The circular economy: the implications for tax policy

Share this article

We consider how a move towards a circular economy can bridge the gap for sustainable growth – and how this would impact tax policy.

Key Points

What is the issue?

A circular economy moves away from the traditional linear model of ‘take-make-dispose’ and instead focuses on eliminating waste, keeping materials in use and regenerating natural systems. We explore how current tax systems hinder the transition to a circular economy and what changes are needed to support sustainable business models.

What does it mean to me?

While many businesses and governments are adopting circular principles, tax systems create barriers for circular practices such as repair, reuse and remanufacturing, which are often penalised through VAT, customs duties and labour taxes.

What can I take away?

We consider how tax reform – such as adjusting VAT rules, redefining customs classifications and shifting tax burdens from labour to resource use – could better align fiscal policy with environmental goals.

The global economy is increasingly strained by resource depletion and environmental degradation. In response to these challenges, the concept of a circular economy has emerged as a compelling framework for sustainable growth by operating within both social foundations and planetary boundaries. By redefining the traditional linear ‘take-make-dispose’ approach, the circular economy promotes resource efficiency, waste reduction and extended product lifecycles.

While some businesses are progressively embracing circular principles and governments are introducing circular guidelines and policies, most tax systems remain anchored in linear economic models. This misalignment may create significant barriers for circular business models. However, if designed effectively, tax systems have the potential to become powerful enablers of the circular transition.

This article explores the core principles of the circular economy, examines its impact on business models and product lifecycles, and considers the implications for tax policy – supported by practical examples.

The circular economy and its impact

Defining the ‘circular economy’

The circular economy offers a systemic shift away from the traditional linear model of production and consumption, which is based on extracting resources, manufacturing goods and disposing of them after use. Instead, it proposes an economy where waste and pollution are designed out, products and materials remain in use for as long as possible, and natural systems are restored rather than depleted.

Rather than relying on endless resource extraction, the circular economy is built on three core principles (see tinyurl.com/23c5r8m4):

- Eliminate waste and pollution through smarter design and systems thinking.

- Circulate products and materials by keeping them in use at their highest possible value.

- Regenerate nature by designing economic activity to support and restore ecosystems.

This approach not only supports environmental sustainability but also presents new business opportunities. However, as many companies begin to implement circular strategies, they quickly encounter a major structural barrier: most fiscal and regulatory frameworks, especially tax systems, remain rooted in linear logic. They continue to incentivise resource extraction and throughput, while penalising labour-intensive activities like repair, remanufacturing or reuse – core components of circular models.

Circular business models

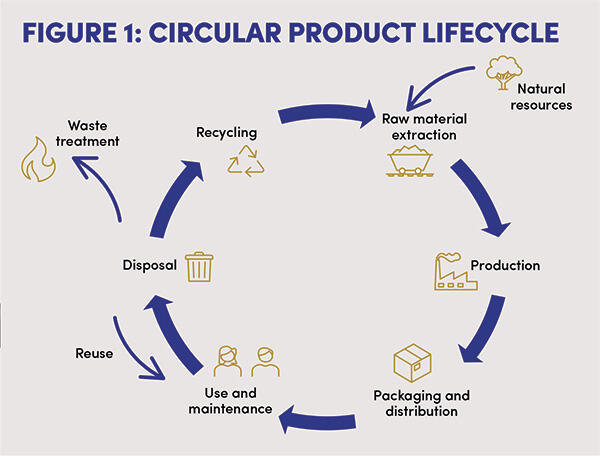

Circular business models translate circular economy principles into practice by rethinking the entire product lifecycle – from design and sourcing to production, use and end-of-life (see Figure 1: Circular product lifecycle).

Unlike linear models that prioritise volume and turnover, circular business models focus on longevity, efficiency and resource optimisation (see bit.ly/4lvNoxk).

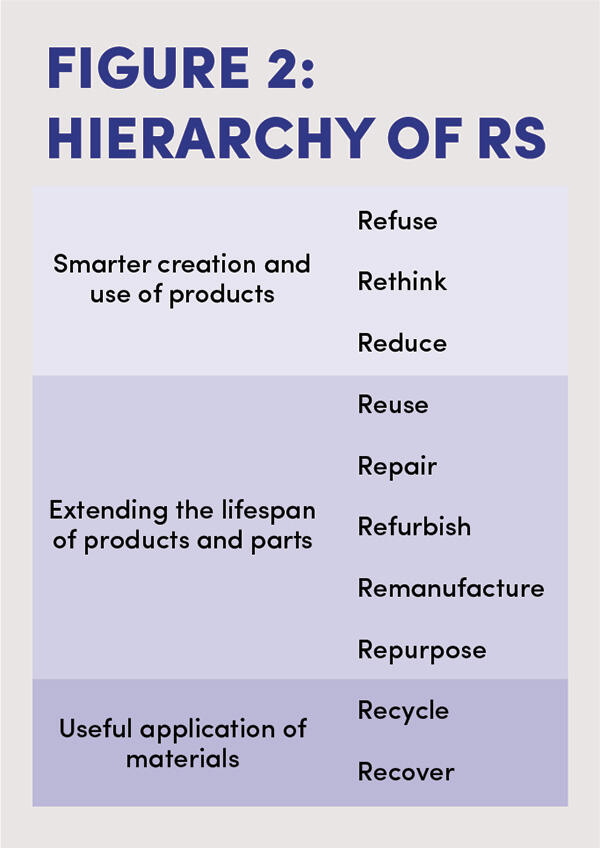

To guide this shift, the ‘Hierarchy of Rs’ (see Figure 2: Hierarchy of Rs) helps businesses and policymakers to prioritise strategies – from refusing unnecessary production altogether to recycling and recovery as last resorts (see tinyurl.com/4u7r9hyj).

Not all forms of circularity are equal: the earlier the intervention (e.g. refusing or rethinking), the greater the environmental and economic benefits.

However, existing tax systems often do the opposite by placing the greatest burden on the very practices that should be promoted – such as labour-intensive repair or Product-as-a-Service models – while continuing to favour virgin material use through lower taxation. This contradiction highlights the urgent need to align fiscal tools with circular economy objectives, making it easier – not harder – for businesses to operate in a regenerative way.

Various circular business models exist, and examples include:

- Circular supply: replacing virgin materials with bio-based or recycled inputs;

- Product life extension: extending product lifespan through repair, remanufacturing and refurbishment;

- Sharing: promoting the use of underutilised consumer assets more intensively; e.g. where private owners can share their assets (such as houses and cars) with strangers in exchange for a payment;

- Product-as-a-Service: shifting from product ownership to service provision; and

- Resource recovery: recovering and reintroducing secondary raw materials into the production cycle; e.g. a trade-in programme for old devices.

Manufacturing companies may apply circular economy principles and lifecycle assessment in their whole business, while other firms specialise in a single step of this process, such as supply of circular materials or resource recovery.

However, as the circular economy disrupts traditional linear supply chains, tax systems based on conventional business models struggle to accommodate the complexity of circular flows, creating tax barriers at each stage of the lifecycle. If we want to align our tax system with the circular principles, then almost every field of tax will require significant changes (removing existing barriers and creating strong incentives that are aligned with other policy mechanisms).

Tax implications: barriers and challenges

Current tax systems have significant implications at almost every step of the lifecycle of a circular product or a service. In this section, we will look into different types of direct and indirect taxes.

VAT

VAT is a clear example of how the current tax system was built for a linear economy and often works against circular business models. Companies trying to recover and reuse products after their first lifecycle can face serious barriers; for example, used products are often classified as waste, meaning that businesses have to pay a waste tax even when the materials are meant for reuse. When those same products are refurbished and sold again, a full VAT rate typically applies, despite the fact that much of their value comes from components that have already been taxed.

The picture isn’t much better for repair services. Some countries apply reduced VAT to repairs to encourage longer product lifespans but these rules vary widely, creating challenges for companies operating internationally. Food donations are also penalised in many jurisdictions – giving away surplus food can still trigger VAT obligations, making it more expensive to donate than to throw food away.

Some countries are starting to address this. In Sweden, recent proposals aim to simplify VAT rules by expanding the profit margin taxation for second-hand goods and exempting food donations to approved charities. Such reforms, reflected in the EU’s ‘Greening VAT’ agenda, are key to making circular practices financially viable but remain the exception, not the rule.

Customs taxes

Customs regulations are another area where linear assumptions obstruct circular practices. One persistent challenge is the lack of harmonised definitions across borders, particularly in distinguishing waste from secondary raw materials. This inconsistency often results in second-hand goods and recycled materials being treated as waste, triggering restrictions and tariffs that make circular trade unnecessarily difficult or expensive.

Under current customs rules designed for virgin goods, there are many other issues; for example, refurbished goods are in most cases taxed as new, and determining the country of origin for recycled materials is complex and burdensome.

However, some international momentum may help to reshape these outdated norms. Initiatives such as the WTO’s Trade and Environmental Sustainability Structured Discussions and the Informal Dialogue on Plastics Pollution are beginning to address these structural issues. Moreover, the introduction of carbon border adjustment mechanisms by the EU (and UK) offers a precedent for aligning trade and environmental objectives.

Labour taxes

The EU’s current tax structure is heavily skewed towards labour: more than 50% of all taxes collected in the EU come from labour-related contributions, while less than 5% comes from green or environmental taxes. This imbalance creates a systemic disadvantage for circular economy models, which tend to be labour-intensive by design.

Repairing, refurbishing, disassembling and remanufacturing products all require skilled hands-on work, yet employers must pay high payroll taxes and social security contributions for each new hire. For circular businesses, this means that doing the right thing environmentally often comes with a financial penalty.

In addition to these structural inefficiencies, circular companies face practical challenges. Many need to invest in upskilling staff but they receive limited incentives to cover training costs. Labour tax incentives are rarely aligned with sustainability goals. While some countries offer generous tax write-offs for machinery or automation, there are few comparable benefits for businesses that rely on human expertise.

This misalignment is especially problematic in the context of an ageing European workforce. As labour supply shrinks and demand for meaningful jobs increases, tax systems should encourage job creation in sectors like repair and reuse, not penalise it.

Green and resource taxes

Despite the growing environmental and economic case for taxing resource use and pollution, green taxes make up less than 5% of total tax revenues in the EU. At the same time, harmful subsidies for fossil fuels and primary resource extraction still persist, undermining the polluter-pays principle and distorting competition.

The result is a tax system that sends weak or contradictory price signals. Businesses which are striving for circularity often encounter overlapping taxes (e.g. VAT and waste tax on reused materials), unclear eligibility for environmental exemptions, and uneven enforcement. Rather than rewarding resource efficiency, the system often penalises it through complexity and inconsistent application.

Circular practices – such as using secondary raw materials, repurposing waste heat or designing for longevity – rarely receive direct tax benefits. Environmental charges are often too low to stimulate behavioural change for companies, and the compliance costs are often higher than actual environmental tax costs. Meanwhile, companies that overconsume or pollute still benefit from low effective tax rates or indirect subsidies.

In light of demographic and economic shifts, including an ageing workforce and shrinking labour base, there is an urgent need to shift taxation toward what we want less of: pollution and virgin resource use. Resource taxes can help to rebalance the system, expanding the tax base while incentivising more circular business practices.

Transfer pricing: valuation complexities in circular models

Circular business models introduce significant complications for transfer pricing rules, which were designed for conventional, linear value chains. One major challenge lies in valuing remanufactured or reused goods – often there are no directly comparable market transactions against which to set an arm’s length price. Similarly, many circular enterprises rely on proprietary or decentralised technology, making the valuation of intellectual property particularly difficult in cross-border contexts.

The complexity deepens with Product-as-a-Service models, where ongoing access replaces one-off sales. In these cases, allocating profits across jurisdictions and determining where value is created becomes difficult, especially when services span several countries. These new models challenge existing norms and demand clearer, more flexible guidance.

Conclusion: building a tax system for circularity

The circular economy offers not only an ecological imperative but also a profound economic opportunity – one that can drive innovation, resilience and long-term value creation. However, for its potential to be fully realised, tax systems must evolve beyond their linear foundations. As this article shows, fiscal policies currently create structural disincentives for circular practices, from penalising repair and reuse to undervaluing environmental benefits.

It is important to clarify that this article does not serve as a policy recommendation. Rather, it aims to set the foundation for understanding the complex relationship between tax systems and circular business models. The insights presented are based on discussions and workshops with numerous multinational enterprises operating in Europe, many of which are actively trying to implement circular strategies but continue to face significant tax-related obstacles.

This ongoing dialogue with industry underscores the urgency of mapping out tax barriers comprehensively across different jurisdictions and lifecycle stages. Only by identifying these friction points can we begin to ask the right questions. What would a tax system look like that truly supports circularity? Which incentives are most effective and fair? How can we align fiscal tools with broader environmental and social goals?

Reforming taxation to support circular economy principles is not just about removing hurdles; it’s about reshaping the rules to reward resource stewardship over depletion. This will require collaboration across governments, businesses and civil society, as well as a willingness to rethink what we value and how we measure progress.

If we are serious about sustainable development, then tax reform must become a cornerstone of circular economy strategies – not an afterthought. The future of taxation is not just about raising revenue; it is about designing systems that enable sustainable, regenerative and inclusive economic growth.

The views and opinions expressed in this article are solely those of the author and do not reflect the views of their her employer.

© Getty images