The devil in the detail

Share this article

Peter Stoddart details the new Structures and Buildings Allowance announced in Budget 2018 and what was learnt from recent consultations with HMRC on the new allowance

Key Points

What is the issue?

A new form of capital allowance was announced in Budget 2018 and the subsequent Financial Bill. Grant Thornton have met with HMRC and the Treasury to discuss key aspects of the proposed changes and have reviewed the draft legislation.

What does it mean for me?

Capital allowances are changing; a brand new form of allowances creates exciting opportunities for taxpayers but, as always, the devil is in the detail and the new allowance needs to be considered carefully.

What can I take away?

Taxpayers and advisers alike need to understand the changes to the capital allowances regime and the opportunities and the hurdles it presents to future claims to ensure no valuable tax savings are missed.

Capital allowances (CAs) have enjoyed a number of years of relative consistency without any landmark changes. In Budget 2017, the main change was to make enhanced capital allowances (ECAs) available on vehicle charge points. Now not only will most ECAs be scrapped, a new capital allowance has been announced in one of the more significant changes in the history of the capital allowances regime.

Now more than ever before, there are big opportunities for UK taxpayers to claim more tax savings by carefully considering the CAs available on commercial construction projects. The key is to consider the new capital allowances regime early to ensure opportunities to optimise tax savings are not lost.

Background

Autumn Budget 2018 was highly anticipated as it was the first following the publication of the Office of Tax Simplification (OTS) review of the CAs regime in June 2018. The OTS report considered whether CAs should be replaced by accounting depreciation following feedback from previous OTS consultations where respondents highlighted CAs as a complex system.

The OTS report ultimately found that CAs are too imbedded in the UK tax system for the benefits of replacing them with depreciation to outweigh the upheaval such a replacement would cause. Nonetheless, the OTS recommended simplification of the CA regime as well as extending the scope of assets which qualify for inclusion within the Annual Investment Allowance (AIA) threshold, which would simplify claiming CAs for SMEs.

So although CAs are here to stay, the OTS’s calls for simplification have been clearly heard in Whitehall and have led to the biggest announcement in the Autumn Budget 2018 with the new form of capital allowance called the Structures and Buildings Allowance (SBA).

The Structures and Buildings Allowance: an overview

The headline is that SBA will allow a taxpayer to claim eligible capital expenditure on non-residential construction projects, including new build, refurbishments and fit-outs, as a 2% straight line deduction claimable over 50 years. Tax payers do need to hold an interest in land, as with the case on fixtures claimed as plant and machinery allowances. SBA will not be available on land, dwellings or planning permission.

The SBA has been introduced to correct what HMRC has perceived as a long-term distortion in the UK capital allowances regime which, unlike other tax jurisdictions, does not allow a tax relief for buildings or structures. Further, HMRC considers SBA provides additional support to UK businesses and expects the new allowance to increase business investment.

The timeline for SBA has been that there was an initial consultation, which closed on 31 January 2018. The draft legislation was released on 13 March 2018, alongside Philip Hammond’s spring statement. A new consultation on this draft legislation has now been launched until 24 April 2019, with the final SBA legislation expected to be introduced by a Statutory Instrument in May 2019, with an eventual plan for amalgamation into the primary Capital Allowances Act 2001.

The SBA is great news for taxpayers as previously ‘non-qualifying’ expenditure on buildings and structures can now be claimed for tax relief. However, the SBA comes with its own complexities.

Firstly, SBA is only available for projects where the related contract has been entered into on or after 29 October 2018. Any contract entered into before this date will not be eligible for SBA, even if the project expenditure is incurred after this date. The draft legislation sets out further that any contract for any works carried out in preparation of the construction works will also mean the project will not qualify for SBA. Grant Thornton are raising with HMRC whether this will include architect or professional fees or if this rule applies only to physical site works.

HMRC also detailed during consultation that there will be stringent evidence requirements in order to claim SBA. Within the draft legislation, this is known as the ‘allowance statement requirement’. This requirement needs to be met, and an ‘allowance statement’ completed, for each construction project upon which a taxpayer wishes to claim SBA. Without meeting this requirement, no SBA will be able to claimed either by the original constructor of the building or structure and any future owners. The requirement will also have to be met by a UK taxpayer when they acquire property overseas and wish to claim SBA.

The allowance statement needs to be a tangible written statement that includes the date of the construction contract, the amount of qualifying SBA expenditure on the construction project or purchase and the date the building was brought into use. HMRC have added a further section setting out that they may revise the allowance statement requirements in future to stipulate other information also has to be included.

We also discussed with HMRC the definition of ‘Buildings’ and ‘Structures’ for the purposes of SBA, and whether they would mirror the current definitions for plant and machinery allowances (PMA) purposes as Capital Allowances Act (CAA) 2001 s22 and s23. HMRC have said the definition will not be the same but will draw from the existing legislation and will be similar. However, within the draft legislation the definition of these terms are not clearly defined as with PMA. During consultation, HMRC seemingly confirmed expenditure on concreting a yard and paths or roads as well as expenditure on a building as part of a project could qualify for SBA. We will be raising this issue with HMRC as to whether there will be a future alteration to the draft legislation to define ‘Buildings’ and ‘Structures’ for the purposes of SBA.

Excluded expenditure

Expenditure on the acquisition of land, including SDLT, or on obtaining planning permission for the project will be considered ‘excluded expenditure’ for the purposes of SBA.

Further, expenditure on a building or structure for ‘residential use’ will also not qualify for SBA. The draft legislation states this will include dwelling houses, student accommodation, army barracks or armed forces accommodation, prisons or retirement home facilities. The draft legislation clearly states that accommodation for persons in need of personal care by reason of old age, disability or alcohol/drug dependencies, such as care homes or medical facilities, will not be considered to be residential use buildings for the purposes of SBA.

Shared areas used for both dwelling and commercial purposes will also not qualify for relief. Where a building is divided into residential and non-residential areas, an apportionment of the expenditure may qualify for SBA.

During the consultation with HMRC, we have stressed that the continued consideration of student accommodation facilities as residential dwellings is rather unfair.

For instance, hotels and care homes are not considered dwellings, in accordance with HMRC guidance and now the draft SBA legislation, and capital allowances are available on these buildings. However, student accommodation are considered residential buildings, upon which capital allowances including SBA are heavily restricted. We will raise this point again with HMRC during this latest round of consultation but do not expect this to change.

Leases

There are also rules around the granting of leases and whether SBA can be claimed by a Lessor or a Lessee. Both can claim SBA for qualifying construction expenditure that they incur on the same property. The situation becomes more complex where there is a granting of a lease that is ‘substantially no different from a purchase of the interest in land’.

Within the draft legislation there is a set of tests to determine whether the SBA remains with the Lessor or transfers to the Lessee.

We understand that if a Lessee incurs more than 75% of the value of the lease plus the value of the retained interest of the Lessor and the lease is greater than 35 years, the right to claim SBA on the building will pass from Lessor to Lessee. If the 75% test or the 35-year test is not met, the Lessor retains the right to claim SBA on the property.

Other key SBA points

SBA expenditure will not be eligible to be claimed as part of the Annual Investment Allowance (AIA) which will still only be available for qualifying expenditure claimed as plant and machinery allowances (PMA).

There will be an interaction between SBA and capital gains tax (CGT) where the CGT base cost is lowered by the amount of the SBA claimed. This essentially will result in a full or partial claw back of the SBA claimed.

There will be no disposal adjustments where SBA is claimed, a purchaser of a building or structure subject to an SBA claim will simply inherit the Seller’s position and continue claiming the 2% straight line relief.

The original technical guidance also detailed ‘use and disuse’ provisions for SBA. If a building upon which SBA had been claimed was not used by a business for their qualifying activity, due to inactivity, market conditions or damage, SBA would cease to be available until it was brought back into use. During consultation, we raised the fact that the use and disuse provisions were unfair, as no taxpayer, whether they are occupiers or investors, wants a building they have constructed to be sat empty. HMRC have seemingly taken this on board, as the draft legislation has removed this aspect. There will still be a disclaiming of allowances on demolished properties however.

The new capital allowances regime

The SBA represents a huge change to the existing capital allowances regime and presents a number of opportunities, particularly in considering how best to claim tax relief on construction projects alongside other forms of capital and revenue expenditure incentives.

Since SBA was announced, Grant Thornton have carried out studies on example construction projects, assuming the scenario that expenditure on ‘buildings’ and ‘structures’ could qualify for SBA.

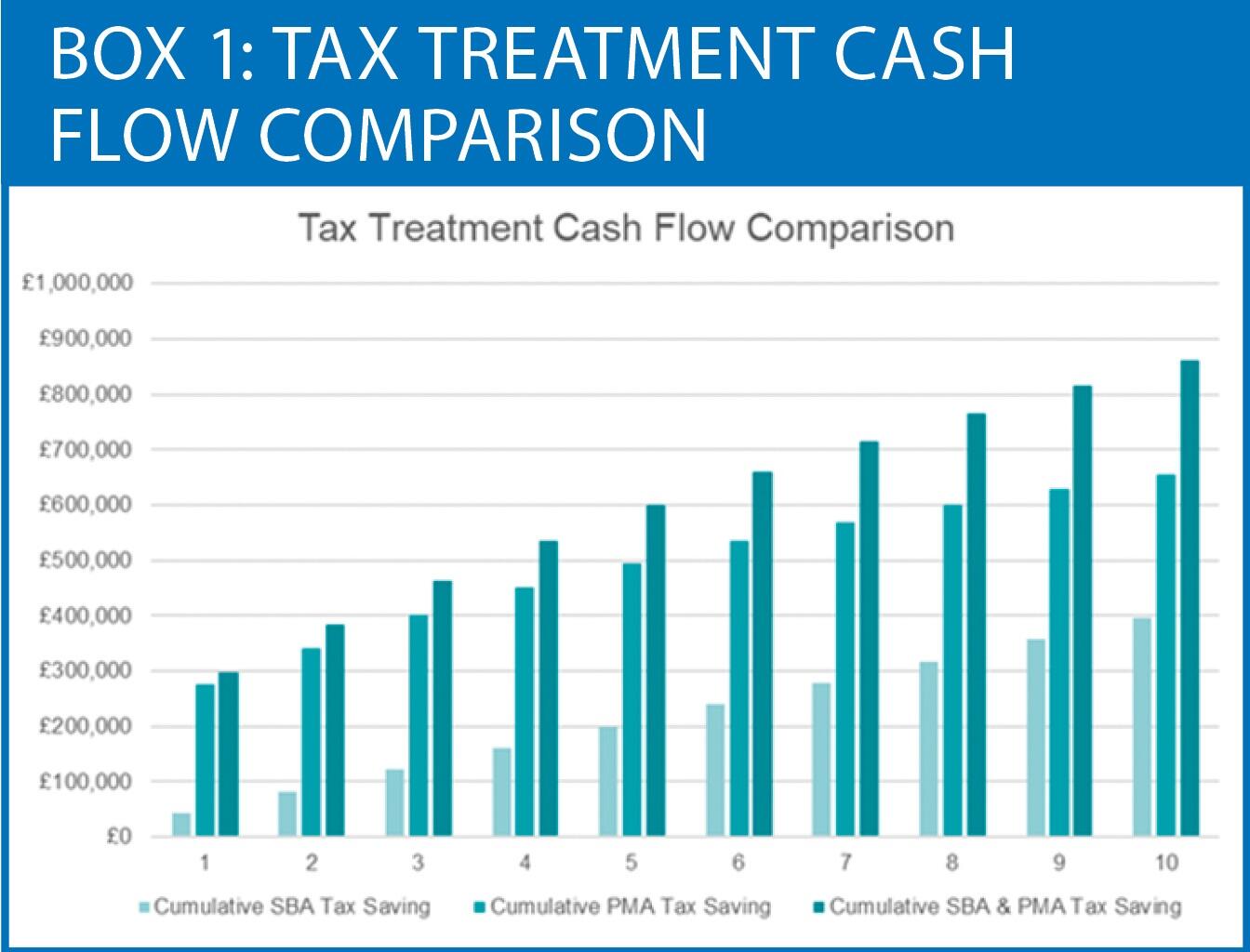

For instance, in an office construction project a typical PMA analysis could identify £5.5m of PMA against say £11.5m of total construction costs. The balance of £6m would be treated as ‘non-qualifying’ for PMA purposes. PMA alone would provide an estimated tax saving of £940,000 over time, based on the 19%/17% corporate tax rates.

However, where the £6m ‘non-qualifying’ expenditure is instead allocated to SBA and claimed alongside PMA, that potential tax saving increases substantially to £1.96m over 50 years, based on a 19%/17% corporate tax rates. The difference between claiming PMA only or SBA and PMA on this example project is displayed in the cash flow graph, showing estimated tax savings over a ten-year period. See box 1.

This is only one example but it highlights the opportunities available in the new capital allowances regime, which includes SBA. There are a number of considerations that need to be made before considering an SBA claim. Take for example our sample office project above. A freehold investor developer would likely sell the property in the medium to long term, which could result in a CGT charge where a gain is realised and the SBA would be clawed back.

This article and our studies are based on the SBA technical note, our consultation with HMRC and the current draft SBA legislation. The current consultation with HMRC on the draft legislation runs until 24 April 2019. We will be involved in this consultation, raising the challenges highlighted in this article and look forward to discussing SBA opportunities with our clients once the Statutory Instrument for SBA is released this summer.