Company cars: now and the future...

Share this article

David Chandler looks at the practicality of providing employees with a means of transport

Writing for the Tax Voice means we need to focus on the facts and technical issues. However, when providing advice direct to clients we’re often asked also to try and “predict” the future (or at the very least provide an opinion). In some areas that is often easier said than done. Where company cars are concerned, of late this has become markedly more difficult. Which is why I’ve decided to keep a closer eye on my crystal ball.

Company cars seems to have undergone some of the most impactful changes over the last 18 months and in addition there are fairly radical changes coming over the next few years. As professionals advising in this space we have never seen such a period of change.

In an attempt to provide a degree of clarity I thought I would try and summarise some of those changes whilst opining on what the crystal ball shows.

Do people still choose company cars?

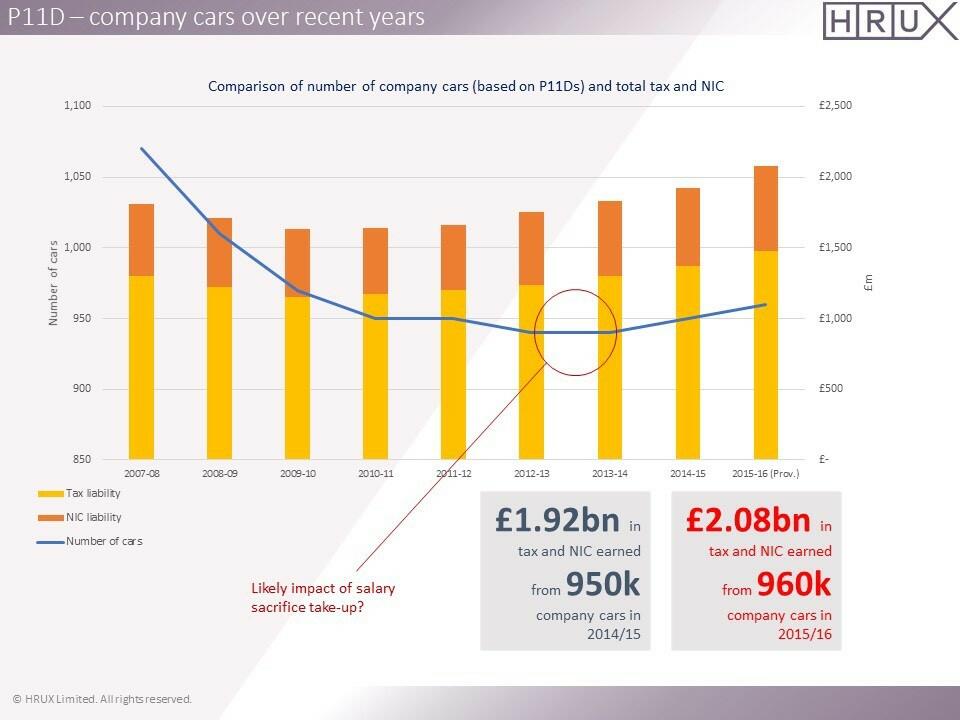

Yes, although the number of company cars has decreased over the last 10 years, there are still somewhere around three-quarters of a million people taking company cars. Graph 1 shows the total tax and NIC “take” on company cars compared to the number of people reported to have one on their P11D. By April 2016, according to HMRC, there were 960 thousand company cars. But many analysists suggest numbers have fallen sharply since.

There are many companies who still offer company cars to employees, especially those who need them to do their jobs, although there are no tax breaks for those with high business mileage so the tax and NIC charge is the same as for employees who receive the car entirely as a “perk” of their jobs.

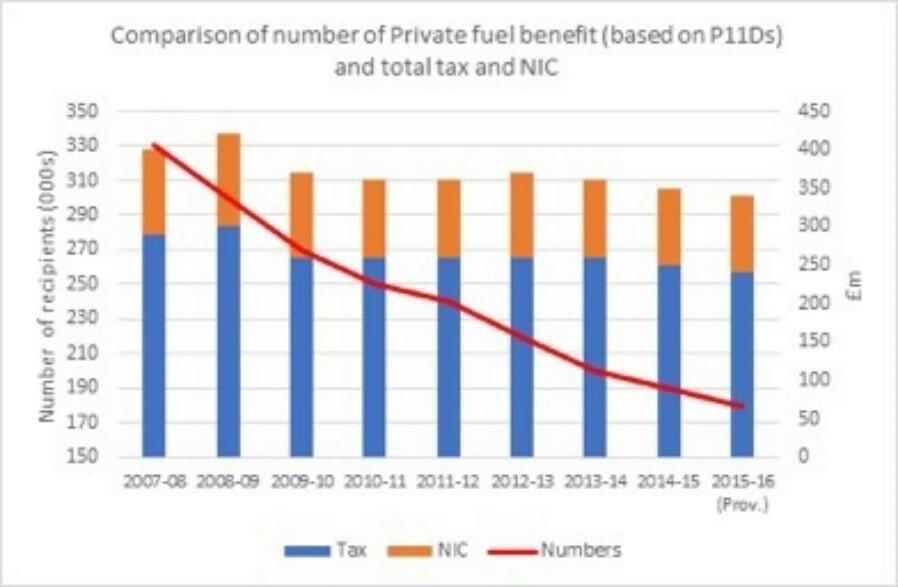

Amazingly, some employees still receive the benefit of free private fuel in a company car. Graph 2 shows how the total number of employees taking the benefit has fallen over 10 years, whilst the total tax and NIC take has remained pretty constant.

What is the latest on the current BiK rates?

Currently we have some of the highest tax charges for company cars we’ve ever seen. For a number of years the government encouraged people to adopt cars with low emission of CO2 and this has worked as a policy.

A typical diesel car with 119 grams of CO2 will have a tax charge of 25% this year (2017/18). Next year this will be 28% and the year after 31% - rates that were previously reserved for the ‘gas guzzlers’. These include the additional 1% tax charge on all diesels (the diesel supplement is now 4%) that was announced during the Autumn budget last year. Over four years you could pay tax on 116% of the List Price – numbers that are quite staggering (during the same period the car will depreciate by only 50-75%, or thereabouts).

Then there are the new rules on real world testing (WLTP) that are expected to come in by 2020 (which still remain a little vague). Initial thoughts are that they will likely push up CO2 ratings although the impact could be mitigated as a lot of cars will by then be taxed at the maximum rate of 37%.

What’s the deal with OpRA?

OpRA has been covered in many articles over the last 18months. It is worth mentioning that where cars and cash allowances are concerned, HMRC are yet to fully address clients’ practical questions. Due to the speed of implementation a number of issues remain a little unclear. Some of these include:

- HMRC clarified that under salary sacrifice you only take account of the finance element of providing a car with CO2 in excess of 75g/km, however what does that mean in practice? Do we include RFL, maintenance, insurance, administration costs just to mention a few (and can leasing companies even provide this data?). The latest guidance is to use a “just and reasonable basis”; one would hope that HMRC won’t reject clients’ computations just because they don’t agree with them given the lack of guidance.

- There is also a similar question on how clients need to look at their cash allowances where employees have a choice between a car and cash, increased administration for minimal tax increase.

- Latest guidance also confirmed that now HMRC are trying to capture car policies that pay AMAPs and variable cash (such as the employee car ownership schemes). Given grandfathering provisions only last 12months for cash schemes, this has left employers and employees in a difficult space – many employees will have started contracts when the rule change was first announced, and these contracts often cannot be broken without expensive charges.

In summary lots of confusion – salary sacrifice, cash allowances, employee car ownership schemes, OpRA, increasing tax BiK rates, new testing regimes... it’s enough to turn companies away from cars (and there’s evidence that’s exactly what’s happening).

Is it all bad news?

In simple terms, no. In just over 2 years, electric cars will attract a 2% BiK tax charge, for the tax year 2018/19 the BiK charge is 13%, then it increases in 2019/20 to 16% before dropping back to 2% from 6 April 2020. That’s a pretty big attraction for electric vehicles.

Hybrids under 50g/km will attract a similarly attractive rate for those with big ranges when on electric power only (2% rate for those vehicles with a range of 130 miles or more).

In no time at all hybrid and electric cars are going to be very attractive as company cars. The government have announced huge investment in electric cars so whatever your view, they are coming: that’s a certainty. The big question for me is will those rates last? With all my years in tax when there is a tax gap the government usually try and plug it, that’s what the crystal ball is saying anyway.

What does this all mean?

Companies need to juggle that difficult act of managing the short-term minefield, whilst having one eye on the future and ensuring a robust and future-proofed policy moving forwards.