In the cloud

Share this article

Meenakshi Iyer and Aron Elsey look at the effect of BEPS on online business models

Key Points

What is the issue?

The tax environment has dramatically evolved since the instigation of the OECD BEPS project, with a greater emphasis on tax transparency potentially resulting in more audits by tax authorities seeking to increase their share of the global tax revenues.

What does it mean to me?

As a result of the OECD BEPS project, there is a greater focus on where functions are performed, particularly control of risk functions and the DEMPE functions surrounding IP, and whether the jurisdictions performing these functions and managing the associated risks are being rewarded appropriately.

What can I take away?

In a post-BEPS and post-Brexit world, online businesses, and multinationals with a UK presence, need to be proactive in assessing the impact of these developments on their operations. As a first step, a risk assessment to determine if your current tax profile is appropriate is vital.

The use of technology has become a prerequisite for success in almost every sector of business. In particular, the advance of digital capabilities has meant that companies can now operate online with limited, if any, brick and mortar presence – a game changer within some industries. For example, where once the casinos, betting shops and racecourses were the buzzing hub of the gambling industry, technology has introduced remote access, giving punters the ability to gamble from almost any location, on any event and at any time. The Friday night trek to the video rental shop has been replaced with the click of a button from the comfort of one’s home, as online video streaming sites like Netflix have introduced fierce competition into the industry.

From holiday booking to gambling websites, technology has led to the creation of what has come to be known as the ‘digital economy’; however, the tax legislation that governs these industries still has some way to go in terms of updating the rules to keep up with the speed of change that technology has brought about.

As such, this article looks at the evolving tax landscape in areas that will impact online businesses like these in the months ahead.

Tax and the Digital Economy (OECD BEPS Action 1)

As part of the OECD’s Action Plan to tackle Base Erosion and Profit Shifting (BEPS), it set out to ‘identify the main difficulties that the digital economy poses for the application of existing international tax rules and to develop detailed options to address these difficulties, taking a holistic approach and considering both direct and indirect taxation’ (BEPS Action 1 Final Report, OECD).

In its final report on Action 1, the OECD concluded that there was no need for a separate set of direct tax rules for the digital economy because it is ‘increasingly becoming the economy itself, and therefore it would be difficult, if not impossible, to ring-fence the digital economy from the rest of the economy for tax purposes’. It recognised that the changes proposed in the work on Controlled Foreign Company (CFC) rules (Action 3), addressing artificial avoidance of Permanent Establishment (Action 7) and transfer pricing (Actions 8-10) should substantially address the BEPS issues identified with the digital economy.

However, the report did recommend that indirect taxes move to a ‘consumption tax’ model, i.e., international services, including digital, should be taxed in the place of consumption regardless of the local presence of the supplier. Further, the ‘Low Value Imports Report’ provided options for tax authorities to tax more low value e-commerce goods by shifting the VAT obligation to the vendor/ intermediary.

In direct response to the OECD’s conclusion on Action 1, there has been unilateral action in some countries. India, for example, has introduced a ‘Google tax’ in the form of an equalisation levy of 6% for services such as online advertisement and any provision of digital advertising space.

The UK is yet to take any industry specific action to address taxation of the digital economy. However, the UK government indicated in the Summer Budget 2015 that it will consider a wider review of ‘use and enjoyment’ measures for services such as advertising, potentially impacting the VAT treatment of the UK advertising revenue for a number of online businesses. The consultation paper is expected to be released later this year with potential implementation in 2017. In the Finance Bill 2016, the UK government announced measures to ‘direct a taxable person, whose business is not established in the EU, to appoint a VAT representative’ responsible and liable for VAT payments (Clause 123 – Finance Bill 2016). Additionally, it announced measures to allow HMRC to hold the operator of an online marketplace liable for VAT on goods sold in the UK via the marketplace by an overseas business (Clause 124 – Finance Bill 2016).

These measures and changes to the tax landscape will invariably increase the operating costs for online business operators in the UK.

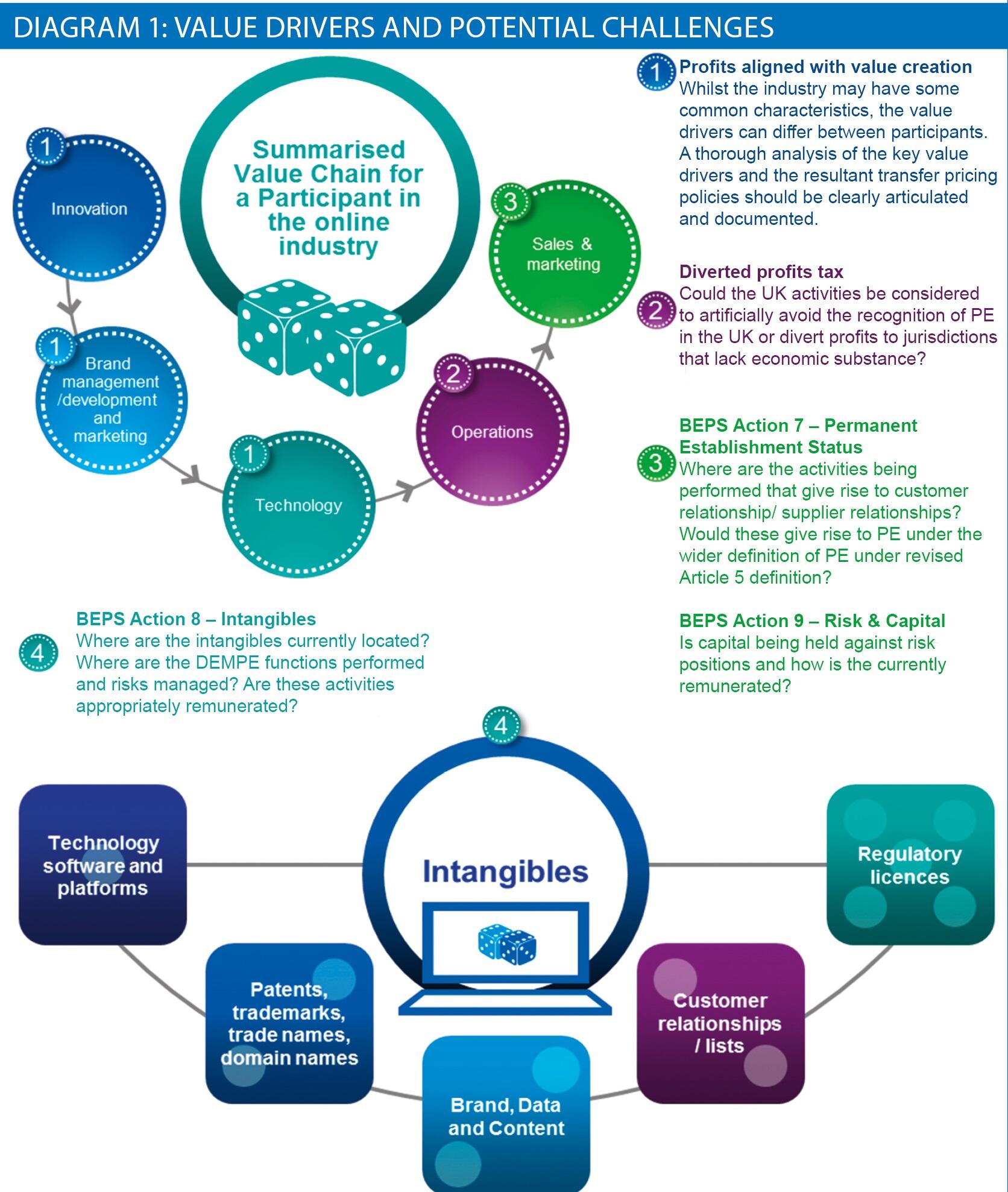

Profits aligned with value creation (OECD BEPS Actions 8-10)

In the Finance Bill 2016, the UK government updated the UK’s transfer pricing rules according to the latest OECD guidelines which incorporate the revisions agreed under BEPS Actions 8-10. This update brings the UK rules in line with the most current, internationally agreed consensus on the practical application of transfer pricing principles. The key objective of Actions 8-10 is for transfer pricing outcomes to be aligned with value creation. In summary, this requires an allocation of profits for tax purposes to be consistent with the economic activity generating that value. The key focus is on the treatment of intellectual property, risk and capital, all of which are likely to be relevant for online businesses.

The increased focus on control of risk and financial capacity to bear risk as detailed in revised Chapter 1 of the OECD Guidelines under BEPS Actions 8-10, means that headquarter services currently being remunerated with a cost plus return may no longer be appropriate.

In order to align profits with value creation, it is necessary to identify the key value drivers of the industry and how they generate profits (or trigger losses) for participants in the industry. Further, it is also important to undertake a detailed review of the group’s value chain to determine how its profits (and/or losses) should be split among the group companies operating in different jurisdictions. This can be done through a detailed value chain analysis.

However, for online businesses, the challenge is to determine the relative contribution of intangible assets such as technology platforms, brand, data and content to the generation of group profits and ensure that the location where the development, enhancement, maintenance, protection and exploitation (DEMPE) and control of risk functions are performed are rewarded appropriately. See diagram 1.

UK Diverted Profits Tax (DPT)–Unilateral action taken by the UK

The UK DPT is a new tax separate from corporation tax that applies at a 25% rate to ‘diverted profits’ arising on or after 1 April 2015. It was introduced to target the issues addressed by BEPS Actions 7-10.

The DPT applies if:

- A UK company is considered to have diverted profits from the UK by involving entities or transactions lacking economic substance (Section 80, DPT Legislation); or

- A non-UK company is considered to have diverted profits from the UK by avoiding a taxable presence (this is directly linked to BEPS Action 7 which introduced changes to the threshold for a Permanent Establishment (PE)) (Section 86, DPT Legislation).

The onus is on the taxpayer to consider whether its provisions and arrangements fall within the scope of DPT, and, where they do, to notify HMRC within three months of the end of the relevant accounting period (six months for accounting periods ending on or before 31 March 2016). Tax-geared penalties can apply for failure to notify within the appropriate timeframe.

The offshore structures adopted by many multinationals with online businesses could potentially be caught by the UK DPT legislation. For example, if a brand is owned in an offshore location and a UK entity pays a brand royalty to the offshore location which lacks economic substance, then this arrangement could be caught by the UK DPT legislation. The impact will be that the brand royalty payment will be disallowed and the UK entity will have to pay tax at 25% on the additional profits that will arise as a result of this denial of deduction.

As such, we expect that a number of companies, and particularly online businesses, may have notification requirements and may be subject to DPT at 25%. HMRC have recently started issuing their first round of DPT notifications and, due to these changes in the rules we expect HMRC to increase their scrutiny of substance.

Impact of Brexit

This article would be incomplete without making reference to the impact of Brexit. The full impact of which will become clearer over time as the form and terms of the exit are negotiated.

UK direct taxation is subject to a number of EU directives, principles and the jurisdiction of the Court of Justice of the European Union. Post-Brexit, EU Directives such as the Parent Subsidiary Directive and the Interest and Royalties Directive may no longer apply. As with any business looking to repatriate income into the UK, this will mean possible withholding tax on dividend payments from EU subsidiaries as well as intra-Europe interest and royalty payments.

For indirect taxes, the impact is likely to depend on whether the online business is involved in the sale of goods (customs duty and excise tax) or the provision of services (primarily VAT). But there is likely to be an adverse impact on cash flows and increased administrative costs for cross-border transactions. Additionally, VAT schemes such as the Tour Operator Margin Scheme (TOMS) which provides exemption from VAT to qualifying European online and offline tour operators may no longer apply.

Both Brexit and BEPS present significant changes to the international tax landscape. The potential impact of Brexit must be juxtaposed with the conclusions of the BEPS Project to accurately assess its impact on online businesses and multinationals in general.

Conclusion

There is a clear direction of travel towards tax transparency which is riding the wave of the OECD BEPS Project. In light of the increased level of tax transparency, online businesses should be prepared to clearly articulate the rationale for any offshore structures in their transfer pricing documentation and CbC report.

Additionally, most online businesses make use of intangible assets such as technology platforms, brand etc. These businesses need to consider whether their current transfer pricing policies result in the right split of profits between the legal owner and the location where the IP related DEMPE and control of risk functions are performed.

Online businesses, and multinationals with a UK presence, need to be proactive in assessing the impact of BEPS and Brexit on their operations, and the knock-on impact on financial metrics such as earnings per share and effective tax rates. A risk assessment to determine if the current tax profile is appropriate in a post-BEPS and post-Brexit world is not an option; it is the necessary minimum. And the time to do that is now.