The cost of reform

Share this article

Jane Mellor sets out the CIOT and ATT’s responses to Treasury plans for an Economic Crime levy

Key Points

What is the issue?

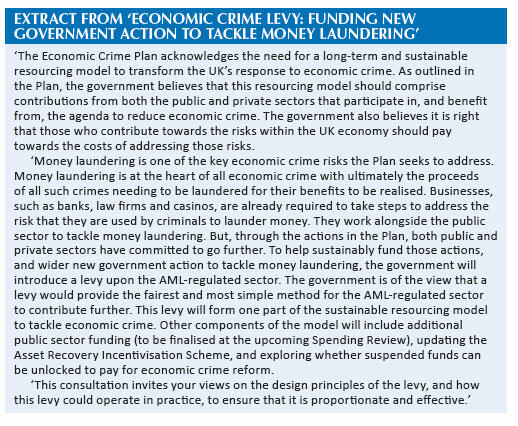

HM Treasury have been consulting on an Economic Crime Levy to fund new government action to tackle money laundering and help deliver Economic Crime plan reforms. The CIOT and ATT responded in detail to the consultation.

What does it mean for me?

Members who are subject to AML Supervision by the CIOT and ATT should be aware of the potential levy and the case put forward by the CIOT and ATT in their consultation response.

What can I take away?

The fight against money laundering and financial crime continues to be a focus for the government and the potential for the introduction of a levy brings another change on the horizon.

Even before the revelations of the recent Financial Crimes Enforcement Network (FinCEN) leaks, the UK government had plans in place to press ahead with additional reforms to tackle the threat from economic crime. Economic crime includes money laundering, fraud, bribery and corruption, and terrorist financing. It is impossible to say accurately the scale of all these crimes, although the National Crime Agency estimates that the scale of money laundering alone impacting the UK annually is in the hundreds of billions of pounds.

The 2019 Economic Crime plan (see bit.ly/361o9Q3) sets out the UK response to economic crime and builds on the commitments of earlier plans. Important elements include the reform of the suspicious activity reporting system, improving the response to fraud, information sharing and enforcement.

Reform has to be funded and at Budget 2020 the government announced its intention to introduce an economic crime levy. In July 2020, a consultation was launched (see bit.ly/3q1UG0c) inviting views on a variety of areas in relation to the levy, including design principles, how it could operate, what it would fund and how it should be collected.

The CIOT and ATT both responded to the consultation in some detail, including coverage of the nature of the tax advice market and the disproportionate burden that anti-money laundering compliance already places on smaller tax practitioner firms. We also ensured that member representatives with an understanding of operating in small firm environments took part in associated roundtable discussions.

The principles applying to the levy The levy principles set out in the consultation document are as follows:

- proportionality and affordability;

- solidarity;

- simplicity and transparency;

- predictability;

- cost effectiveness of levy collection; and

- avoiding unintended consequences.

The CIOT and ATT response agreed these principles and pointed out that they should be applied to the costs and burdens of anti-money laundering compliance overall, and that the levy should be considered as part of the overall picture. In relation to the principle of solidarity, all parts of the anti-money laundering regulated sector are required to meet the same legislative requirements, irrespective of size. For example, all firms, even sole practitioners with no employees, have to have written policies and procedures and a written practice risk assessment in the same way as the largest firms.

What should the levy fund?

Areas requiring levy funds as set out in the Economic Crime plan include:

- suspicious activity reporting reform programme;

- increased resources and staffing for law enforcement agencies involved in the response to economic crime;

- awareness raising campaigns; and

- Companies House reform.

The CIOT and ATT responses agreed that the levy should pay for the priorities under the Economic Crime plan and the money should be ringfenced.

We noted in the response document that the government should raise money in as few ways as possible and with as few additional collection costs. Medium to longer term planning should aim to look at overall needs over that period in order to minimise repeated requests for additional funding via different levies and fees.

The levy calculation

The consultation document set out a number of potential ways of calculating the levy, including:

- a fixed percentage of current anti-money laundering supervision fees;

- a fixed charge per business;

- a levy proportionate to the number of suspicious activity reports submitted; or

- the number of employees or business owners, officers and managers.

However, the consultation indicated that ‘the government currently assesses revenue as the most desirable levy base’ and considered issues such as a single fixed percentage, fixed amounts based on revenue bands, the exemption of small businesses and how to take into account money laundering risk.

The CIOT and ATT responded to indicate that the only fair basis of allocating costs of regulation was by reference to fees, being a fair indicator of the scale of operation and level of risk. We strongly supported the proposal that businesses with fees below £10.2 million (the small company threshold in the Companies Act 2006) should be exempted from paying the levy.

The CIOT and ATT submitted background information on the way in which the tax market operates and evidence of the size of firms supervised by the CIOT and ATT. We referenced the considerable increase in costs already borne by our supervised firms over recent years as a result of required increased supervisory activity and the Office for Professional Body AML Supervision (OPBAS) levy passed on as part of anti-money laundering renewal fees.

The CIOT and ATT recognise the loyalty of our membership and the high standards of conduct which they embrace. However, we took the opportunity to make the point that escalating costs could push advisers out of the market or out of the scope of professional body membership. This could only have a detrimental impact on those with lower incomes who use smaller firms with a lower cost base (and lower fees). Firms serving this market can find it hard to pass on any cost increases and may simply choose to exit the market, thus reducing the choice of advisers for those on lower incomes. It could also increase the number of firms acting outside the requirements of professional body standards which is not in line with public policy objectives to improve the standards applying to tax agents.

Collection of the levy

The consultation document considered the best method of collecting the levy and asked for responses on whether there should be collection by the current anti-money laundering supervisory bodies or a single agency.

From a practical perspective, there are a number of hurdles to the CIOT and ATT acting as a collection agency. The collection of a government debt such as the levy would require changes to the CIOT Royal Charter and the ATT Articles of Association, together with potential updates to agreements with members. It would create significant additional administrative costs for CIOT and ATT, which would have a knock-on effect on supervisory costs to pass on to firms and would divert resources from other CIOT and ATT charitable objectives.

In our view, HMRC is uniquely placed as it has the power to collect and enforce the payment of government debt. It would make sense to use this existing model, especially since they would have to have systems in place to collect the levy from their supervised firms.

Where do we go from here?

The response to the consultation document is expected in Spring 2021 and is likely to be followed by further consultations and draft legislation. The CIOT and ATT will update members on possible changes as soon as further details become available and will continue to voice concerns about additional costs in this area and increased administrative burdens on our supervised populations.