Demolition job

Share this article

Sam Dewes considers the tax complexities of demolishing a property in order to rebuild, rather than simply renovating

Key Points

What is the issue?

If you want to make major changes to your home it is often easier and more cost effective to start from scratch, rather than renovating the existing structure. This can have a significant impact on capital gains tax.

What does it mean for me?

A deemed disposal can be triggered in respect of the site of the building by treating it as having been sold and immediately reacquired for consideration equal to the market value of the land site at that time.

What can I take away?

Given the number of factors at play, each case will need to be considered on its own merits to see if a claim is worthwhile to secure the resulting tax savings.

Watching your house fall to the ground may sound like a homeowner’s worst nightmare. And yet, many people are willing to pay for the service of having their property knocked down. What is behind this seeming act of recklessness? As it turns out, if you want to make major changes to your home it is often easier and more cost effective to start from scratch, rather than renovating the existing structure.

Take the example of Jenny. She moved out of London with her family, selling her house for £3 million, and bought a new house in Surrey for £2 million, keeping back some of the proceeds for much needed renovations on her new home. After six months of living there, she realises that the house is not suitable for her family to live in until her planned renovations take place, and so she moves the family into rented accommodation. Having moved out, and following a consultation with the architects, she discovers that the house requires more work than she originally thought. Therefore, 18 months after purchasing it, she decides that it would be better to knock down the house and start again. It is unlikely that under such strain, capital gains tax is on her radar. So, let us consider for her the capital gains tax consequences of her decision. All statutory references are to Taxation of Chargeable Gains Act 1992.

Does the demolition create a disposal?

A deemed disposal is created ‘on the occasion of the entire loss, destruction, dissipation or extinction of an asset’ (s 24(1)). Under land law, Jenny’s asset is the interest she holds in the land on which her Surrey house once stood. She therefore does not destroy her asset (the land) by demolishing the house. However, s 24(3) goes on to say that ‘a building … may be regarded as an asset separate from the land on which it is situated’. The effect of this provision is that a deemed disposal can be triggered under subsection 1 in respect of the site of the building (including any land occupied for purposes ancillary to the use of the building) by treating it has having been sold and immediately reacquired for consideration equal to the market value of that site at the time the house is demolished. There are some important points to note here:

- Only the entire destruction of an asset will create a disposal under s 24(1). HMRC is likely to take this literally; i.e. to create a deemed disposal nothing but the foundations of the building can remain after the demolition.

- It is the site of the building that is treated as having been sold and immediately reacquired at market value. In some cases, the land area owned will be larger than what is ancillary to the site of the building, leading to a part disposal. Furthermore, for some clients the market value of the site of the building will in itself be worth more than the total acquisition costs of the original house, perhaps because valuable planning permission has been obtained since it was purchased or because of a substantial increase in the land value between acquisition and demolition.

- The legislation states that a person may regard the building as separate from the land. This denotes a choice. Jenny can decide if she wants to create a disposal when the entire building is demolished. The default position appears to be that the disposal is not triggered, such that the demolition costs will simply be added to the enhancement expenditure that is deductible from a future sale of the house (see HMRC manual CG15200).

So what are the potential advantages of creating a disposal in such circumstances?

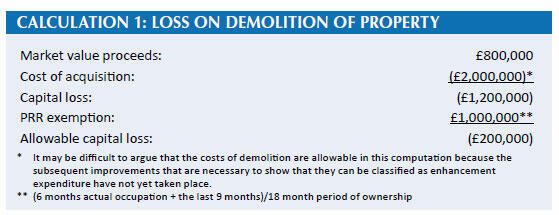

Firstly, if the disposal gives rise to a capital loss, then treating the house as separate from the land under s 24(3) will enable the owner to accelerate the use of the loss by claiming it in the tax year of the deemed disposal.

In Jenny’s case, let’s assume that the market value of the site of the house was £800,000 after the demolition. Part of the capital loss arising is disallowed due to private residence relief (PRR) because the house was her main residence for six months (see Calculation 1). Jenny’s new base cost of the site of the house will be equal to its market value at the time of the demolition which, being lower than her acquisition costs, means that she has reduced her base cost on a future disposal. However, this is not necessarily a problem, as will now be explained in relation to the second potential advantage of creating the deemed disposal.

Impact of deemed disposal on private residence relief

The second advantage is that by triggering the deemed disposal, arguably a new period of ownership for PRR purposes is created. As established in Henke v HMRC [2006] SpC 550, the period of ownership for PRR purposes is the date on which the land is acquired. Therefore, without the deemed disposal, the period of ownership began when the demolished house was acquired.

Triggering the deemed disposal is of particular benefit for individuals who were not living in their property prior to its demolition because that period of non-occupation falls away when the new period of ownership starts. Furthermore, if the construction works are completed within two years of the deemed disposal (i.e. since the demolition) such that the owner can move into the new house, this period should be covered by the deemed occupation provided for by s 223ZA for delays moving into your home.

In Jenny’s case, one might think that the time when she was absent from the property due to the demolition or reconstruction works would be covered by the period of absence for any reason, which can extend to three years, as long as she moves back into the new house as her main residence (s 223(3)(a)).

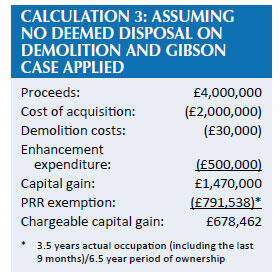

However, HMRC could argue that, based on Gibson v HMRC [2013] UKFTT 636, the occupation of the original house is ignored because it is a completely separate dwelling from the new house. Whilst this case was heard only at the First-tier Tribunal (and the tribunal was not unanimous in its decision – the casting vote going to the tribunal judge), it nonetheless poses a serious risk for individuals who are relying on occupation of an existing property (before it is demolished) to improve the PRR position on the new property (built in its place).

By triggering the deemed disposal, Jenny therefore alleviates the risk of HMRC making this argument, and the new house is treated as a separate dwelling with a new period of occupation and ownership.

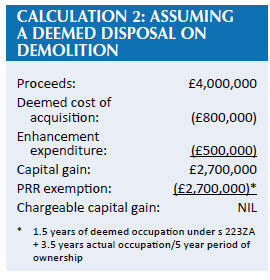

Calculations 2 and 3 highlight the impact of making the deemed disposal on a future sale of the new house by Jenny. They are calculated on the basis that Jenny:

- sells the new house five years after the demolition of the old one for net proceeds of £4 million;

- spent £30,000 on demolishing the original house and £500,000 building the new house; and

- moved into the new house 1.5 years following the demolition.

Clearly, in Jenny’s case, she is better off triggering the deemed disposal on demolition. She has created a capital loss of £200,000 and, because she lives in the property as her main residence after it is constructed, her entire subsequent gain of £2.7 million is exempt.

An alternative method of doing the calculations could be to time apportion the gain on a just and reasonable basis under s 224(2), before applying PRR to those separate parts. Those wanting to explore this further may want to look at Ritchie & Anor v HMRC [2017] UKFTT 449, where a fairly generous approach was applied.

Given the number of factors at play, each case will need to be considered on its own merits to see if a claim under s 24(3) is worthwhile. In particular, care must be taken to ensure that claiming the loss is actually possible; i.e. has the entire building been demolished? However, as demonstrated with Jenny, where the deemed disposal can be claimed, this little known provision can offer some tax savings to lift the spirits as the walls come down.