Before death do us part

Share this article

In the second of her two-part series, Emma Chamberlain considers the inheritance tax issues for divorcing couples

Key Points

What is the issue?

In many ‘big money’ cases, it will be desirable that some of the property transferred to the spouse is retained in trust rather than given to them outright

What does it mean to me?

Transfers into trusts, whether or not interest in possession, are normally chargeable transfers and the trust will be subject to 10-year anniversary charges and exit charges

What can I take away?

If a court order directs a spouse to hold a cash sum or a particular house under declaration of trust made by them as initial sole trustee there will not be a chargeable transfer

Assets can be transferred between husband and wife or civil partners or same-sex spouses of the same domicile without attracting an inheritance tax (IHT) charge up to decree absolute, whether or not they are separated (IHTA 1984 s 18). This is in contrast to the capital gains tax treatment discussed in my article Capital split (Tax Adviser, June). The spouse exemption is restricted when assets are transferred from a UK domiciled spouse to a foreign domiciled spouse. But a domicile election made by the transferee spouse can now cover any potential inheritance tax risk (IHTA 1984 s 267ZA). Statutory references refer to IHTA 1984 unless stated otherwise. References to spouses should be taken to include references to civil partners and same-sex couples.

After the decree absolute, the spouse exemption in IHTA 1984 s 18 does not apply, although two statutory provisions may still provide relief for transfer between themselves. First, s 10 provides that a transfer of assets not intended to confer any gratuitous benefit is not a transfer of value.

Second, s 11 provides that a disposition will not be a transfer of value if it is made by one party to the marriage or civil partnership in favour of the other party; or to a child of either party to the marriage or former marriage and is:

- for the maintenance of the other party; or

- for the maintenance, education or training of the child for a period ending not later than the year ending April 5 in which the child attains 18 or, if later, finishes full-time education.

Under s 11(6) relief can also apply to dispositions for the maintenance of a divorced spouse or civil partner is dissolved or annulled and to the later variation of a disposition so made, for example, on the remarriage of the other party.

In most cases dispositions made on divorce or on termination of a civil partnership are made after arms’ length negotiations or under the terms of a court order. They are therefore not treated as transfers of value. This could be because they come within s 10 or, more likely, they are not dispositions at all because the liability is imposed by law under a court order.

Section 11 is of more use in the context of provision for children. However, it could be useful after a divorce if the parties wish to change maintenance orders between themselves without obtaining a court order. This could apply when an ongoing maintenance order is capitalised into a lump sum.

The property of an ex-spouse no longer affects the value of property of their former partner because it is no longer ‘related property’ within s 161. Divorce means that the parties are no longer connected persons for IHT purposes. Because the spouse exemption is no longer available, any gift between ex-spouses can be caught by the reservation of benefit provisions (FA 1986 s 102(5)(a)). If the disponer spouse wishes to retain a benefit in any trust he or she set up for the other spouse, bear in mind the property may be taxed as part of his or her estate for IHT purposes.

It is not possible to claim the unused nil rate band of a predeceasing spouse if the couple have divorced.

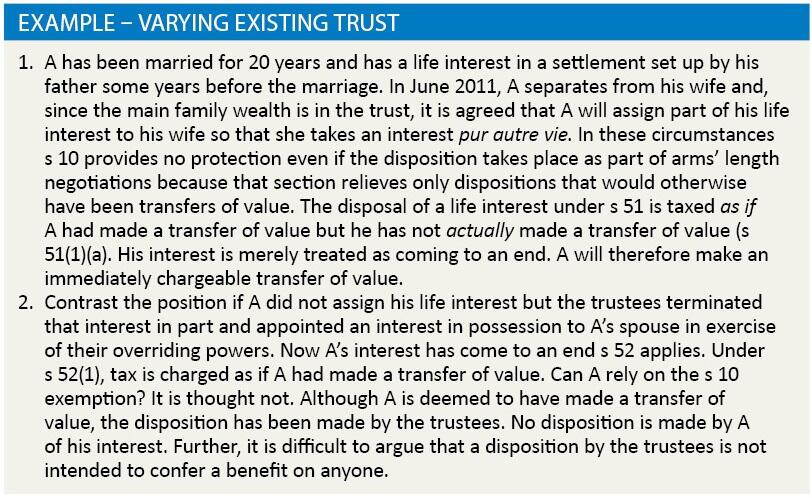

Varying existing trusts

Divorce settlements may not simply involve one spouse transferring assets outright to the other or settling assets owned on trust for the other. The principal financial resource of the family may be the assets already contained in a settlement in which one spouse has a life interest and it is desired that the trust should be varied to allow the other spouse to receive benefits. The trustees may not have power to advance capital to either spouse or may be reluctant to do so if the settlor was, say, the divorcing spouse’s father who wanted capital to pass to grandchildren. The trust assets may not be readily realisable or the trust may have been offshore and contain significant stockpiled gains which will make an outright distribution of capital expensive. In these circumstances, how can the trust assets best be rearranged?

In the Example, if the couple are still married it would be possible to obtain spouse exemption if the trustees terminated A’s interest in part and advanced the property to A’s spouse absolutely. Otherwise for divorces after 5 October 2008, the couple will need to consider the potential IHT charges arising on varying a trust where A’s qualifying interest in possession is ended and in terms of future 10-year anniversary charges.

In short, variations of qualifying interest-in-possession settlements have become problematic for IHT purposes.

Bear in mind that, if the settlor was not UK domiciled or deemed domiciled, there is no IHT problem about varying trusts that hold no UK situated assets because these are excluded property settlements. Nor is there any difficulty if the trust is already a relevant property settlement. An appointment of an interest in possession to one spouse or another is a non-event for IHT purposes.

Setting up new trusts

In many ‘big money’ cases, it will be desirable that some of the property transferred from one spouse to the other, is retained in trust, rather than given outright. The transferring spouse then feels that there is some guarantee that the assets will eventually pass to the children of the marriage rather than to a future partner of the ex-spouse.

Before FA 2006, a spouse could settle the assets on interest-in-possession trusts for his spouse and spouse exemption would have been available if the transfer took place before decree absolute. The trust would have been outside the relevant property regime. The spouse could then enjoy the income and use of the assets which would pass on to the children when the ex-spouse died.

Since 22 March 2006, all inter vivos transfers into trusts, whether or not interest in possession, are chargeable transfers unless the spouse is disabled. The trust property will accordingly fall into the relevant property regime. A transfer of £500,000 into an interest-in-possession trust for the spouse could, in the absence of any other relief, attract a 20% IHT charge on the excess above the £325,000 threshold and the trust would be subject to 10-year anniversary charges and exit charges.

Is there a solution to this dilemma? One option is for the transferor spouse to give the house or cash sum outright to the other spouse but impose conditions, for example, that the transferee spouse must undertake to leave the house outright to the children on death, or that on sale the proceeds over a certain amount must be left to them. However, enforcing all this many years hence would be difficult. Possibly, the house could be put in the legal name of an independent bare trustee and held absolutely for the transferee spouse to ensure better enforcement of the undertakings. A charge could be placed on the house as security for the undertakings.

In practice, if the house is held for the transferee spouse absolutely it will be difficult to stop that spouse mortgaging or selling it. If too many conditions are imposed, or conditions are varied later, there is a risk that a settlement is created inadvertently, at least for inheritance tax purposes. No gratuitous intention is required for a settlement to arise for IHT purposes, leading to unexpected inheritance tax charges every 10 years. It is better to be clear either way as to whether a trust has arisen.

A solution is for the court to exercise its powers against the husband (H), say, assuming he is the wealthier party – under the Matrimonial Causes Act 1973. The relevant MCA 1973 s 24(1)(b) enables the court ‘to order that a settlement of such property as may be so specified, being property to which a party to the marriage is so entitled, be made to the satisfaction of the court for the benefit of the other party to the marriage and of the children of the family or either or any of them.’

H could be directed to hold a cash sum or a particular house under declaration of trust made by him as initial sole trustee (other trustees could be appointed later) annexed to the court order for his wife (W) and the children. The trust can be used to buy a home to ensure parity in living standards between W and H; it can ensure that the children have an equal standard of accommodation with both parents.

However, W will not be entitled to any capital. She will be entitled to live in any property rent-free and receive the income from any proceeds should it be sold. There could be power to advance capital to the children while W is alive if she no longer has need of the house or such a large house, but only if she consents.

This new trust will be subject to 10-year and exit charges in the future. The settlor will have to settle or add enough funds to allow for this or agree to fund the charges. The settlor should be excluded to avoid any reservation of benefit problem. Is there an entry charge on setting up the trust? It is clear that there is no gratuitous benefit and no loss to H’s estate when the settlement is set up because he is simply transferring property in settlement of W’s matrimonial claims against him pursuant to a court order. As Haines v Hill [2007] EWCA Civ 1284 indicates, the court is not taking away from one party and giving to the other. All that the court is doing is quantifying each party’s respective entitlements as a matter of law.

It is sometimes said that there is no entry charge because s 10 protects the transaction. Section 10 provides that a disposition is not a transfer of value if it is shown that it was not intended and it was not made in a transaction intended to confer any gratuitous benefit on any person and either it was made in a transaction at arms’ length between persons not connected with each other or it was such as might be expected to be made in a transaction at arms’ length between persons not connected with each other.

However, s 10 is intended to apply where there has been a loss to someone’s estate due to a bad bargain, but no gift is intended. This would be so if 2% of a controlling shareholding was sold to a third party but the loss of control was much greater than the price received. In this case the value of H’s estate is the same before as afterwards; it is simply that the obligations he owes W have been satisfied. He is merely doing what the court has required him to do anyway. As Haines confirms, the transfer is not gratuitous and is protected from Insolvency Act claims because neither party’s estate is reduced. In any event, even if there were a loss, it is not a disposition made by H, but a disposition made pursuant to the court order. The basic charging provisions of s 10 are not engaged. As was made clear in de Lasala v de Lasala [1980] AC 546 by Lord Diplock:

‘Financial arrangements that are agreed upon between the parties for the purpose of receiving the approval and being made the subject of a consent order by the court once they have been made the subject to the court order are no longer dependent upon the agreement of the parties as the source from which their legal effect has derived. Their legal effect is derived from the court order.’

This has been accepted by HMRC in the CGT context. See CG22420 which confirms that the legal effect of any provisions embodied in the order is derived from the order itself and does not depend on any anterior agreement between the parties.

FA 2010 s 53 charge

It has been suggested that this anti-avoidance section might apply on the basis that the interest in possession taken by W could fall within s 5(1B). This is on the basis that W is domiciled in the UK and has become beneficially entitled to it by virtue of a disposition which s 10 prevented being a transfer of value. That in turn would bring in s 49(1) and, on W’s death, she would be treated as owning the underlying property in which her interest subsists. The trust would be subject to ten-year charges and a charge on W’s death. However, if, as HMRC have confirmed is the case, s 10 does not apply in the first place, this analysis is misconceived. Even if s 10 did apply, W has not given consideration within the meaning of FA 2010 s 53, nor is there a disposition made by either party – the disposition has been made by order of the court. See the judicial observations made at para 43 in the case of G v G [2002] EWHC 306 (Fam), discussed in my June article. As Morritt said at para 30 of Haines, the fact the transfer ordered by the court does not give rise to a payment of consideration so as to reduce the value of holdover relief for capital gains tax does not entail a conclusion that a property adjustment order must be regarded as being made for no consideration within the meaning of the Insolvency Act. It is consistent with the CGT position that there is no transfer of value for IHT purposes and that W has not given consideration for the purposes of FA 2010 s 53. HMRC have accepted this analysis.

Of course, whether the parties will agree to the imposition of a trust where H has to fund future 10-year charges and W has less freedom to deal with the house as she chooses are issues that will have to be resolved by the matrimonial lawyers. A trust is likely to be a solution only in big money cases. However, the IHT position of such a trust now seems reasonably clear.

Further information

A fuller consideration of these issues can be found in Trust Taxation and Estate Planning – 4th Edition (Sweet & Maxwell) by Chamberlain and Whitehouse.