Wimbledon tax traps: corporate entertaining

Share this article

Hospitality events can carry significant tax costs. Understanding the different treatment of client and staff entertaining helps businesses avoid unexpected liabilities.

Key Points

What is the issue?

The tax treatment of corporate hospitality events varies depending on whether clients, staff or a combination of both attend.

What does it mean to me?

Businesses need to distinguish between client, staff and mixed-attendance events, understand exemptions, and ensure any employment and corporate tax liabilities are dealt with correctly.

What can I take away?

Keep clear records of attendees, costs and business purpose, as poor record-keeping can lead to HMRC challenges, penalties and incorrect tax treatment.

Wimbledon season is almost upon us: the sun is shining, the grounds crew are maintaining the impeccably mowed lawns and the iconic strawberries are ripening, ready for consumption in their thousands. For many businesses, hosting clients and staff at this quintessential British event is the epitome of summer indulgence. However, with HMRC paying close attention to sporting event hospitality, businesses need to take care to avoid turning a day at the tennis into a tax headache.

In this article, we have assumed that entertaining is not the company’s trade, the entertainment is provided as a perk, and the business is VAT registered.

High level overview

Wimbledon hospitality costs for client entertaining generally receive no corporation tax relief, making such events tax inefficient. This article clarifies the distinction between client and staff entertaining and highlights common pitfalls.

- Staff-only entertainment events where the total cost does not exceed £150 per head (including VAT) may qualify for corporation tax deductions and income tax exemptions under the annual function exemption.

- Mixed client and staff events require careful cost allocation.

- The mix of staff and client attendees determines the corporation tax, VAT and employment tax treatment and therefore impacts the overall cost.

- Companies must maintain clear records and identify expenditure relating to clients, employees and private purposes. Poor record-keeping can lead to penalties and incorrect tax treatment.

Determining the correct tax treatment

A common misconception is that because client entertaining has an obvious commercial purpose, it should be tax deductible. However, UK tax legislation includes specific restrictions on relief for business entertaining.

The default position for client hospitality costs is that corporation tax relief is denied for the entire client-related expenditure under Corporation Tax Act 2009 s 1298. In addition, input VAT attributable to business entertaining of non-employees is generally irrecoverable. This includes all associated costs of provision, such as the costs of tickets (including debenture tickets), hospitality packages, food and drink, and related travel and accommodation. The restriction applies regardless of the commercial justification for the expenditure, including generating new business or maintaining existing client relationships.

In practice, however, Wimbledon events are rarely pure client entertainment. Employees will attend alongside clients in most cases, meaning the tax treatment of hospitality expenditure depends on the nature and purpose of the event as a whole.

The key question is whether the event is principally intended to entertain existing or prospective clients, or whether it is staff entertainment provided in connection with employment. Where the primary purpose is client entertainment, the attendance of employees in a hosting capacity does not alter the corporation tax position. The expenditure remains business entertainment and is not deductible in computing taxable profits. This treatment generally extends to employee travel and subsistence costs incurred in facilitating the entertaining.

The employment tax position is more favourable. Where employees attend solely to host clients, or where entertaining clients forms part of their duties, no income tax or NICs liability will generally arise in respect of the hospitality itself. Any associated travel and subsistence costs will need to satisfy the normal employment income rules, including the relevant workplace requirements where applicable.

By contrast, where hospitality is provided to employees as staff entertaining, the costs will ordinarily be deductible for corporation tax purposes and input VAT may be recoverable. Attention then must turn to the employment tax treatment, specifically whether a benefit in kind arises or a statutory exemption applies, such as the annual function exemption or the trivial benefits regime.

We have not considered the trivial benefits exemption in detail because, with a limit of £50 per person, it is unlikely to be relevant in the context of Wimbledon hospitality. However, it may be relevant for smaller events. For example, a staff-only day at Wimbledon could theoretically qualify for the annual function exemption under the Income Tax (Earnings and Pensions) Act (ITEPA) 2003 s 264 where the event is open to all employees, forms part of an annual programme of events and the total cost does not exceed £150 per head, including VAT. If the exemption applies, no income tax or NIC reporting obligation arises, making the event a relatively efficient employee benefit.

When the £150 limit was set more than 20 years ago, a hospitality day at Wimbledon may have cost less than £150 per person. Today, even with careful budgeting, remaining within the limit is likely to be challenging.

Where the annual function exemption is not available, the whole cost of attendance gives rise to a taxable benefit. Where family members attend, the cost attributable to those individuals is treated as incurred for the employee’s benefit, thereby increasing the value of the benefit in kind. In practice, many employers settle the resulting liabilities through a PAYE Settlement Agreement (PSA), ensuring that employees do not personally pay the tax and NIC liabilities.

Mixed-attendance events require careful analysis. Where both employees and clients attend, and the employees are not primarily attending as hosts, an allocation exercise is required. From an employment tax perspective, the portion relating to employees may be taxable and subject to NICs, while the client element does not need to be reported. From a corporation tax perspective, expenditure attributable to employees may be deductible, whereas expenditure relating to client entertainment must be disallowed.

Blurring of costs in OMBs

For founder-led and owner-managed businesses, the distinction between personal and company expenditure can become blurred, particularly during the early stages of trading when owners are investing significant time and resources into the business.

In these circumstances, there is a greater risk that expenditure with both a private and business element is treated as though it were wholly incurred for trading purposes. For example, where an owner attends Wimbledon with family members or other personal guests, it may not always be clear whether the associated costs have been incurred for business purposes, private purposes or a combination of both. Care is therefore needed to ensure that expenditure is analysed correctly and treated appropriately for tax purposes.

As Beckwith v HMRC [2012] UKFTT 181 (TC) demonstrates, where business expenditure is made from a personal account, HMRC may seek access to the taxpayer’s personal bank statements during an enquiry. The position becomes even more difficult where there is both a business and a personal relationship with the individual concerned. The fact that a family member occasionally assists the business does not automatically mean related expenditure has been incurred wholly and exclusively for the purposes of the trade.

Businesses should therefore maintain a clear separation between personal and company spending, and retain evidence supporting the treatment adopted. Failure to do so may result in personal expenses being incorrectly deducted for corporation tax purposes, creating exposure to additional corporation tax, employment tax, interest and penalties.

HMRC’s recent consultation, ‘Company payments to participators’, highlights its focus on transactions between close companies and their owners, particularly where the distinction between company and personal finances becomes blurred.

The issue is not limited to tax compliance. As a business grows, poorly defined boundaries between private and commercial expenditure may also distort reported profitability and complicate investment, sale and due diligence processes. Ultimately, weak controls can undermine confidence in the business’s financial position and wider governance.

Record-keeping essentials

Even where no corporation tax deduction is available and no taxable benefit arises, HMRC will expect businesses to retain evidence supporting the treatment adopted. In practice, this means keeping records of the costs incurred, attendees and their status (for example, clients or employees), the business purpose of the event where relevant, and the date and location. This is particularly important where any part of the expenditure is deductible or gives rise to a benefit in kind.

Records should be kept for six years from the end of the relevant accounting period for corporation tax purposes, six full years for NIC purposes and at least the previous four tax years for income tax purposes.

Finance Act 2008 Sch 36 gives HMRC extensive powers to request information and documents and, in certain circumstances, to inspect business premises and records. The consequences of poor record-keeping can be significant. Failure to comply with an information notice can result in an initial penalty of £300, with further penalties for continued non-compliance. Where non-compliance persists for more than 30 days in serious cases, HMRC may seek tribunal approval to impose increased daily penalties of up to £1,000 per day. Providing inaccurate information in response to an information notice can also attract penalties of up to £3,000. Good record-keeping is therefore essential.

With mandatory payrolling of benefits approaching, proper record keeping of costs will become increasingly important. The tax and NIC will need to be identified and reported as part of Real Time Information (RTI) submissions, rather than being addressed solely through a year-end review.

Inevitable tax consequences

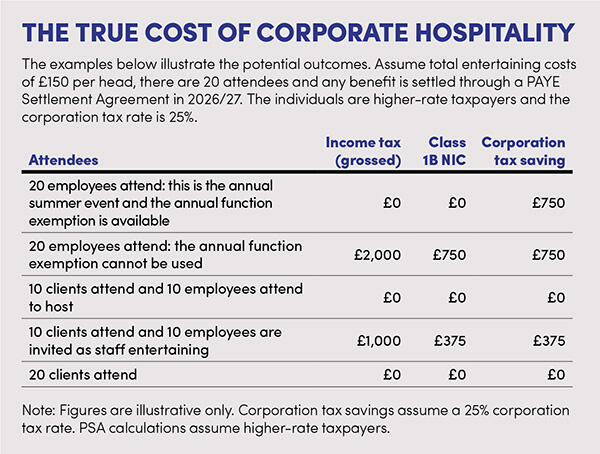

So, can taking clients or prospective clients to Wimbledon ever be tax free? In short, the answer is no. The restrictions on tax relief for business entertaining were introduced because legislators considered such expenditure to be extravagant and inherently non-deductible, notwithstanding its business purpose. As a result, client hospitality continues to carry a significant cost. See The true cost of corporate hospitality.

As the table demonstrates, the identity of the attendees can have a significant impact on the overall tax cost. Businesses must therefore weigh the relative commercial benefits of each approach against the tax consequences.

Hosting clients may strengthen relationships and support revenue generation, but it comes with a higher effective cost given the absence of corporation tax relief on entertaining. By contrast, staff-only events can improve morale, retention and team cohesion, and may be structured more tax efficiently where the annual function exemption applies. So, the next time you’re treating guests to strawberries and champagne at Wimbledon, remember that it is not only the ticket price that matters. The tax treatment can turn a generous gesture into a surprisingly expensive tax proposition.

© Getty images