Clearance services

Share this article

Georgina West provides an overview of the recent Air Berlin case on stamp duty in the context of clearance services and depositaries

Key Points

What is the issue?

The recent Air Berlin decision has had an effect on stamp duty in the context of clearance services and depositaries.

What does it mean to me?

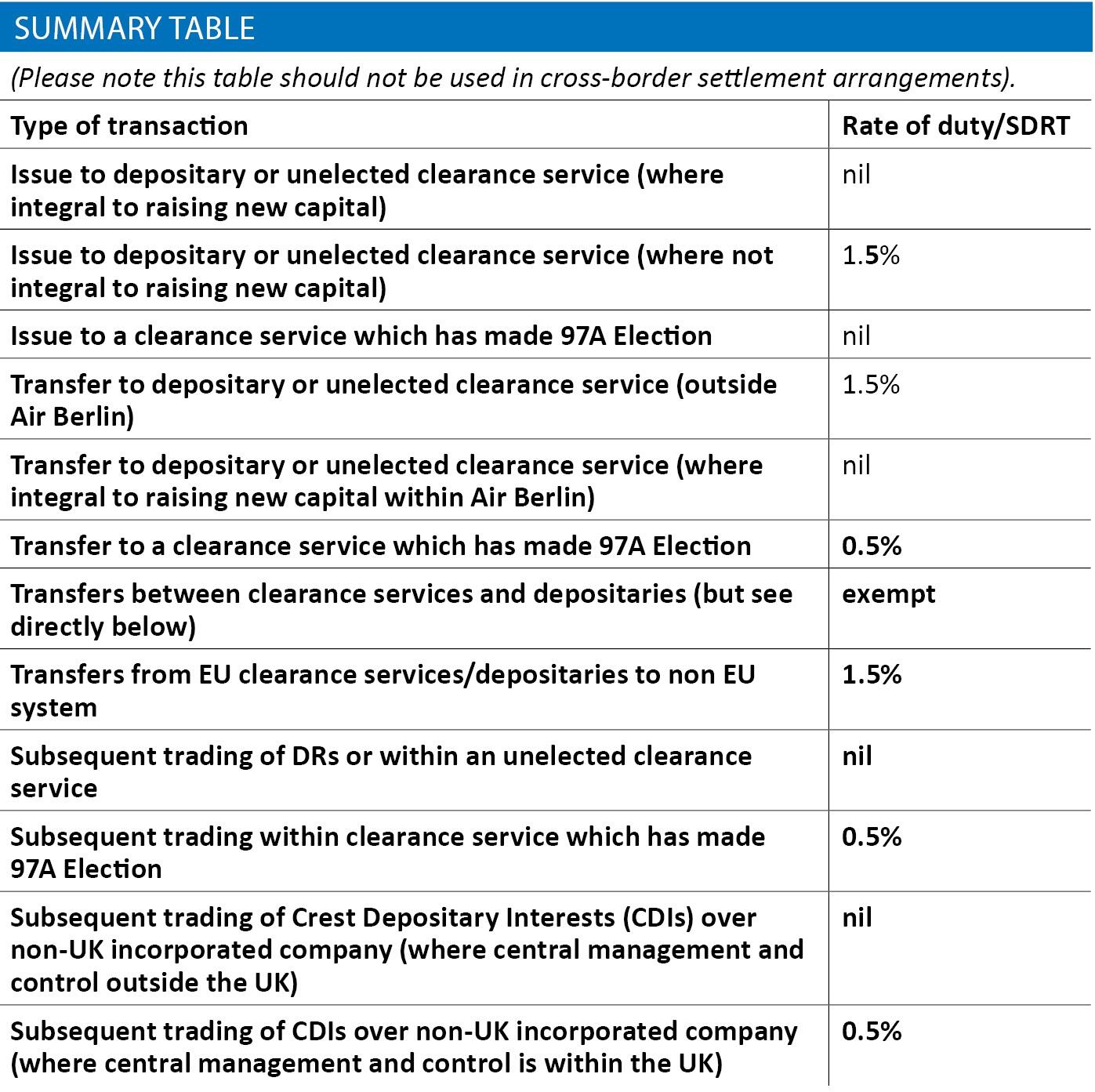

Where shares in UK incorporated companies are being issued or transferred into a clearance service or depository receipt issuer the 1.5% charge to stamp duty and SDRT will apply unless HSBC Vidacos or Air Berlin applies to disapply the 1.5% charge.

What can I take away?

Although Air Berlin now means that certain transfers of shares into a clearance service or depositary will be exempt from the 1.5% charge this is limited to a narrow set of facts.

The basic 1.5% charge

In general terms, clearing is the process of reconciling purchases and sales of financial instruments between a buyer and a purchaser whereby a clearing house (appointed by an exchange) acts as a ‘central counterparty’, matching and guaranteeing the performance of securities ordered and placed by buyers and sellers on an electronic share trading system. The clearing house will usually validate the availability of the appropriate funds, record the transfer, and where appropriate ensure the delivery to the buyer of the securities.

Although the stamp taxes statutes do not define the term clearance service, HMRC Stamp Taxes state in their Stamp Duty on Shares Manual (at STSM052010) that: ‘[A] clearance service is, typically, a system for holding securities and offering a facility to trade and settle those securities within the system by book entry. Once deposited in a clearance service, securities can remain in the system indefinitely and can be traded without a change in the underlying company share register, as the legal title of the underlying securities remains in the name of the clearance service or that of its nominee. Interests in securities can therefore be traded and settled between members of the clearance service without using paper instruments’.

It is, however, typical that the registered title to the securities deposited with the clearance service will in fact be held by a nominee for the clearing house. The Stamp Duty on Shares Manual (at STSM056040) contains a list of clearance service nominees and depositary receipt nominees that are recognised by HMRC Stamp Taxes.

In general terms, a depositary receipt is a negotiable financial instrument usually issued by a bank to represent a company’s securities. It may be necessary to use a depositary receipt where shares in a foreign company are to be listed on an exchange other than that which the company is incorporated under. As depositary receipts are commonly used in the US (over foreign securities) a depositary receipt is frequently referred to as an American Depositary Receipt (‘ADR’). Once the underlying securities are deposited with the depositary, legal title of the underlying securities remains in the name of the depositary or that of its nominee and it is the depositary receipt itself which is traded (e.g. within the clearance service).

Notwithstanding the above, the term depositary receipt is defined in the stamp taxes legislation (at s 69(1), s 94(1) and s 99(7)) as: ‘an instrument acknowledging – (a) that a person holds [Securities] or evidence of the right to receive them, and (b) that another person is entitled to rights, whether expressed as units or otherwise, in or in relation to [Securities] of the same kind, including the right to receive such [Securities] (or evidence of the right to receive them) from the person mentioned in paragraph (a) above), except that for those purposes a depositary receipt for [Securities] does not include an instrument acknowledging rights in or in relation to [Securities] if they are issued or sold under terms providing for payment in instalments and for the issue of the instrument as evidence that an instalment has been paid.’

Broadly, s 67 and s 70 respectively provide for a 1.5% stamp duty charge on an instrument which transfers relevant securities of a UK incorporated company to a depositary receipt issuer (or their nominee or agent) or to a clearance service (or their nominee).

Broadly, s 93 provides for a 1.5% SDRT charge where chargeable securities are transferred or issued to a depositary receipt issuer (or their nominee or agent) towards the eventual satisfaction of the entitlement of the receipt’s holder to receive chargeable securities. Broadly s 96 provides for a 1.5% SDRT charge where chargeable securities are transferred or issued to a person (or their nominee) whose business is or includes the provision of clearance services.

Where both stamp duty and SDRT apply the stamp duty does not cancel the SDRT charge, rather, credit for the stamp duty paid is given against the SDRT charge.

However, once the securities are within the clearance service no further charge to stamp duty or SDRT should arise on transactions wholly within the clearance service (as there is no document of transfer/s 90(4)-(6) exempts the 0.5% SDRT charge). Furthermore, a depositary receipt is not ‘stock’ or a ‘marketable security’ (as defined by SA 1891 s 122), and is excluded from being a chargeable security for SDRT (s 99(6)). As such no stamp duty or SDRT arise on subsequent transfers of the depositary receipt.

Notwithstanding this, it is possible for a clearance service to elect for a different form of treatment under s 97A (a ‘97A Election’). It should be noted that a clearance service may have two segregated parts whereby one part makes a 97A Election whilst the other part remains ‘unelected’. Where a 97A Election has been made (and approved by HMRC Stamp Taxes) the 1.5% charge (for transfers or issues to the clearance service) is disapplied and instead a 0.5% charge is levied on all transfers to, or within, the clearance service operating under the 97A election.

Application of the decisions in HSBC Holdings plc and Vidacos Nominees Ltd v The Commissioners of HMRC C-569/07 (Vidacos) and HSBC and The Bank of New York Mellon Corporation v The Commissioners for HMRC [2012] UKFTT 163 (BNY)

The Vidacos Case concerned the acquisition of a French company (‘French Co’) by HSBC Holdings plc (‘HSBC’). As consideration for selling their shares in French Co the French Co shareholders could elect to receive new shares issued by HSBC. These were to be issued into a French clearance service and listed on the Paris Stock Exchange. A 1.5% SDRT was applied to the issuance of the HSBC shares into the clearance service.

The BNY Case concerned the acquisition by HSBC of a US target company (the ‘US Co’), which was effected by way of a merger whereby the US co would merge with a US subsidiary of HSBC (‘HSBC Sub’) with the HSBC Sub being the surviving entity. The US Co’s shareholders were entitled to receive either HSBC shares or ADRs. A 1.5% charge was applied on the shares issued to the depositary.

In both of these cases it was held (by the Court of Justice of the EU (CJEU) and the First-tier Tribunal respectively) that where shares are issued as an integral part of an overall transaction with regard to the raising of capital the levying of the 1.5% charge was contrary to EU law. In April 2012, HMRC Stamp Taxes confirmed (in their statement entitled ‘SDRT – HSBC Holdings Plc and the Bank of New York Mellon Corporation v HMRC: First-tier Tax Tribunal decision – further announcement’ – see STSM053010) that they will no longer seek to impose the 1.5% charge on issues of UK shares to clearance services or depositaries. The government has also recently announced (in its 2018/19 Budget) that it will not re-introduce this charge once the UK has left the EU.

Application of Air Berlin plc v Commissioners for Her Majesty’s Revenue and Customs (Case C 573/16)

Air Berlin (a UK-incorporated company) undertook an initial public offering on the Frankfurt Stock Exchange whereby it issued a number of new shares into the German clearance service. In order to meet German listing requirements, shares held by the existing shareholders were also required to be transferred into Clearstream Frankfurt (the ‘IPO Transaction’).

Subsequently, Air Berlin issued additional shares to three different shareholders on 10 June 2009. These shares were subsequently transferred into Clearstream on 7 October 2009 (as a requirement for their listing), the ‘Second Transaction’.

Although the 1.5% charge was not charged on the issue of the new shares as part of the IPO Transaction (as the issue of the new shares fell within the remit of HSBC Vidacos) 1.5% stamp duty was collected on the transfer of the existing shares as part of the IPO Transaction and also on the Second Transaction.

In respect of the IPO transaction the CJEU held that, as it was a requirement under German law, for all the shares to be held within the clearance service the transfer of the existing shares was not independent and was merely an incidental transaction which was integral to the process of listing the shares on the exchange. Therefore, it would be contrary to EU law to charge stamp duty or SDRT thereon.

In respect of the Second Transaction, the CJEU held that no stamp tax should have applied as the shares had been newly-issued pursuant to an increase in capital and were transferred to Clearstream solely for the purpose of offering those shares for purchase.

Although HMRC’s current approach to levying stamp tax on transfers of securities into depositaries and clearance services was disputed, this case is confined to a relatively narrow range of fact-patterns. In particular, to transactions that are merely incidental transactions which are integral to the raising of capital. Although, in this case, it was a statutory requirement that all the shares must be put into the clearance service, the CJEU held that the existence of a legal obligation is not a pre-requisite.

Except as otherwise provided all references in this article are to FA 1986.