Cross-border structuring: US citizens with UK limited companies

Share this article

UK advisers must address US CFC, GILTI and reporting risks when US citizens operate through UK private companies.

Key Points

What is the issue?

A UK private limited company owned by a US citizen is treated as a foreign corporation for US tax purposes and may be a controlled foreign corporation. This can trigger GILTI, Form 5471 reporting and US tax on retained profits.

What does it mean to me?

UK advisers face both tax and compliance risk. Profits retained in the company may be taxed currently in the US, dividends may attract non-treaty-relieved NIIT, and reporting failures can carry significant penalties.

What can I take away?

Identify US citizenship early, model profits across both systems, consider whether a §962 election is appropriate, and ensure US filing obligations are built into engagement planning.

UK practitioners increasingly advise US citizens who are resident in the UK and operate through UK private limited companies. At first glance, the structure appears straightforward: incorporation under the Companies Act 2006, profits subject to UK corporation tax, and remuneration extracted through salary and dividends.

However, for US citizens, a UK company does not operate solely within the UK tax system. The United States taxes its citizens on worldwide income regardless of residence. As a result, a UK-incorporated company owned by a US citizen frequently falls within the US controlled foreign corporation (CFC) regime, bringing into play anti-deferral rules such as global intangible low-taxed income (GILTI), together with extensive information reporting obligations.

For UK advisers, the technical issue is not merely double taxation in the conventional treaty sense. It is the structural interaction between UK corporation tax, UK personal taxation and US anti-deferral rules that can trigger current US tax on profits retained in the UK company.

This article is written for UK accountants and tax advisers who act for US citizen clients operating through UK private limited companies. It focuses on the interaction between regimes rather than domestic compliance in isolation, with particular emphasis on US CFC classification, GILTI under IRC §951A, the IRC §962 election and Form 5471 reporting obligations. These areas most frequently give rise to unexpected tax exposure – and professional risk – for UK firms. A single fact pattern is used throughout to illustrate structural mismatches rather than restating basic rules.

The core fact pattern: Harper Advisory Ltd

Harper Advisory Ltd is a UK private limited company incorporated under the Companies Act 2006. It provides consultancy services to UK and overseas clients and is wholly owned by a US citizen who is UK resident under the statutory residence test and performs all substantive services from the UK.

The company generates annual profits of £200,000 before remuneration. The shareholder-director draws a salary of £50,000, receives dividends of £75,000 and retains £39,000 within the company. This profile is representative of many owner-managed professional services businesses and provides a realistic base case for cross-border analysis.

The £50,000 salary requires careful consideration of the US-UK Totalization Agreement – a bilateral social security agreement between the US and the UK intended to prevent double social security taxation and to co-ordinate benefit entitlements for individuals who work in both countries. Without a Certificate of Coverage, the client could potentially face double taxation through Social Security and National Insurance liabilities, if challenged by the Internal Revenue Service (IRS). UK advisers should therefore ensure social security co‑ordination is addressed early in the engagement.

UK legal status and corporation tax

From a UK perspective, the position is conventional. Harper Advisory Ltd is a separate legal person under the Companies Act 2006 and is UK resident for tax purposes by virtue of its incorporation under the Companies Act 2006. Its worldwide profits are chargeable to corporation tax under the Corporation Tax Act 2009.

For 2025-26, UK corporation tax applies at 19% on profits up to £50,000. Profits between £50,001 and £250,000 fall within the marginal relief band, producing a tapered effective rate between 19% and 25%. Profits exceeding £250,000 are taxed at the main rate of 25%.

On taxable profits of £150,000 after salary, Harper Advisory Ltd falls within the marginal relief band, producing an effective rate of approximately 24%. These rates are critical to later analysis because the effective rate, rather than the headline rate, determines whether US inclusions can be offset through foreign tax credits.

US entity classification and Form 5471 exposure

A frequent source of error among UK practitioners is the US tax classification of a UK private limited company.

Under US entity classification regulations (Treasury Regulation §301.7701-2(b)(8)), a UK private limited company is automatically classified by the IRS as a corporation for US tax purposes and is therefore treated as a foreign corporation from inception. It is not generally eligible to elect partnership or disregarded entity treatment, even where there is a single shareholder. For UK advisers, this means that the US tax characterisation of the structure is fixed and cannot be simplified through election.

Once a US person is a ‘US shareholder’ (generally 10% or more of the vote or value, including constructive ownership), Form 5471 reporting may be triggered under the category tests (such as acquisition events, control or controlled foreign company (CFC) status). Advisers must apply the specific Category 2–5 rules, not just the 10% threshold in isolation.

Where more than 50% of the vote or value is held (directly or indirectly) by US shareholders, the company is a CFC and majority US owners typically fall within Category 4 and/or Category 5 filing. These categories impose the most comprehensive ongoing reporting requirements for CFCs. For Category 4 and 5 filers, Form 5471 requires detailed financial statements, earnings and profits tracking, and disclosure of relatedparty transactions.

Penalties for non-filing or incomplete filing begin at $10,000 per form per year under IRC §6038 and can escalate quickly where non-compliance continues after IRS notification. For many UK firms advising US citizen shareholders, Form 5471 compliance represents the most significant area of professional risk within the structure.

CFC status and the operation of GILTI

Because Harper Advisory Ltd is wholly owned by a US person, it is a controlled foreign corporation within the meaning of IRC §957. This status activates the US anti-deferral regime, including Subpart F. However, the more significant provision for professional services companies is the Global Intangible Low-Taxed Income (GILTI) regime under IRC §951A.

GILTI requires a US shareholder to include annually their pro rata share of the company’s ‘tested income’, regardless of whether profits are distributed. The regime is designed to limit the ability of US taxpayers to defer US tax by accumulating profits within foreign corporations.

In practice, many UK professional services companies are particularly exposed, as their value is derived primarily from human capital. GILTI allows only a limited reduction, which is based on tangible assets. Where tangible assets are minimal, most of the company’s accounting profit may constitute tested income for US purposes.

In practical terms, retained profits within a UK company may still be subject to US taxation each year, even if no money is taken out. This often surprises UK advisers who expect retained profits to be taxed only when distributed.

In the Harper Advisory Ltd scenario, the £39,000 of retained earnings would typically give rise to a current US inclusion under the GILTI rules, even though no distribution has been made.

Mitigating GILTI: the section 962 election

For individual shareholders, the principal statutory mitigation is an election under IRC §962. This election allows the shareholder, for the purposes of Subpart F and GILTI inclusions, to be treated as if they were a US corporation.

The practical consequence of this is that the individual may gain access to the section 250 deduction applicable to GILTI and to deemedpaid foreign tax credits under IRC §960. This may materially reduce the incremental US tax exposure on GILTI inclusions.

However, the election does not eliminate complexity. If profits that have previously been taxed under a §962 election are later distributed, further US tax may arise at shareholder level. The alignment between UK corporation tax and US taxation is therefore improved but is only partial.

Advisers must therefore still consider the downstream taxation of distributions of previously taxed earnings and the interaction with UK dividend taxation.

UK personal taxation and treaty limits

At shareholder level, the UK tax treatment follows established principles. Salary is subject to income tax under ITEPA 2003 and National Insurance contributions under the Social Security Contributions and Benefits Act 1992, while dividends are taxed under the dividend regime in ITA 2007.

From a US perspective, both salary and dividends are included in gross income under IRC §61. Salary is generally taxed as ordinary income, while dividends are taxed as foreign dividend income.

A further complication arises when a UK company pays a dividend to a US citizen, as that dividend is usually subject to an additional 3.8% US Net Investment Income Tax (NIIT) under US IRC §1411. Importantly, the US-UK Double Tax Treaty does not give relief for NIIT, so this tax cannot be offset by UK tax paid on the dividend.

As a result, dividends received from a UK company often carry an additional non-recoverable US tax charge, even where UK tax has been paid at rates exceeding the US federal dividend rate.

The treaty mitigates juridical double taxation in many cases, but it does not override GILTI inclusions or eliminate NIIT exposure. UK advisers should therefore be cautious in assuming that treaty relief will fully resolve cross-border mismatches.

Consolidated tax layering and timing risk

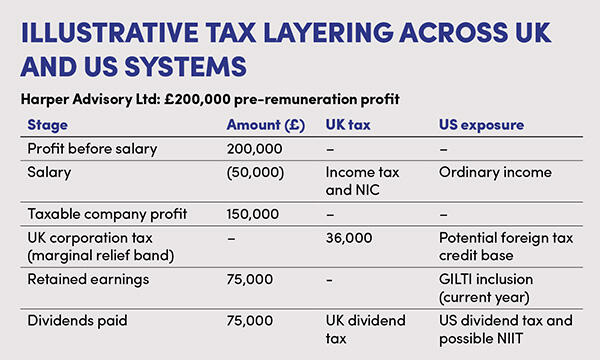

The interaction of corporation tax, personal taxation and US anti-deferral rules can be seen by tracing Harper Advisory Ltd’s economic profit of £200,000 through each layer of the structure.

After paying a £50,000 salary, taxable profits of £150,000 arise, giving rise to UK corporation tax within the marginal relief band. Of the taxable profit, £75,000 is retained and £75,000 is distributed as dividends. The table Illustrative tax layering across UK and US systems summarises how that profit is taxed at company and shareholder level in both jurisdictions.

Double taxation arises not from a single conflict, but from cumulative system interaction. Timing mismatches between UK corporation tax payments and US inclusion years may further complicate the availability of foreign tax credits. Modelling the full lifecycle of profit – generation, retention and extraction – is therefore essential when advising US citizen shareholders of UK companies.

Compliance exposure and professional risk

Beyond substantive tax cost, US information reporting obligations represent a material professional risk.

Advisers must consider Form 5471, FBAR (FinCEN Form 114) reporting and Form 8938 (under the FATCA regime). These filing obligations carry strict statutory penalties that apply independently of underlying profitability. In some cases, the penalties for non-compliance can exceed the tax at stake.

For UK firms, this underlines the importance of an integrated advisory approach, grounded in realistic modelling, early identification of US shareholder status, and a clear assessment of compliance risk. Where this is achieved, the structure can function effectively; where it is not, it remains a frequent source of retrospective correction and professional exposure.

© Getty images