve bringing in specialists with expertise in wealth management, as well as leveraging AI and analytics to more effectively identify and scrutinise those concealing their wealth.

Focus on tax advisers

HMRC is also looking to strengthen its ability to take action against tax advisers who facilitate non-compliance for their clients. A consultation, which ended on 7 May 2025, asked for views on the introduction of stronger penalties against tax advisers who contribute to the tax gap, including the publication of their details if they are subject to HMRC sanctions, the expansion of information notices that can be issued to tax advisers, and the sharing of information about tax advisers with their professional bodies where appropriate.

These proposals are designed to influence the behaviour of tax advisers by ensuring that they are disincentivised from action that has the potential to increase the tax gap.

The reforms being considered in the consultation follow the Autumn Budget statement that all tax advisers who interact with HMRC must register with HMRC from April 2026. HMRC has stated that this will give it options for compliance enforcement, as tax advisers not meeting the required standards can be suspended from registration. These reforms build on existing powers to take action against ‘promoters of tax avoidance schemes’ and ‘dishonest’ tax agents.

To support taxpayers in meeting their obligations, HMRC is also working on a transformation roadmap to ‘deliver the digital services which will mean a better experience for our 35 million individual taxpayers, for agents, and for the more than 5 million businesses in the UK’, as the Exchequer Secretary announced in March. The Transformation Roadmap is expected to be published in summer 2025 and will set out how HMRC will move towards its ambition to be a fully digital tax authority.

Investing in debt management

Recognising the scale of outstanding tax debt, the government is making a substantial investment in HMRC’s debt management capability. It will recruit 600 additional HMRC Debt Management staff to increase the collection of overdue tax debt, in addition to the 1,800 new recruits announced in the Autumn Budget.

The government will invest £114 million into HMRC’s Debt Management team over the next five years, which is forecasted to ensure the collection of an additional £2.8 billion of tax revenues in the same period. In addition to internal staffing, there are plans to invest £87 million over the next five years in HMRC’s existing partnerships with the private sector debt collection agencies to increase their capacity to collect tax debt.

A key operational change is the reintroduction of ‘direct recovery’ powers, allowing HMRC to recover outstanding tax debts directly from the bank accounts of individuals and companies who have the means to pay but choose not to. This measure is targeted at those who are aware of their liabilities and have the ability to settle them, reinforcing the message that deliberate non-payment will not be tolerated.

HMRC, in partnership with Companies House and the Insolvency Service, has also committed to a joint plan to tackle contrived insolvencies, committing to the increased use of upfront payment demands, making more directors personally liable for company taxes and increasing enforcement sanctions where they suspect ‘phoenixism’.

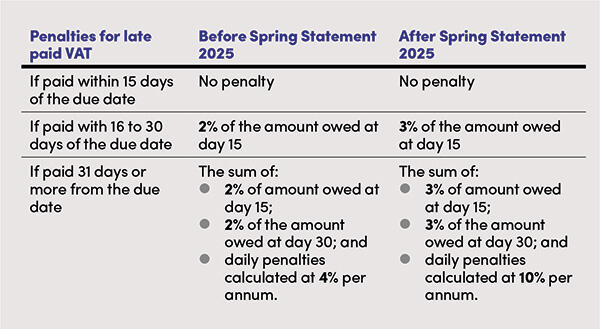

Increased rates on late payment penalties

Late payment penalties are currently in place across all UK tax regimes. From April 2025, HMRC has chosen to increase these penalties specifically for VAT payments, to encourage taxpayers to pay their liabilities on time. Following the Spring Statement 2025, the penalties that applied for late paid VAT were increased significantly (see box).

Penalties will also be increased for income tax self-assessment taxpayers as they join Making Tax Digital for income tax. From April 2026, those with self-employment income of more than £50,000 will be required to file quarterly under Making Tax Digital. From April 2027, this will be extended to those with an income of £30,000 or more. The payment penalty increases for late payment of VAT noted above will also apply to those who join Making Tax Digital. These changes have been put in place to encourage payments to be made on time.

Conclusion

The announcements in the Spring Statement show that the government is committed to introducing measures designed to close the tax gap. For businesses and individuals, it will be more important than ever to understand the potential consequences of not complying with their tax obligations.

Whilst much of the Statement was focused on deliberate non-compliance, it is clear that HMRC scrutiny will not only be confined to intentional behaviour. With the increased investment in HMRC’s compliance staff, there will be more capacity to detect and challenge a wider range of behaviours, including those arising from misunderstanding or a lack of care, particularly where income or assets are held outside of the UK.

Individuals and businesses need to be proactive in maintaining accurate records and seeking professional advice where there is any uncertainty about how tax rules apply in their individual circumstances. They should also be aware of the various routes to make a disclosure to HMRC where they identify historic liabilities that have been unpaid. Those who fail to keep up with their obligations could potentially face investigation and significant penalties as a result.

We would like to thank Lucy Sharrock, Senior Associate, and Polly Pendrich, Associate at PwC, for their assistance with this article.

© Getty images