Clad safely

Share this article

David Rees considers how the tragedy at Grenfell House may affect the tax treatment of replacement cladding on residential buildings

Key Points

What is the issue?

Cladding systems are a standard building solution utilised across most sectors of the economy. The tragedy at Grenfell House will be a catalyst to regulatory change, and retrofit improvements may be required to existing buildings.

What does it mean to me?

The replacement of cladding has gained in importance as the first generation of these buildings have needed to be updated. In many cases replacing cladding has typically formed part of a complete refurbishment, and so the cost has become part of the new capital expenditure incurred and not been tax-relieved.

What can I take away?

Replacement cladding can be treated as a revenue deduction provided it performs the same function as its predecessor and is being claimed by an established owner or occupier. If in due course, the renewal of an existing cladding system becomes necessary via a change in regulation rendering it non-compliant (e.g. poor fire resistance), then this should also be allowable as a revenue deduction.

The Grenfell Tower tragedy was an unexpected wake-up call for everyone associated in some capacity with the property industry. We have grown up in a highly-regulated country and it has been a given assumption that our system of building control was at least as good as, if not better than, those of most other developed countries. It has therefore come as an unpleasant surprise to find that the UK might have in some way failed to maintain adequate diligence in this area, particularly where it relates to an obvious need for the safety and security of residents in their homes.

Plainly, what can now be anticipated is change. It may be some time before we learn how this will present itself, but a review of Building Regulations is expected. While this will change the approach to new buildings or major refurbishments, the treatment of the existing building stock will be significant if regulatory changes are introduced requiring costly retrofit changes. This is likely to focus first on the external cladding, and secondly, the internal fire resistance requirements and safety systems.

It is worth commenting that even if there were to be no compulsory requirement to upgrade existing buildings, those structures which have any identifiable shortcomings, could face other problems. The most obvious being difficulty in letting, with potential tenants deterred either by the perceived risk (which presumably will have to be declared by a landlord), or by the possibility of works having to be carried out during their tenancy. Other areas of concern might be insurance premiums and investment value, which may both be casualties of such uncertainty.

Cladding systems are a standard building solution utilised across most sectors of the economy. Probably only individual residential houses avoid this type of construction, as our enduring love affair with traditional brick and tile, or slate, is unlikely to end in the foreseeable future. External cladding systems are largely a post-World War II introduction which during years of austerity utilised mass-production of components to reduce cost. Early examples of the concept are now generally considered unlikely to become treasured examples of our architectural heritage. Many buildings from the 1960s and 70s went from being new to somewhat dated, bypassing any period of comfortable maturity. This aesthetic decline, compounded with low performance standards which made them difficult to heat or cool, meant obsolescence loomed sooner than architects might have anticipated.

Since their inception, however, the technical quality and appearance of cladding solutions has much improved, and by the 1990s were supplanting bricks & mortar construction for even comparatively smaller buildings such as doctors’ surgeries and motor dealerships. A key attraction has been that where the building has a steel or concrete frame, then the cladding is an outer shell which provides weatherproofing, but is also an aesthetic finish which can relatively easily be renewed in the future to extend the life of the asset.

From the tax perspective, the replacement of cladding has gradually gained in importance as the first generation of these buildings have reached an age where updating becomes desirable. In many cases replacing cladding has typically formed part of a complete refurbishment, and so the cost has become part of the new capital expenditure incurred and not been tax-relieved. Before their demise in 2010 Industrial or Hotel Buildings Allowances could have been available in those specific sectors to mitigate expenditure on the external shell, but their removal has meant there is no direct depreciation allowances on exterior elements.

With respect to the treatment of repairs, in the 20 years prior to HMRC’S 2013 update of its guidance, claims by taxpayers had gradually become more contentious, with the Revenue maintaining a stance that replacements should be like-for-like. In other words a steel-framed single-glazed window could only be replaced with a similar frame.

Double-glazing became a focus issue because HMRC argued that it was an improvement and should therefore be capitalised – accordingly meaning no tax relief. Nevertheless, the growing focus on carbon reduction meant that in 2008 Capital Allowances were introduced to include the addition of insulation to an existing building. For double-glazing this immediately meant that it could be included in a Capital Allowances analysis of an improvement package. It was, however, something of a halfway house for cladding and meant where a system was replaced, and the new panelling was pre-insulated, then a proportion of the cost might be claimable. Additional insulation to existing building could (and still can) be written down at the same rate as the Special Rate Pool (Integral Features). The timing of the introduction of this new category of allowances coincided with the impact of the economic downturn in 2009 and thus ensured that subsequently hardly any claims have been made on this basis.

In the meantime, two other factors were eroding the Revenue’s position on like-for-like repairs. Firstly, changing standards in Building Regulations were raising performance criteria and meant that where a submission to Building Control was required, it might simply not be permissible to install a like-for-like replacement. Secondly, advances in material technologies and construction methods meant that the original installed item was no longer available and a modern equivalent would have to be used.

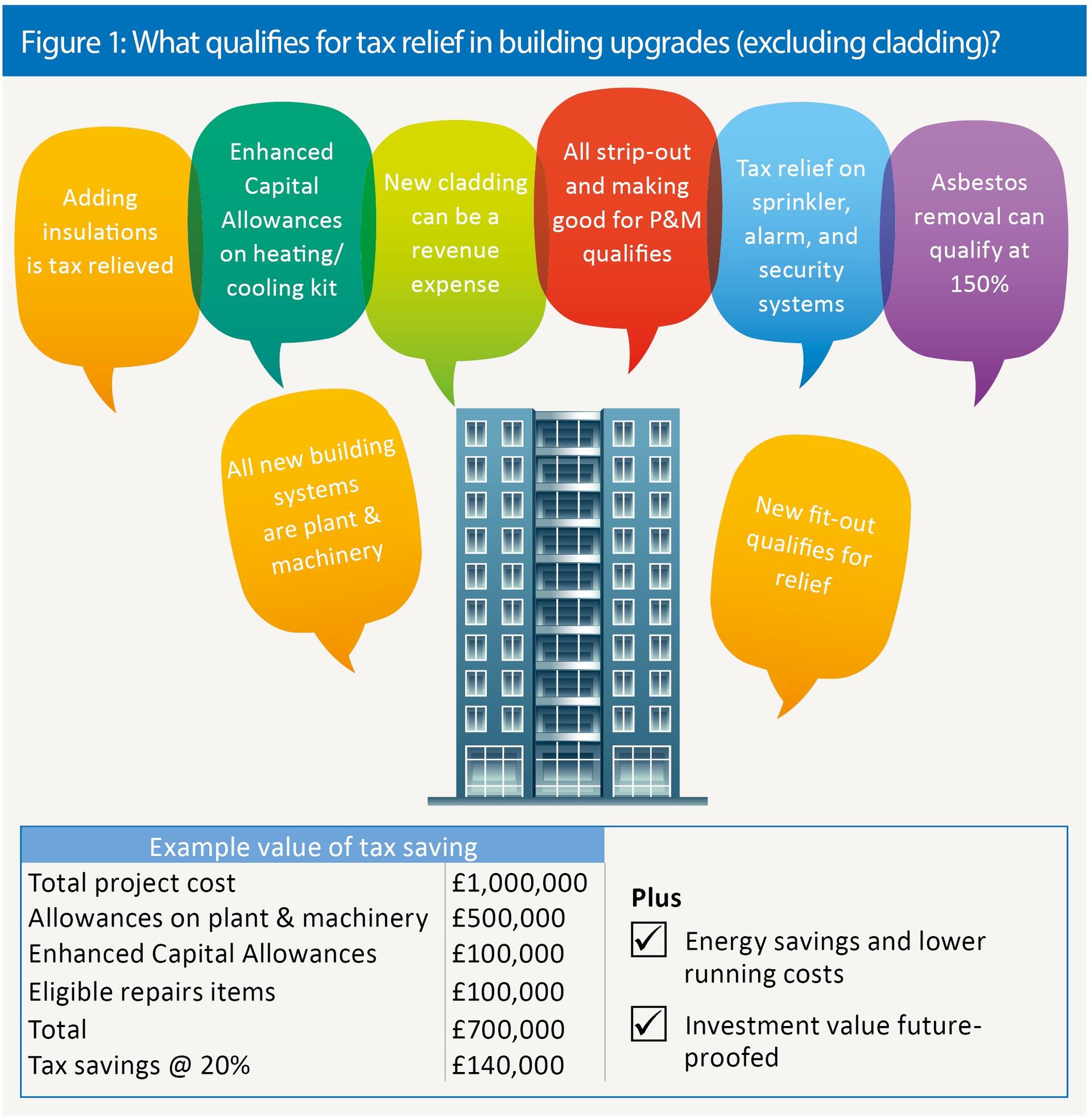

Ultimately HMRC published new guidance on repair in 2013 and the test applied now is functionality. If the replacement item fulfils the exact function of its predecessor, then it can be treated as a repair or renewal qualifying as a revenue deduction. The most minor change is, however, counted as an improvement requiring the cost to be capitalised. There is an inevitable desire by users to make changes in any renovation to optimise a building and this can easily become problematic, requiring a very detailed apportionment of the cost between items qualifying as revenue deductions and the other non-qualifying items. In some instances there may still be another avenue available – which for internal fit-out is the possibility of qualifying for Capital Allowances as Fixed Plant & Machinery. To see what qualifies for tax relief in building upgrades, see figure 1.

To return to replacement cladding, this can accordingly now be treated as a revenue deduction provided it performs the same function as its predecessor and is being claimed by an established owner or occupier. If in due course, the renewal of an existing cladding system becomes necessary via a change in regulation rendering it non-compliant (e.g. poor fire resistance), then this should also be allowable as a revenue deduction. Having to replace a cladding system will clearly be an unwelcome cost for property owners and investors, but factoring in the bottom-line tax saving to cost projections may be some mitigation.

Plainly there will be various scenarios that may influence the position; such as the responsibilities of tenants who hold full repairing and insuring leases. Here a different set of arguments will apply – potentially whether non-compliant cladding is a pre-existing defect and whether it should be outside a tenant’s liabilities. There would seem to be no definitive answer on this question, either in legislation or in case law and so the particular wording of a lease may be important (Bristows LLP published a very useful article looking at this in some detail in the Estates Gazette). While neither landlord or tenant will be likely to want to meet the renewal cost of a modern functional cladding which becomes non-compliant – there is some communality of interest which may help see a negotiated outcome. A landlord might prefer to see the full repairing and insuring tenant meet the cost, but will also have an eye to the future investment value of the asset and so will probably want to influence final specification or aesthetic choices for the replacement. The chances are that a compromise will be needed which could divide the cost.

There is an important distinction when an existing property is newly acquired as its condition will dictate the availability of revenue deductions. The HMRC position (see HMRC Manual BIM35450) is that when a building is purchased allowable repairs should be no more than items which would be considered normal maintenance – not major works. Where a complete renovation is planned post-purchase then HMRC’s stance is likely to be that the price paid must have been discounted to reflect the poor condition and the taxpayer has already benefited from that saving to contribute to the cost of works. Accordingly, where a building is purchased in poor order then the fall-back is a Capital Allowances claim on the cladding on the basis of added insulation.

Another potential cost to be anticipated will be requirements for upgraded fire protection systems, in particular sprinkler systems. Such items are unlikely to be contentious in terms of qualification for tax relief, but an important consideration will be s.25 works under the Capital Allowances Act. This allows for all works associated with the renewal of plant items to be added to the claim for allowances. The scope can be considerable with all costs of stripping-out, making-good, and installation costs being admissible. An extreme example is where it is necessary to open up an external wall to enable access for removal of old plant and new installations. In some instances the associated works can be as much as the cost of the plant. A detailed analysis and breakdown of the costs under the heading ‘building works’ will be needed to identify the appropriate amounts.

Lastly, those familiar with the history of Capital Allowances will be aware of the demise of section 29 which was removed from the act in 2008. This related to what were generally known as ‘Fire Officers instructions’ and allowed works carried out under the Fire Precautions Act at the behest of the fire officer, to be added to the taxpayer’s pool of Capital Allowances. The deletion may seem an irony if it is likely that new provisions for works relating to fire safety are introduced in coming years and that these requirements may lead to a reconsideration of the provision of the relief.

In summary. the necessary and unavoidable aftermath of Grenfell Tower will be more cost for building owners or occupiers, either to replace unsatisfactory cladding systems, or if required, to upgrade internal fire safety installations. Nobody will welcome this unexpected cost but equally few will be likely to strongly contest its need. Nevertheless, tax relief may help sweeten the pill and if at all possible, necessary expenditures should be pre-planned in order to maximise tax reliefs and make the best use of available revenue or capital funds.