The complex structure of VAT: too complicated to reform?

Share this article

While the complex structure of VAT is hard to rationalise, the huge costs of reform would be even more complicated.

The highly respected Institute for Fiscal Studies recently released a document ‘Tax and public finances: the fundamentals’ (see tinyurl.com/jrycjhy4) highlighting ‘10 key facts related to taxes and the public finances that will underlie the fiscal policy challenges and choices faced by citizens and governments in coming decades’. Fact No 5 said: ‘VAT zero rates and exemptions cost £100 billion in forgone revenue. They place a large compliance burden on firms and are a very poorly targeted way to redistribute income to lower-income households.’

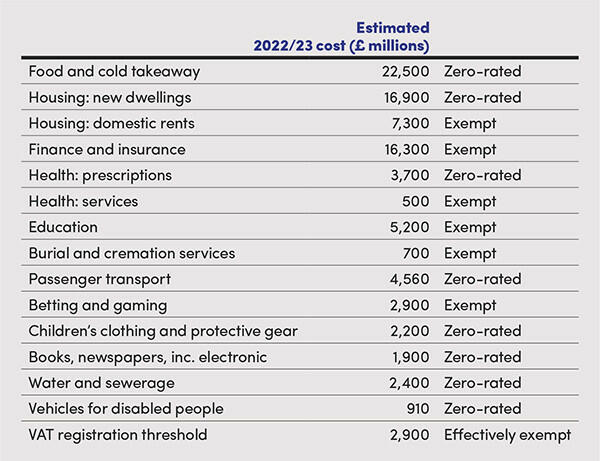

VAT was estimated to contribute £160 billion in 2022/23 to the Exchequer. We now have data from HMRC which costs the main VAT zero rates and exemptions. Zero rates are classified as non-structural reliefs (see tinyurl.com/yeykk9xb), whilst exemptions are classified as structural reliefs (see tinyurl.com/2jezbacs). The reason for the distinction is not obvious! The big difference in practice is that where sales are zero-rated, there is no loss of VAT in the supply chain. By contrast, exempt goods and services typically carry a built-in VAT cost directly borne by the suppliers, no doubt affecting their pricing decisions. The main areas, totalling just under £91 billion in 2022/23, are shown on the right.

In addition, VAT is refunded to a range of public bodies, estimated to amount to just under £23 billion.

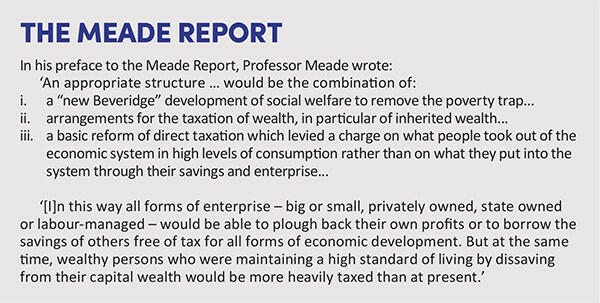

In 1978, the Meade Report ‘The structure and reform of direct taxation’ was published (see tinyurl.com/yychw9yn). It reflected the deliberations of a committee put together by the IFS, chaired by Professor James Meade, and advocated significant expansion of consumption taxes and a corresponding reduction in direct taxes (see The Meade Report).

Despite these urgings, the UK has not changed its general approach. We still raise roughly the same amount (as a percentage of GDP) from consumption taxes, although we have seen the expansion of VAT and a broadly equivalent reduction in specific consumption taxes. In fact, it is taxes on income which have risen, especially national insurance and corporation tax.

A confusing tax

It is easy to see why VAT is not charged in some areas. Most health services in the UK are supplied without charge, so adding VAT onto private health services would introduce a distortion. Both public and private health services do pay VAT on some purchases, which they cannot recover. The same issue arises in education, although the Labour party proposes making private school fees subject to standard-rate VAT.

There is no agreed approach globally to levying VAT on finance and insurance services, mainly because there is no agreement on what the taxable supply is or should be. The financial service sector bears a large amount of input tax which it cannot recover, as the purchases are not related to taxable sales. The EU has debated the issue for decades and not reached any conclusion. In 2021, Deloitte Netherlands produced a paper outlining various options, including doing nothing (see tinyurl.com/3wv49z82).

Housing is another area fraught with difficulty. Rents are exempt, so some VAT is borne by landlords in relation to building repairs and improvements and other administrative costs. Adding VAT to the price of new houses and increasing the cost of rents looks very unlikely. And how would VAT apply to second-owner housing?

Betting and gaming don’t need VAT, as specific tax regimes are designed for the sector. That leaves us with children’s clothing, books, newspapers and magazines, passenger transport, disabled people’s vehicles, burial services and water. It would theoretically be quite easy to add on VAT, as there are no boundaries with other currently standard-rated items. Burial services already bear some VAT, as they are exempt – but everything else is zero-rated, which means that 20% would need to be added to the sales price to preserve supplier margins. There isn’t much complexity here, though.

The complications of food

Food remains the largest item benefiting from zero-rating. However, not everything we eat or drink is zero-rated. Restaurant meals are liable to standard-rated VAT, as is confectionary, chocolate, and chocolate-covered biscuits, fruit and nuts. Hot takeaway food and drinks are liable to VAT, while cold food and drink is zero-rated if takeaway but standard-rated if eaten in the café. We won’t mention pasties, which are only hot if you are lucky enough to catch one fresh from baking the oven...

Food obviously remains the most complicated area on this list, as providers need to work out which side of the boundary the product lies and take account of their customers’ consumption intentions in some cases. There would be a clear logic to having a single VAT rate for everything that is eaten or drunk, no matter its temperature, or the location. But the challenge is made harder by the UK’s relatively high 20% standard VAT rate. Adding 20% to the cost of food would be a major increase for many households. On the other hand, introducing say a new 5% rate would reduce the tax take from currently standard rated items and would bring in only something like £5-6 billion before considering what compensation would be needed for less well-off households.

Household spending

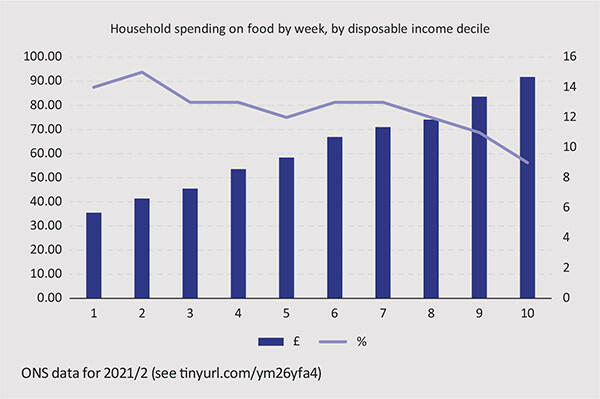

Household spending on food goes up in absolute amounts by income decile but drops as a percentage of household disposal income (see Household spending by week). The wealthiest decile spends more than twice as much on food as the second decile – but it is just 9% of disposable income compared to 15%. Interestingly, there are 1.5 people in the second decile household, but 3.2 people in the top decile – so a 1.5 person household in the top decile would probably spend less than 5% of disposable income on food.

Any decision to start charging VAT on food would need to take into account the burden it would place on households. For some, increasing benefits could give the necessary income to help, but the current benefit system does not reach all low-income individuals, requiring a new design for benefits. Inevitably, some households would fare better than others, with larger households facing greater hardship and single people not obviously fitting into any easy route for support. The poorest fifth of households spent about £330 pw on food in 2021/22 – so a 20% VAT rate would mean those households would need something like £3,500 annually, just to stand still. The richest fifth spent over £800 every week – so would be over £8,000 worse off every year. Where should the cut-off for compensation be?

This remains the challenge for any government. Having a single VAT rate for all food and non-alcoholic drink would be simpler – but the transition would be very hard. The same applies to other areas, especially transport. The impact on inflation would be obvious, as would the challenge in trying not only to compensate less well-off people but demonstrating that the compensation did actually cover extra costs. It’s not surprising that no government has sought to pick up that challenge.

If governments are to start broadening the VAT base, economists need to demonstrate that this would be better for the economy; in other words, that a barrier to growth had been reduced. At the moment, all we have are fine words, when what a government (and the public) needs is clear evidence that there are indeed sunlit uplands worth the very painful transition. Increasing the cost of items that form a much larger part of a poorer household’s budget (food, transport, housing, energy) looks regressive and very bad politics. Meade’s 1970s fears that too many households live off inherited wealth look much less relevant today.