The concept of 'connected persons': what are the ties that bind?

Share this article

The definition of connected persons is complicated, and becoming more so as our social norms evolve. With marriage and civil partnership at the heart of the rules, not all families fall neatly into the legal classifications.

Key Points

What is the issue?

The concept of connected persons appears throughout the direct taxes legislation. This article focuses on how two individuals can be connected by virtue of being part of the same family.

What does it mean for me?

Families and tax law share a reputation for being complicated and so the provisions for connecting family members for tax purposes must be approached with caution.

What can I take away?

The connected parties rules are starting to lose their appropriateness as the nuclear family declines in significance. With marriage and civil partnership at the heart of these rules, a number of family relationships are left outside of their purview.

The concept of connected persons appears throughout the direct taxes legislation. Usually its purpose is to treat connected persons differently to unconnected persons on the basis that they may be able to work together to achieve an outcome that would not be possible in a normal commercial environment.

There are a number of ways that two persons can be connected, particularly in the context of companies and trusts. The focus here is solely on how two individuals can be connected by virtue of being part of the same family (hereafter called a ‘family connection’). Families and tax law share a reputation for being complicated and so the provisions for connecting family members for tax purposes must be approached with caution.

The general definitions of connected persons in the main direct taxing Acts are:

- Taxation of Capital Gains Act (TCGA) 1992 s 286 (the ‘primary definition’)

- Inheritance Tax Act (IHTA) 1984 s 270 (borrowed from the primary definition with a couple of extensions);

- Income Tax Act (ITA) 2007 ss 993 and 994 (the ‘primary definition’ but worded differently); and

- other definitions borrowed from ITA 2007 s 993, (Income Tax (Earnings and Pensions) Act (ITEPA) 2003 s 718, Corporation Tax Act (CTA) 2009 s 843, CTA 2010 s 1122, and Income Tax (Trading and Other Income) Act (ITTOIA) 2005 s 878(5).

These general definitions are, of course, subject to any specific definitions that apply for a particular purpose in the Act.

The primary definition

Under the primary definition of connected persons at TCGA 1992 s 286, an individual ‘A’ is connected with ‘B’ as a member of their family if A is:

1) B’s spouse/civil partner; or

2) B’s relative.

Pausing here, a relative is a sibling, ancestor (parents, grandparents, etc.) or lineal descendent (children, grandchildren, etc.). It is suggested that half-brothers and half-sisters are not siblings for this purpose (in ITTOIA 2005 s 804A(6) they have to be expressly included). Adopted children are lineal descendants of their adoptive parent(s) only under Adoption and Children Act 2002 s 67.

Then the list gets more complicated. The following groups are also connected with B:

3) relatives of B’s spouse/civil partner;

4) the spouses/civil partners of B’s relatives; and

5) the spouses/civil partners of the relatives of B’s spouse/civil partner.

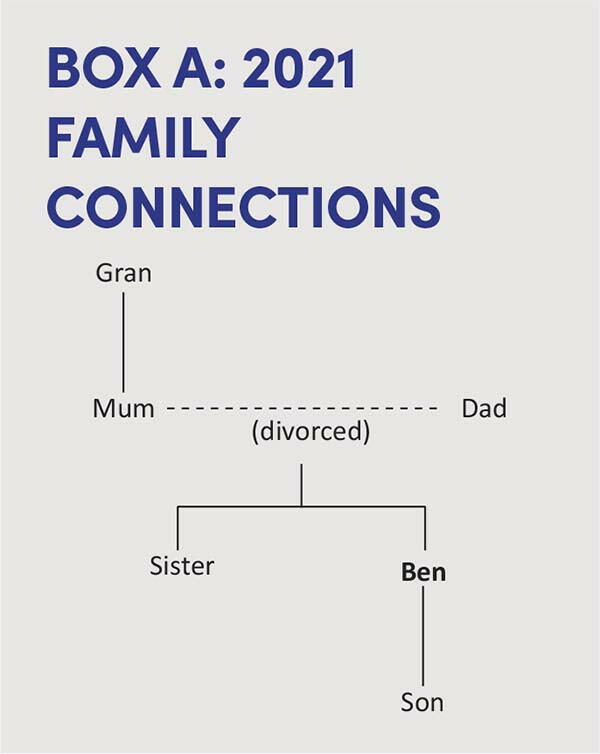

These types of relationship are easier to digest with an example and some pictures. Let’s say person B here is Ben. Ben is unmarried, and has a son from a previous relationship. His immediate family in 2021 is shown in Box A: 2021 Family Connections. They are all connected with him under group 2 above by virtue of being his relatives.

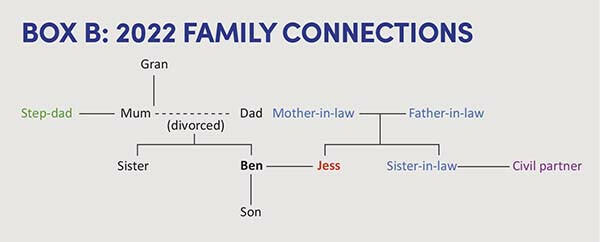

2022 is the year for long term commitments. Ben marries his new girlfriend Jess and his mum marries her boyfriend (making him Ben’s step-father). Jess’s sister enters into a civil partnership with her partner. Ben is now also connected with:

- Jess (under group 1);

- his mother-in-law, father-in-law and sister in-law (under group 3);

- his step-father (under group 4); and

- his sister-in-law’s civil partner (under group 5).

This is shown in Box B: 2022 Family Connections.

One may wonder which family members are not included under the primary definition. The most common examples are:

- aunts and uncles;

- nieces and nephews;

- cousins;

- partners of Ben and Jess’s relatives who are not married or in a civil partnership; and

- ex-spouses or ex-civil partners of Ben and Jess’s relatives, assuming that the marriage or civil partnership has legally ended.

The IHTA 1984 s 270 definition of connected parties extends the primary definition by including aunts, uncles, nieces and nephews in the meaning of a ‘relative’. Step-families do not fall neatly into any of the groups that are included in, or excluded from, the primary definition and are dealt with separately below.

Step-families

Step-relationships are not generally included within the legal definition of a particular family relationship. For example, a step-child or a step-parent is not included in the meaning of the word ‘child’ or ‘parent’ where it appears in tax legislation unless it is explicitly stated otherwise, such as in IHTA 1984 s 8K(3).

Despite this, an individual is still connected with their step-children and step-parents under the primary definition: step-children under group 3 as a relative of B’s spouse, and step-parents under group 4 as a spouse of B’s relative.

However, other types of step‑relationship are not included. An individual is not connected with their step-brother or step-sister.

Confusingly, there is a mismatch in the treatment of step-relations when looking across three generations. An individual is connected with their parent’s step-parent, but not their step-parent’s parent. Viewed the other way around, an individual is connected with their step-child’s child, but not their child’s step-child.

This brainteaser is much easier to follow using the diagram in Box B: 2022 Family Connections. Ben’s son is connected with Ben’s step-father but not with Jess’s mother (and vice-versa).

To create a step-family there must be a marriage or civil partnership between two individuals, at least one of whom is a parent of a child not biologically related to the other. Many families exist where the relationship between the parents has not been formalised by marriage or civil partnership. For example, Ben may have raised his son with Jess acting as the second parent but without marrying her. Even if his son considered Jess to be his step-mother, they would not have a family connection for tax purposes without her marrying Ben. Similarly, if Ben and Jess had married but later divorced, the connection between Ben’s son and Jess ends on the divorce.

If not already clear from the above, this highlights the critical importance of marriage and civil partnership to the concept of connected parties. This is reinforced by the continued connection between a couple who remain married or civil partners despite having been separated for many years.

Illegitimate children

Another family group that is defined in relation to marriage or civil partnership is illegitimate children.

This rather archaic term, which refers to children conceived and born outside of marriage, has been made largely redundant in UK tax law since the introduction of the FLRA 1987 s 1. Since then, an illegitimate child is connected to their parents under the primary definition of a family connection by virtue of being their lineal descendent.

Thankfully, there is consistency across all of the main direct taxing Acts. In each case, an illegitimate child will be connected with their parents. However, the position for IHTA 1984 and ITEPA 2003 is worth a separate comment.

Although IHTA 1984 was written before the Family Law Reform Act 1987, it borrows its definition from TCGA 1992 which was written afterwards. Therefore, as a matter of statutory interpretation, illegitimate children are connected with their parents in IHTA 1984. In other parts of IHTA 1984, however, the Act has to specifically extend the meaning of a child to include illegitimate children where the law deems it appropriate to do so (see IHTA 1984 s 22(2) for example).

From the post-1987 direct taxing Acts, ITEPA 2003 is peculiar in that it specifically disapplies FLRA 1987 s 1 for references to a ‘child’ or ‘children’ in the Act (see ITEPA 2003 s 721(6)). Again, this author’s view is that illegitimate children will still be connected with their parents in ITEPA 2003 because the connected parties definition is taken from an Act to which FLRA 1987 s 1 does apply, and that definition refers to lineal descendants rather than children. Furthermore, one would generally expect a court to avoid interpreting a statute such that illegitimate children are treated differently from legitimate children wherever possible.

It is worth highlighting, though, that the exclusion of illegitimate children from the meaning of the word ‘child’ in ITEPA 2003 does have major implications for other areas of the Act, such as the employment benefits code. In view of its inappropriateness to today’s society, one would like to think that this provision will therefore be removed.

Some readers may be surprised to learn that ITEPA 2003 s 721(6) excludes the application of FLRA 1987 s 1 to the Act, such that illegitimate children are not included as a child of their parents unless otherwise stated. However, the definition of connected parties in ITEPA 2003 is also borrowed from an Act to which FLRA 1987 s 1 does apply and so illegitimate children will still be connected with their parents in ITEPA 2003.

Although ITEPA 2003 s 721(6) does not impact on connected parties, it has serious implications for other areas which rely heavily on the definition of a family or household. For example, an illegitimate child that is independent of its parents will not be part of their parents’ family for the purposes of the employment benefits code. One would like to think that this provision will be removed.

Comment

Having looked in detail at the types of family relationship that result in two individuals being connected with each other, it remains to take a step back and question whether the rules make sense to families in the UK today.

In recent decades, the number of traditional ‘nuclear’ families has fallen as attitudes to marriage and family law changes. A variety of other family models have become more common, creating a diverse picture across the UK. Although the majority of families with children in the UK still involve parents who are married or in a civil partnership, their share of all families in England and Wales has fallen from 69% to 61% in the past 25 years alone (see the Office of National Statistics report ‘Families and households in the UK: 2021’ at bit.ly/3vN8zDb).

Like many parts of the tax code, the connected parties rules may be starting to lose their appropriateness as the nuclear family declines in significance. With marriage and civil partnership at the heart of these rules, a number of family relationships are left outside of their purview.

In reality, the fact that two family members are not connected for tax purposes under the primary definition may come as good news to them. In the case of unmarried couples, it perhaps offsets some of the tax disadvantages they face by not being married. But clearly there is an issue for policy makers as they try to ensure that the connected party rules meet their intended aims without creating knots for those that do not wish to tie them.