Deregistration tips

Share this article

Many businesses might benefit from VAT deregistration. Neil Warren considers some practical issues and VAT saving tips.

Key Points

What is the issue?

A business can deregister at any time if it expects taxable sales in the next 12 months will be less than the deregistration threshold. Could this be a worthwhile opportunity for many small businesses? A business cannot deregister on a retrospective basis if it is still trading so it is important to identify the potential benefits when they arise.

What does it mean to me?

The rules for deregistration can be tricky, particularly for users of the flat rate scheme or a business that owns stock and assets when it deregisters. It is important to be aware of these rules to maximise tax saving opportunities and also to submit an accurate final return before the business deregisters.

What can I take away?

Many businesses might be registered on a voluntary basis because they have saved tax in the past using the flat rate scheme. But many of those gains ended when the ‘limited cost trader’ category came into effect on 1 April 2017 so deregistration might now be worthwhile in many cases.

Life without worrying about VAT might be an attractive thought for many small business owners. I know that many businesses which were voluntarily registered decided to call it a day when the new ‘limited cost trader’ category was introduced to the flat rate scheme (FRS) on 1 April 2017, with its very high rate of 16.5%, which removed most of the financial savings that scheme users had enjoyed for many years. And many other business owners might be tempted to escape before the introduction of Making Tax Digital in April 2019, with its link between VAT returns and online submissions. So it is a good time to consider some practical issues with the deregistration process and a few tax saving tips as well.

Basic rules

Here are the basic rules for deregistering a trading business:

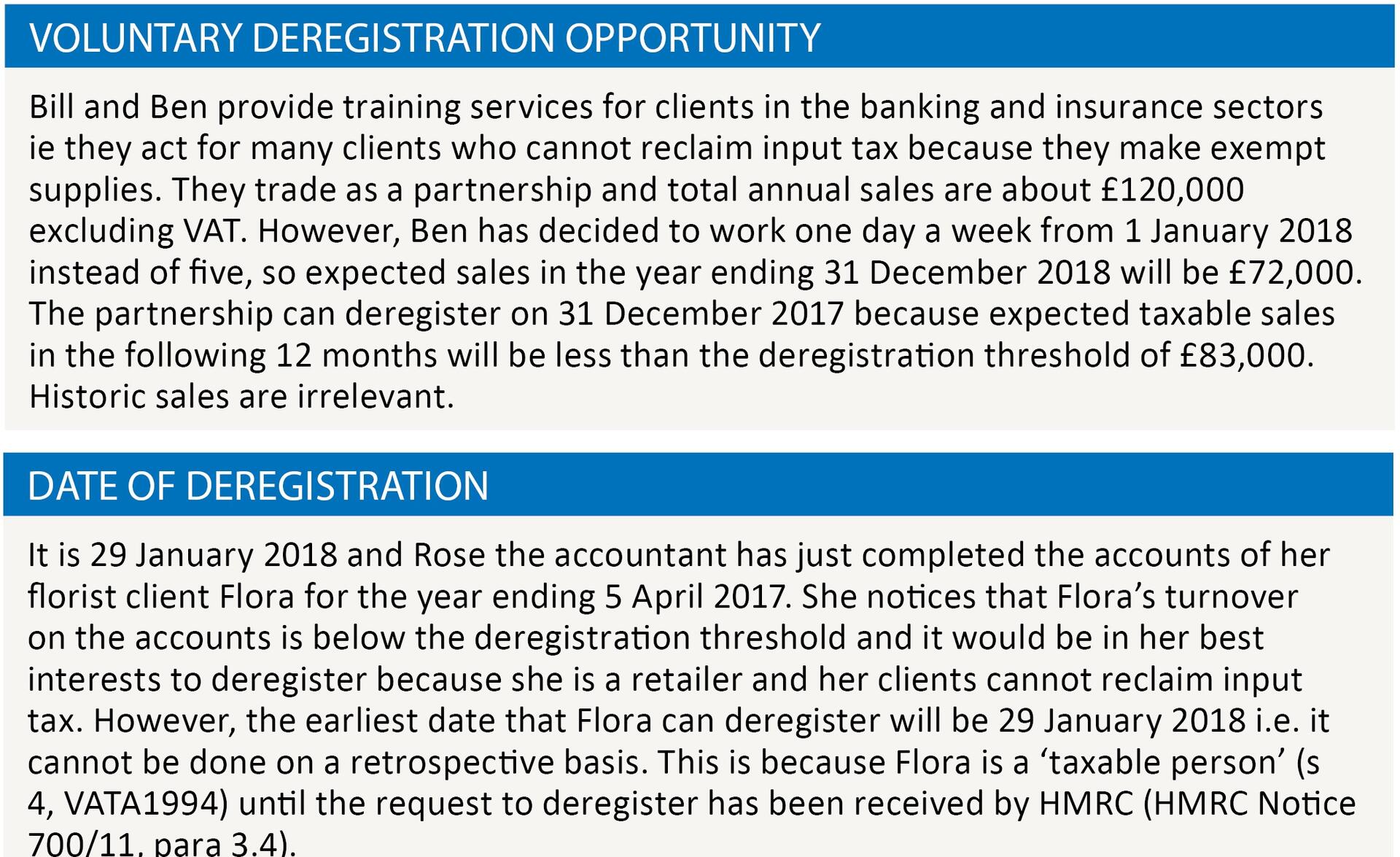

- A business can deregister at any time if taxable sales in the next 12 months are expected to be less than £83,000 – see Voluntary deregistration opportunity.

- The date of deregistration is based on the date when the application is received by HMRC or a later date and not on a retrospective basis – see Date of deregistration.

Share the VAT saving

I deregistered some of my private clients at the end of March, mainly because of the flat rate scheme changes, and the tip I gave them was to try and share the 20% VAT saving on sales with those clients who could not claim input tax (such as those of Bill and Ben in the example) by proposing a 10% increase in their fees. This increase recognised the loss of input tax and flat rate scheme windfalls for my clients, which obviously end when a business deregisters. I was surprised that some clients did not appreciate the fact that many businesses cannot claim input tax, such as those trading below the registration threshold or making exempt supplies. The main customer for one of my clients was an undertaker and she had no idea that her 20% VAT charge was a cost to the undertaker and not recoverable as input tax.

Flat rate scheme

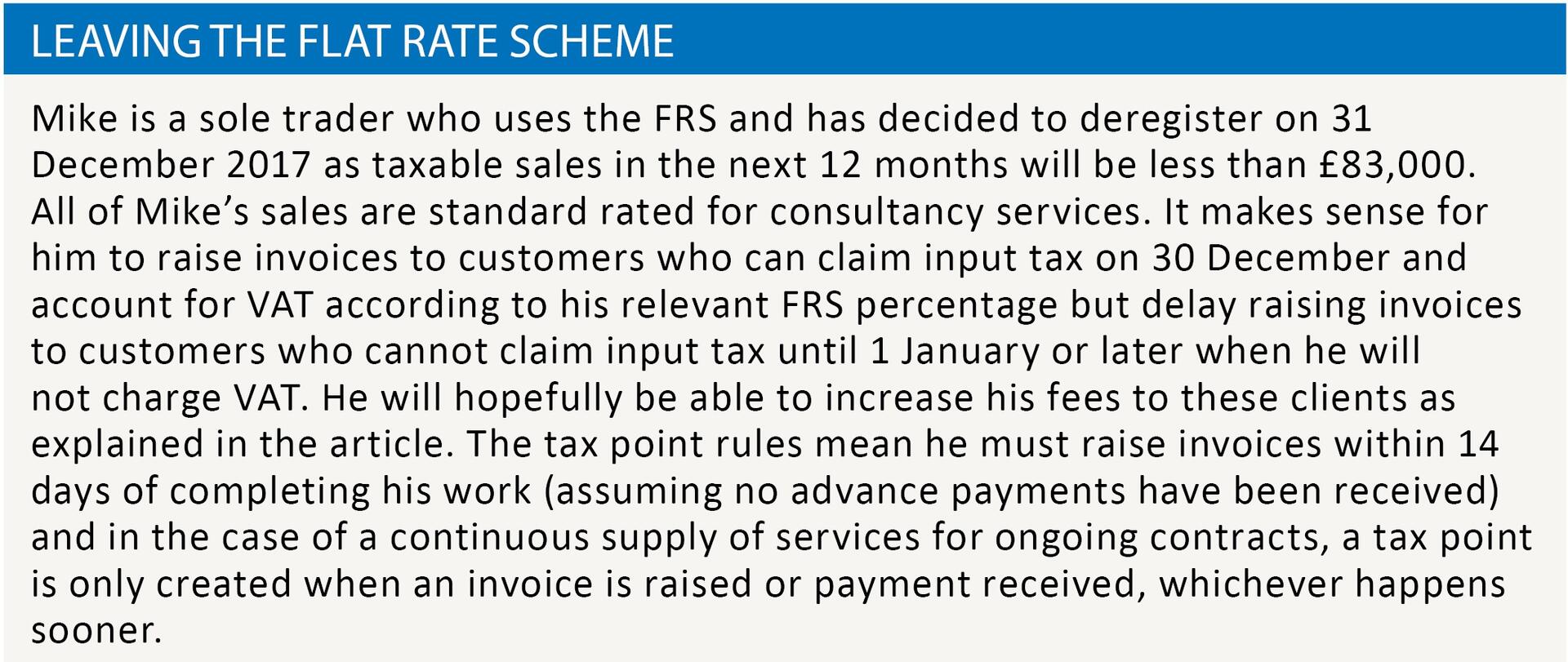

There is a quirk with the FRS rules and deregistration: when a scheme user deregisters, he is deemed to be leaving the scheme on the day before he deregisters (HMRC Notice 733, para 12.4). See Leaving the flat rate scheme.

Here is another twist: it makes sense for Mike in the example to encourage suppliers to invoice his business on 31 December rather than an earlier date. This is because he can claim input tax on these costs because he left the FRS on the previous day. However, the downside is that output tax will be due at 20% on any stock and assets caught by the valuation rules (see next section) as the key date is his deregistration date i.e. 31 December.

Output tax on assets and stock

A business must pay output tax on any standard rated stock and assets it owns at the time of deregistration. The relevant figure is the market value of the asset, so the calculations take into account wear and tear, obsolescence and damage to the items in question. However, the good news is that a lot of items can be omitted. And output tax is only payable if the total market value of the items that remain is more than £5,000 (i.e. VAT payable exceeds £1,000). Here are the basic rules:

- Stock and assets are excluded if no input tax was claimed when they were purchased e.g. a computer bought from a friend or supplier who was not VAT registered.

- There is no output tax to pay on zero-rated or exempt items e.g. most food stock for a restaurant or a motor car where input tax was blocked on purchase (the latter is VAT exempt by VATA1994, Sch 9, Group 14).

- Output tax is declared on the final VAT return on all relevant stock and assets if the £5,000 limit is exceeded i.e. not just the value above £5,000. So if the total value of relevant assets is £6,000, output tax of £1,200 will be due rather than £200.

Cash accounting scheme

If a business uses the cash accounting scheme, it only accounts for output tax or claims input tax when payments have been made to suppliers or received from customers. However, the final VAT return before deregistration must be completed on the basis of debtor and creditor accounting. This makes sense because it is the last chance to account for output tax and claim input tax on sales and purchase invoices raised by the business while it is a member of the VAT club. (HMRC Notice 731, para 6.12).

Post deregistration expenses and bad debts

If a business deregisters and then subsequently receives purchase invoices that relate to its period of registration, there is scope to reclaim VAT by sending form VAT427 to HMRC along with original purchase invoices. Claims will usually relate to services e.g. accountancy fees. The form can also be used to claim bad debt relief if some of the debtors on which the business accounted for output tax while it was registered subsequently go bad.

Reference: HMRC Notice 700/11, section 9.

Compulsory deregistration

I have so far considered the rules for voluntary deregistration, where advisers need to be proactive to identify the most suitable date for leaving the VAT club. However, there are situations when a business must deregister on a compulsory basis:

- It has ceased to trade and has no intention of making future taxable sales

- The business has been sold

- A business joins a VAT group (or a VAT group is disbanded)

- The legal status of the business changes e.g. a sole trader incorporates his business

- A farming business decides to join the agricultural Flat Rate Scheme (VAT Notice 700/11, para 2.7).

In the case of legal entity changes or business sales, the new owner can retain the VAT number of the previous owner if both parties agree. The process is straightforward (form VAT 68 is completed and signed by both parties) but the main disadvantage is that the buyer takes over the VAT liabilities and potential VAT errors of the seller for the last four years. So it is usually wise for the buyer to start with a clean slate and a new VAT number.

Missing traders

As a final tip, always ensure that your clients amend their online details with HMRC if they change address or move to new premises. I have heard about situations where HMRC tried to contact a business without success (returned post etc), so they put a block on the business being able to submit returns online. In one extreme case, where the business was also behind on submitting and paying its returns, they deregistered the business. This was a big shock for the business owner, who happily carried on issuing sales invoices and charging VAT and the problem only came to light a couple of years later when he tried to sort out his VAT affairs!