Cause for complaint

Share this article

Kelly Sizer looks at HMRC’s complaints process and escalation routes

Key Points

What is the issue?

Tax advisers might need to help clients complain to HMRC – this article explains how.

What does it mean to me?

Agents can make a complaint on a client’s behalf, and on upholding the complaint, HMRC can reimburse any reasonable and proportionate fees in so doing.

What can I take away?

Complaining might not just resolve your client’s issue – if it helps to identify a wider problem, it could help to solve it for others.

When should you consider making a complaint to HMRC? The range of circumstances is wide, but HMRC’s complaints process covers most situations in which you would like the Department to put something right, but for which there is no formal right of appeal to the tax tribunal.

One example might be poor HMRC service, such as a staff member being rude or unhelpful which has caused upset. Another might be an HMRC mistake that has caused excessive tax to have been paid, such as HMRC failing to act upon information in its possession, or HMRC giving misleading information to the taxpayer which they have relied upon to their detriment.

If there is a right of appeal against an HMRC decision, the correct course of action is to appeal to HMRC and to follow the usual escalation routes, such as internal review or taking the matter to the tax tribunal. Alternative dispute resolution might also be considered.

This article explains how to make a complaint to HMRC and, if no satisfactory response is received, how to escalate it for independent review.

A note of caution

This article does not cover judicial review.

Complaints will usually relate in some way to HMRC’s administration of the tax system, so they potentially stray into the same territory as judicial review. As explained in Keith Gordan’s article ‘Last chance HMRC’ (Tax Adviser, September 2015), cases might therefore warrant specialist legal advice at an early stage so that any appropriate judicial review application is made at the correct time.

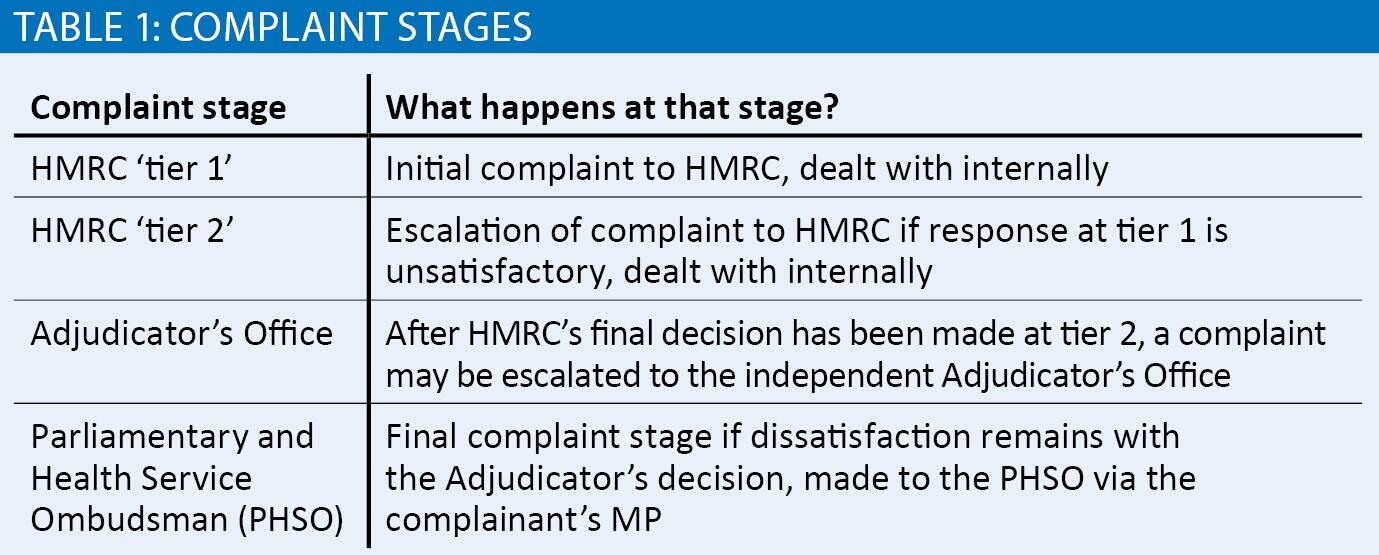

HMRC complaints overview

The overall process for an HMRC-related complaint has four potential stages. These are set out in the table.

As indicated in the table, the stages should be followed in order – for example, the Adjudicator will not take on a case without the full HMRC complaints process having first been exhausted. Similarly, the PHSO will not usually look at cases that have not first been through the Adjudicator’s Office.

Complaints about ‘serious’ allegations of misconduct by HMRC staff (such as assault or corruption) are handled differently. Such complaints are made to HMRC and will be investigated by someone who has not previously been involved with the case. They are overseen by the Independent Office for Police Conduct.

If the complaint relates to data protection, it can be made to HMRC via the usual process but can also be made at any time to the Information Commissioner’s Office.

Public information on HMRC complaints can be found on GOV.UK and HMRC internal guidance is found in two manuals: Complaints Handling Guidance (CHG), and Complaints and Remedy Guidance (CRG).

How can a complaint be made?

HMRC tier 1

Complaints by individuals and unincorporated businesses can be made online by logging in via the Government Gateway. Incorporated businesses cannot complain online.

For those who cannot or do not wish to use the online form, complaints can be made by telephone or letter. Although HMRC say that any expression of dissatisfaction will be handled as a complaint, it is preferable to state clearly that a complaint is being made, for example in the heading of the letter.

An individual can appoint an agent to complain on their behalf (via the usual online or 64-8 channels). However, agents cannot make a complaint online; they have to do so by telephone or letter.

The ability to complain in person has largely been removed due to the closure of Enquiry Centres several years ago. Nevertheless, it should presumably still be possible to make a complaint to an HMRC officer at a face to face meeting, for example if the taxpayer has a home visit from HMRC through its ‘needs enhanced support’ service.

As much information as possible should be included in the complaint. This should include:

- the taxpayer’s full name, address and contact details (or the agent’s contact details if HMRC is to contact the agent in response to the complaint)

- a tax reference, such as National Insurance number, Unique Taxpayer Reference or VAT number

- details of what happened and when

- what outcome is sought

Also include details of any impact on the complainant, such as distress or expenses (which HMRC might refund, see ‘complaint resolution’ below).

If the complaint is about poor HMRC service, you might refer to ‘Your Charter’ and explain how HMRC has fallen short of expectations. It is also helpful to explain whether there are any specific equality issues arising, for example HMRC having failed to make reasonable adjustments for a disabled person.

HMRC noted in a recent webinar on the complaints process that the aim is to respond to complaints within 15 working days. The timeframe might be longer, especially where the issues arising are complex. However, HMRC says it will provide contact details for the officer dealing with the complaint, and keep you informed of progress.

HMRC tier 2

If the outcome of the first complaint to HMRC is unsatisfactory, a review can be sought. A different HMRC officer will review the matter and provide a final response.

Adjudicator’s Office

Once HMRC’s internal complaints process has been exhausted, the matter can be taken further by writing to the Adjudicator’s Office with full details of the complaint and why you are still not satisfied.

A copy of the final HMRC decision letter must be enclosed. This must usually be done within six months, but it is assumed from the use of the word ‘usually’ that cases might be taken on outside this timescale if there is a good reason for the delay.

There is currently no way to complain online to the Adjudicator. However, in correspondence with the Treasury Committee, HMRC has indicated that an online facility will be available later in 2019.

While the Adjudicator’s Office is independent, her review is limited to the extent that it can only consider whether HMRC has handled the complaint correctly in accordance with its own guidelines and given a reasonable decision. She will also not be able to look at complaints relating to whether tax law or an HMRC policy is inherently fair. For example, she might review a complaint that HMRC has not followed its own guidance or published policy (such as an Extra Statutory Concession), but her remit would not extend to whether that guidance or policy was in itself fair.

The Adjudicator will not look at cases where there is an ongoing HMRC enquiry.

Some case studies of the types of complaint the Adjudicator sees and their outcomes can be found in her annual reports.

PHSO

If dissatisfied with the Adjudicator’s decision, complainants have one final escalation route – the Parliamentary and Health Service Ombudsman. This final complaint must be made within a year of the taxpayer first becoming aware of the problem. If this was more than a year ago, the PHSO say that it might still consider it ‘if there were good reasons for the delay’. Given that there is a requirement to first exhaust other avenues, it is assumed that delays incurred in pursuing the complaint with HMRC at tiers 1 and 2 and then with the Adjudicator should qualify as a good reason.

A complaint cannot be made direct to the PHSO; it must be raised via the complainant’s MP. The Parliament UK website gives guidance for those who do not have their own MP (for example, British citizens living abroad) on how to find out which MP to contact.

The PHSO does not investigate all complaints. Some initial checks are made, following which only around 25% of cases are selected for detailed investigation.

Complaint resolution

The actual method of complaint resolution can vary. HMRC may try to resolve the matter by telephoning the complainant. This might cover a simple matter of poor customer service, for example. Otherwise, a written response will be sent.

To resolve complaints, HMRC might offer an apology and in some cases, this will be an end to it.

However, it is probable that most people who have reached the point of complaining might seek some further form of redress. For example, a tax liability could be written off if the circumstances meet Extra Statutory Concession A19 requirements.

Redress is considered on a case by case basis and is made ex gratia. This might be financial, for example a sum to recognise worry or distress; or non-financial, such as a bunch of flowers.

Reimbursement of costs (postage, phone charges etc) that directly relate to the matter under complaint (and in bringing the complaint itself, see CRG5350) will also be considered if they are reasonable and proportionate. HMRC will require receipts for any amounts claimed. Agents’ fees can be included. HMRC would normally expect the complainant to have paid the bill and claim it back, however in limited circumstances such as if the client is in financial hardship or the same problem has affected multiple clients, the agent may be paid direct by HMRC (CRG5275).

Note that the taxpayer will find it an uphill struggle to get HMRC to reimburse them for loss of earnings unless there is very clear evidence that there is a direct correlation between the HMRC mistake and the loss (CRG1575). Also, the cost of one’s own time more generally is not reimbursed. However, HMRC might take this into account generally as part of making a worry and distress payment where there has overall been a significant adverse impact.

If the Adjudicator upholds (fully or in part) a complaint, she will make recommendations to HMRC as to how to put things right. HMRC is not bound to follow those recommendations, but the Adjudicator’s Office website says that HMRC has accepted all recommendations to date.

The PHSO concludes complaints in the same way, by way of making recommendations to HMRC.

Not worth the hassle?

HMRC is a large organisation, dealing with millions of taxpayers every year. Mistakes happen, and complaints will arise. But is there perhaps a tendency not to bother?

Tax advisers might spend time resolving HMRC mistakes for their clients and then not feel able to charge for their time. Alternatively, if charges are made, the client can end up paying to put right HMRC’s mistakes.

Clients might not wish to complain, perhaps fearing that this will trigger a flag on their record, prompting an enquiry! However, HMRC promises not to treat anyone differently because they have made a complaint.

We might also think that it’s not worth the hassle of complaining, if the problem itself has been resolved.

However, while not wishing to burden HMRC’s stretched staff further, it is worth remembering that complaining can be beneficial for reasons other than resolving the immediate client issue. HMRC says that it attempts to learn lessons from complaints cases. The Adjudicator can also report back to HMRC with suggestions for service improvement.

Tracking through complaints can identify problems that can be corrected and avoid a recurrence. HMRC’s equality teams might also identify and address service issues affecting taxpayers with particular needs.

So perhaps it is sometimes worth complaining, if it might prompt HMRC to fix a wider problem? That is not to say that some judgement should not be exercised, especially given that – as noted above – HMRC’s policy is to reimburse only those costs incurred reasonably and proportionately in bringing a complaint, even when fully upheld.