Clear views

Share this article

Alex Henderson and Natalie Martin consider the range of initiatives introduced to increase transparency

Key Points

What is the issue?

HMRC and other bodies continue to focus on tax transparency and compliance, with a number of new initiatives in this area being introduced.

What does it mean to me?

Initiatives introduced aimed at increasing transparency have been accompanied with increased civil and corporate deterrents in respect of those evading or avoiding tax as well as those enabling others to do so.

What can I take away?

Advisors need to understand the risks when considering any areas of potential ambiguity and consider whether their advice could be considered ‘disqualified advice’ meaning a client could not rely on it for any Reasonable Excuse defence.

Successive UK governments have been clear about their goal of increasing and encouraging tax transparency and this trend for greater transparency is also reflected in the agendas and action plans of the Organisation for Economic Co-operation and Development (OECD), the European Union, and the United Nations.

Initiatives introduced aimed at increasing transparency through Automatic Exchange of Information such as the OECD’s Common Standard on Reporting (CRS), or through the introduction of beneficial ownership registers, have been accompanied with increased civil and corporate deterrents in respect of those evading or avoiding tax as well as those enabling others to do so.

In this article we will examine two recent developments: HMRC’s new beneficial owners of trust register and the Requirement to Correct and Failure to Correct legislation. We will consider what these mean for clients and their advisors and what actions should be taken now.

The Trust Register

In line with its obligations under 4th Money Laundering Directive, the UK government introduced the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (the Regulations) on 26 June 2017. The main impact of the Regulations is the introduction by HMRC of a new trust register (the Register).

The Register, which is operated by HMRC, is to perform two functions, namely providing:

- a register of the beneficial ownership of all ‘relevant taxable trusts’ to meet HMRC’s obligations to collect the information required under the Regulations (regulation 45); and

- the means for trustees to register trusts with HMRC for the purposes of obtaining a Unique Tax Reference Number (‘UTR’) and delivering tax returns.

As a consequence, in May 2017, HMRC withdrew Form 41G, the paper form which trusts previously had to use in order to register themselves with HMRC for tax reporting purposes.

In addition to registering with HMRC, the trustees of ‘relevant trusts’ are also obliged to maintain enhanced records relating to the trust’s beneficial owners and potential beneficiaries which they must share on request from law enforcement authorities and other relevant bodies (regulation 44).

What trusts are within scope?

The term ‘relevant trust’ includes all UK resident express trusts and any non-UK express trust which has UK source income or UK assets. An ‘express’ trust is a trust established deliberately by a settlor as opposed to a statutory, resulting or constructive trust.

This term ‘non-UK express trusts’ may be relevant to a trust with trustees resident anywhere in the world and under any governing law. However, non-UK trusts are only relevant trusts if they have relevant UK tax events. Where UK assets are held by an underlying non-UK holding company, or UK source income arises within such a company, this will not in itself result in the trust being registrable. This will remove a significant number of non-UK trusts out of the scope of the register.

The new rules also apply to foundations and other legal arrangements similar to a trust.

What information needs to be provided on the Trust Register by taxable relevant trusts?

The information required falls into two categories: 1) administrative details; and 2) beneficial ownership details.

- The administrative details required include:

- the full name of the trust;

- the date on which the trust was set up;

- the country where the trust is considered to be resident for tax purposes;

- the place where the trust is administered;

- a contact address for the trustees;

- the full names of any advisers who are being paid to provide legal, financial or tax advice to the trustees in relation to the trust; and

- a statement of accounts for the trust, describing the trust assets and identifying the value of each category of trust assets at the date on which the information is first provided.

It should be noted that the trust’s assets are only reported once, at the value at which the assets were settled into the trust. This means, for example, that if the trust was initially settled with a nominal £100, the register will continue to show the trust as having assets of £100, irrespective of the current market value of the assets.

- Beneficial ownership details

Detailed information is required for each beneficial owner, including their name and address and (for individuals) their date of birth and National Insurance number or UTR (or, for non-residents, their passport number). It is important to note that the information provided must be current and up to date. Thus, if there are changes between now and the relevant registration or updating deadline, the outdated information can be disregarded. For example if beneficiary is removed or added in the interim period, only beneficial class at the date of registration need to be disclosed, and former beneficiaries should not be registered or should be removed.

For the purpose of the Regulations, ‘beneficial owner’, in relation to a trust, means each of the following:

- the settlor;

- the trustees;

- the beneficiaries;

- where the individuals (or some of the individuals) benefiting from the trust have not been determined, the class of persons in whose main interest the trust is set up, or operates;

- any individual who has control over the trust.

‘control’ means a power (whether exercisable alone, jointly with another person or with the consent of another person) under the trust instrument or by law to: (a) dispose of, advance, lend, invest, pay or apply trust property; (b) vary or terminate the trust; (c) add or remove a person as a beneficiary or to or from a class of beneficiaries; (d) appoint or remove trustees or give another individual control over the trust; (e) direct, withhold consent to or veto the exercise of a power

It is important to note that the Regulations refer to ‘the beneficial owners of the trust and any other individual referred to as a potential beneficiary’. A ‘potential beneficiary’ refers to someone named in a letter of wishes or other relevant document written by the settlor who clearly stands to benefit from the trust as a result of the settlor’s express wishes, but would not include a person who is named in a document but is unlikely to benefit.

What are the deadlines?

The relevant deadline will depend on each trust’s particular circumstances (and, in particular, whether it needs to register for self-assessment).

Existing trusts were required to register by 31 January 2018. However, for this year only HMRC have confirmed that no penalties will be charged if the trust registers before 5 March 2018. Going forward, new trusts will need to register by 31 January following the tax year in which the trust first has a relevant UK tax consequence. However, as there is no separate registration process for self-assessment (for those trusts subject to income tax or CGT), new trusts which need to submit a self-assessment return will need to complete their registration by the earlier deadline of 5 October following the end of the tax year. Trusts which needed to submit a self-assessment for 2016-17 originally had a deadline of 5 October but this deadline was extended twice to 5 December 2017 and then 5 January 2018. Updates must be made by 31 January following the tax year in which the relevant tax consequence arises.

Trustees should ensure that they understand their registration and reporting obligations and that they register by the appropriate deadline.

Further developments for beneficial ownership registers

At the International Anti-Corruption Summit held in London in May 2016, the UK announced its intention of creating a new register showing the beneficial owners of overseas companies that own or want to buy property in the UK, and of overseas companies involved in central government contracts. The Government’s proposals were more specifically set out in a call for evidence in April 2017 which show the intention is to align the new overseas companies register requirements with the existing PSC regime. It was recently announced that the register will be introduced and go live by early 2021.

In addition, in 2016 the government launched a consultation on a requirement to register offshore structures for ‘intermediaries arranging complex structures for clients holding money offshore’. The consultation response document was published on 1 December 2017. Since the consultation was undertaken, both the OECD and EU have undertaken work on similar measures. The Government has therefore stated in its response document that it intends to work with international partners on the development of appropriate multi-national rules, taking into account the responses received for this consultation.

The Requirement to Correct and Failure to Correct

At the same time as measures have been introduced to increase transparency, HMRC has been increasing the sanctions for any perceived non-compliance. The introduction of the Requirement to Correct (RTC) legislation is one such example, compelling taxpayers to review their offshore interests and correct any UK tax irregularities by 30 September 2018 or face new severe penalties.

What is the scope of RTC?

The first point to note is that there is no new legal requirement to correct introduced by the Finance Bill (No2) 2017. Rather, Schedule 18 provides that a penalty is payable by a person who has any relevant offshore tax non-compliance to correct at the end of the tax year 2016-17 and fails to correct the tax non-compliance within the period beginning with 6 April 2017 and ending with 30 September 2018.

‘Offshore tax non-compliance’ includes a failure to notify, a failure to file and delivering an incorrect return and the offshore element means tax non-compliance which involves an offshore matter or an offshore transfer.

The tax non-compliance ‘involves an offshore matter’ if the tax due is charged on or by reference to:

- income arising from a source in a territory outside the UK,

- assets situated or held in a territory outside the UK,

- activities carried on wholly or mainly in a territory outside the UK, or

- anything having effect as if it were income, assets or activities of a kind described above

For income tax and capital gains tax purposes an ‘offshore transfer’ is broadly anything which isn’t an offshore matter and the income or proceeds were received in a territory outside of the UK or transferred to a territory outside the UK. There is a similar definition for inheritance tax. It can be seen from the above, that the scope of the RTC and FTC regime is extremely wide and will capture far more than simple errors. Clients and advisors should give consideration to general concepts which underpin a client’s tax position such as their domicile and residence position, as well as more complex issues such as the application of anti-avoidance legislation and relevant defences.

Consequences of a Failure to Correct

The RTC and FTC measures will apply to all tax still assessable by HMRC as at 5 April 2017. HMRC can ‘look back’ twenty years for deliberate behaviour (back to 1997/98), six years for careless behaviour (back to 2011/12) and four years for innocent behaviour (back to 2013/14). To give HMRC more time to process the information due under the CRS, a special statutory extension will allow any tax years still assessable under existing statute as at 5 April 2017 to remain assessable until at least 5 April 2021.

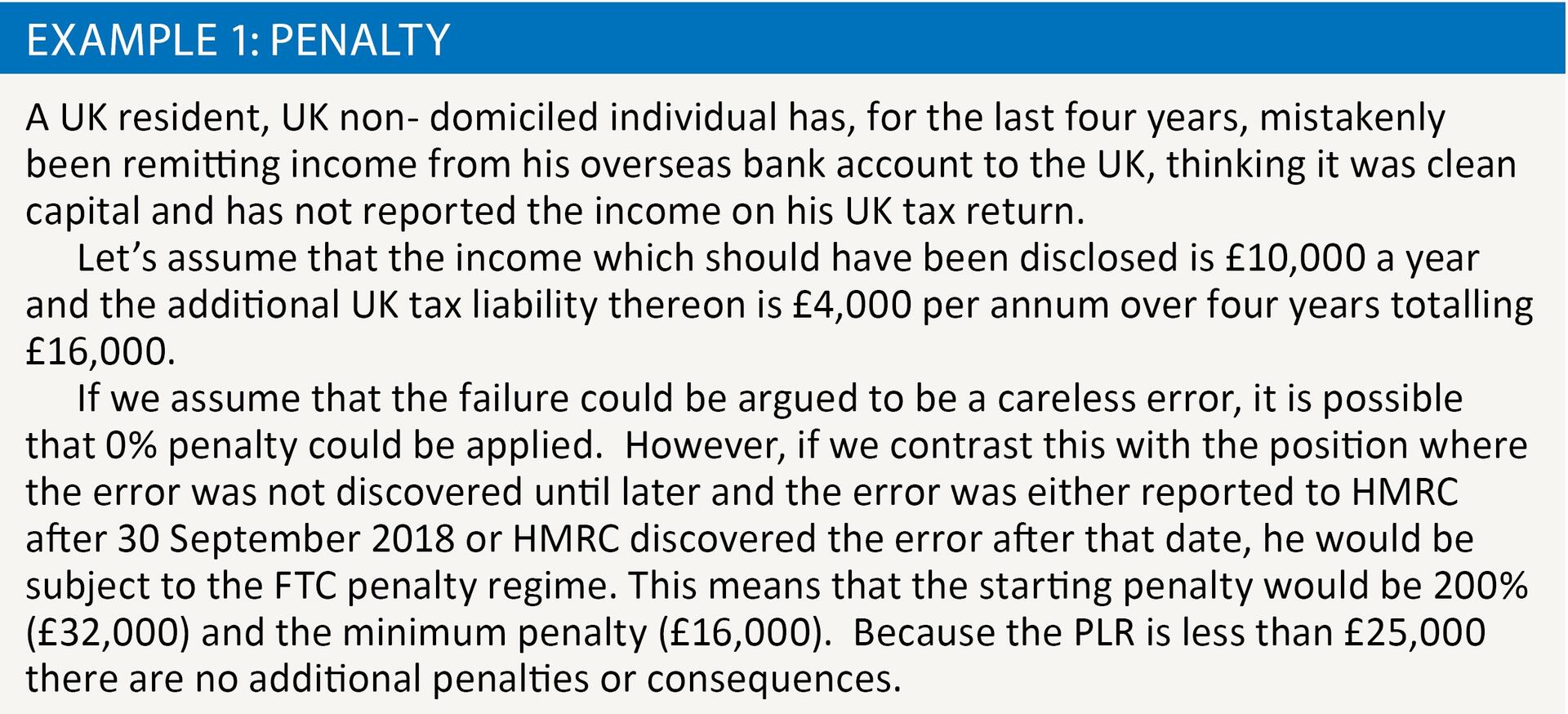

If a failure to correct is identified, the starting position is that the taxpayer will be liable to:

- a penalty of 200 per cent of the potential loss of revenue (PLR). This can be mitigated but not below 100 per cent and any reduction will be based on the timing, nature and extent of the disclosure

- a further asset based penalty of up to 10 per cent of the value of relevant offshore assets may apply where a PLR exceeds £25,000

- an enhanced penalty of 50 per cent of the amount of the standard penalty if HMRC can show that assets or funds had been moved to attempt to avoid the RTC rules.

Naming and shaming can apply where the PLR exceeds £25,000.

It can be seen from the above, that the causal link between the behaviour which caused the original non-compliance and the amount of penalty due is removed. HMRC acknowledged the severity of the FTC regime in their original consultation when they said taxpayers ‘will have committed an original offence, they will have failed to come forward under any previous disclosure facility and will now also have failed to correct under the new legal obligation.’

‘This is a significant failure on the taxpayer’s part and we feel it should therefore attract increased rates of penalty compared with the standard penalties for offshore evasion. This makes it very clear that correcting before the end of the Requirement to Correct window is the best option’.

See example 1.

What if an inaccuracy is discovered during the RTC period?

Given the complexity of the UK tax system it is also not uncommon that mistakes are made within overseas structures. For those who have not paid the right amount of tax historically, making a disclosure to HMRC as soon as the inaccuracy is spotted is key. Options include:

- Digital disclosure service (the Worldwide Disclosure Facility) or any other service provided by HMRC as a means of correcting tax non-compliance.

- Amend an existing tax return or deliver a new tax return.

- Amend in the course of an enquiry into the individual’s tax affairs.

What if there is an area of ambiguity?

There are many areas relevant to UK tax law which may be considered ambiguous or open to interpretation. As an example, a person’s domicile position can best be thought of as a subjective concept due to the mental element which requires a settled intention, or lack thereof as the case may be, to reside permanently or indefinitely in a particular jurisdiction. It is the intention that is the most important element and, unsurprisingly, the most difficult thing to prove.

The difficulty that the RTC and FTC regime presents is that by effectively removing any consideration of causal behaviour when considering the application of penalties, a client who had taken advice and had a supportable filing position relating to a subjective point, may find himself potentially subject to the FTC penalties should that position later be challenged by HMRC and conceded by the client for whatever reason, be it the professional costs or the personal stress of defending the enquiry. Advisers will need to ensure that clients are aware of the risks of the RTC and FTC regime when considering any areas of potential ambiguity.

Reasonable excuse defence

If a failure to correct has occurred, the only way to avoid the FTC penalty is to have a reasonable excuse. The draft legislation provides that ‘where P relied on any other person to do anything that cannot be a reasonable excuse unless P took reasonable care to avoid the failure’. It further provides ‘reliance on advice is to be taken automatically not to be a reasonable excuse if it is disqualified’.

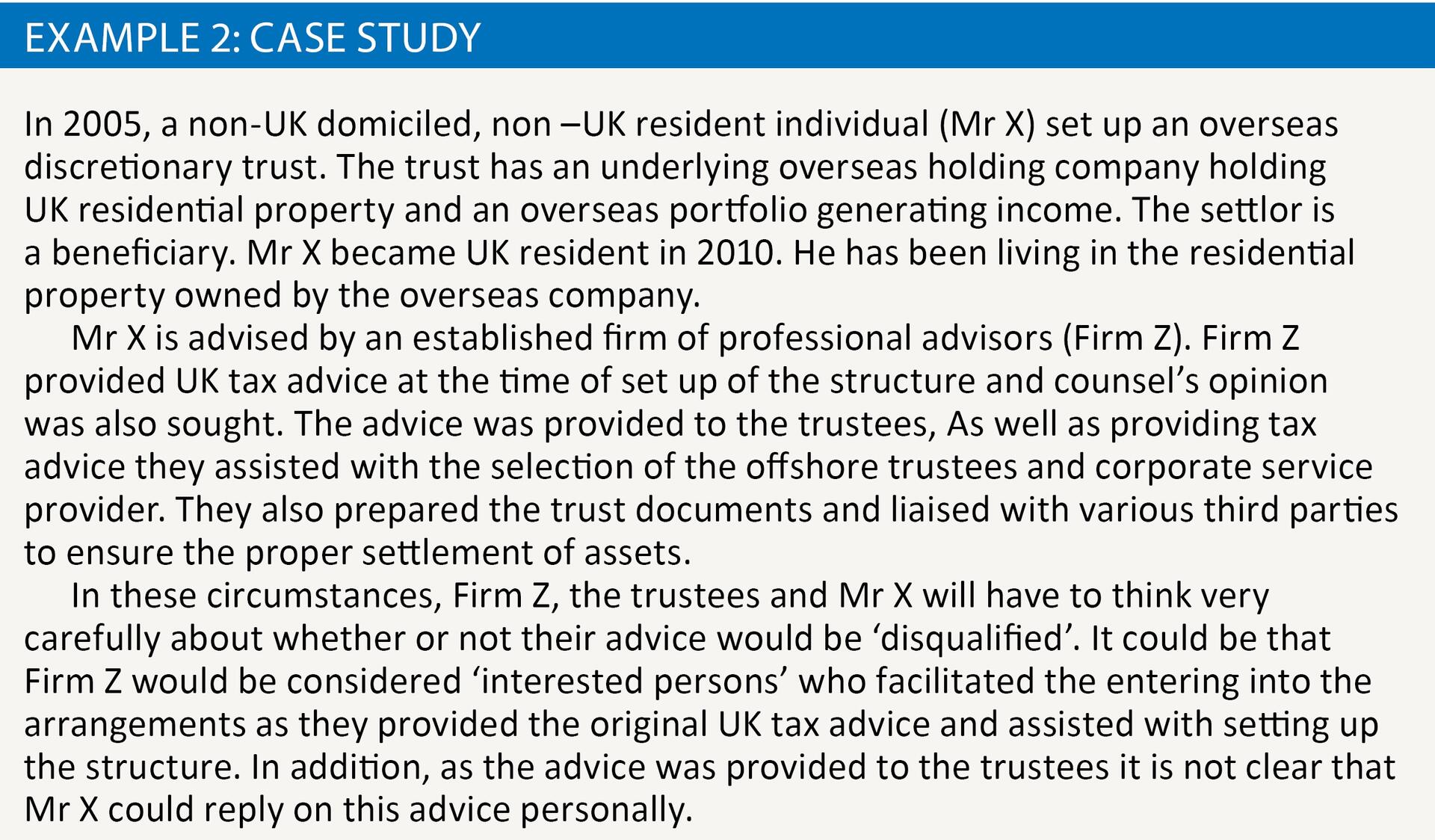

Advice is disqualified if

- the advice was given to P by an interested person,

- the advice was given to P as a result of arrangements made between an interested person and the person who gave the advice,

- the person who gave the advice did not have appropriate expertise for giving the advice,

- the advice failed to take account of all P’s individual circumstances (so far as relevant to the matters to which the advice relates), or

- the advice was addressed to, or was given to, a person other than P.

Broadly for these circumstances ‘an interested person’ means a person who either participated in relevant avoidance arrangements or who for any consideration facilitated the entering into relevant avoidance arrangements and ‘avoidance arrangements’ means arrangements as respects which, in all the circumstances, it would be reasonable to conclude that their main purpose, or one of their main purposes, is the obtaining of a tax advantage. The term ‘facilitated’ is not defined in the legislation.

Although the concept of ‘Disqualified Advice’ has no impact on whether the taxpayer has satisfied their obligation to make a complete and accurate return, the potential impact on penalties will mean that in some situations careful analysis will be needed during the RTC period of the extent to which historic advice may need to be supplemented or extended, possibly involving an additional advisor or tax counsel. It may also be appropriate to consider whether a full factual disclosure should be made to HMRC before the end of the RTC window.

The future of transparency

The complexity of UK tax law and the increasingly tough sanctions for errors, even if entirely innocent in nature, means that it is crucial that clients receive the right advice. Given the wider economic conditions in the UK, the tax transparency agenda and associated revenue powers will continue to evolve and lead to some further changes in HMRC’s approach. Some key actions points to consider are:

- Make clients aware of their compliance and reporting obligations and the relevant deadlines under the various transparency initiatives, including the Trust Register.

- Advise clients with offshore interests to review their affairs to ensure there are no errors or omissions

- Where any errors are discovered, assist the client makes a full and prompt disclosure to HMRC.

- Retain documentation and correspondence, particularly that which shows a potential offshore tax ambiguity was reviewed and addressed appropriately.

- Carefully consider whether any advice provided could be ‘disqualified advice’ and whether this needs to be supplemented or extended.