A digital single window

Share this article

Daisy Ogembo considers the taxation of platform workers and the viability of an EU digital single window for income data

Key Points

What is the issue?

Platform work includes localised gig work, such as taxi and food delivery services provided through platforms like Uber and Deliveroo, as well as web-based platform work such as graphic design and data entry through platforms like Fiverr and Upwork.

What does it mean for me?

Income earned through gig platforms, letting platforms and other digital intermediaries presents new challenges for taxation. There is a real risk that a significant amount of platform work is not fully taxed, and that platform workers are not adequately covered by social security systems.

What can I take away?

This article discusses the challenges connected with the taxation of web-based services and assesses the viability of the national initiatives of Denmark, Estonia and France to obtain data on platform users’ earnings directly from platform companies into an EU-level ‘digital single window’.

Platform work has been defined by EU-OSHA, the European Agency for Health and Safety at Work, as ‘all labour provided through, on, or mediated by platforms, and which features a wide array of standard and non-standard working arrangements/relationships’ (see bit.ly/3f66gAZ). The Cambridge Dictionary defines ‘gig-economy’ as ‘a way of working that is based on people having temporary jobs or doing separate pieces of work, each paid separately, rather than working for an employer’. Platform work includes localised gig work, such as taxi and food delivery services provided through platforms like Uber and Deliveroo, as well as web-based platform work such as graphic design and data entry through platforms like Fiverr and Upwork.

It is difficult to estimate the size of the platform economy for various reasons, including the fact that it is often a source of secondary income and the income earned is not consistently reported to tax authorities. According to some estimates, the gig economy – comprising crowd funding, asset sharing, transport, on-demand household services and on-demand professional services – in the European Union alone generated €3.6 billion in revenue in 2015, while online outsourcing was projected to grow to $4.8 billion in 2016 (see bit.ly/39Ap0HH).

Taxation and social security protection challenges

There is a real risk that a significant amount of platform work is not fully taxed, and that platform workers are not adequately covered by social security systems, with future adverse consequences both to individuals and public finances. Part of the difficulty in taxing and extending social security coverage to platform workers stems from their employment status. In most, but not all, instances, platform workers are classified as self-employed contractors. (For the purposes of this article, I assume that the vast majority of platform workers are regarded as self-employed under the law.

However, this assumption is limited because of the diversity of employment categories in various countries.) The self-employed tend to be significantly less tax compliant than employees whose salaries and wages are subject to an employer withholding scheme, a fact that is well-documented in tax evasion literature. Employees are more likely to be liable for a higher level of security costs (with entitlement to higher benefits) than self-employed individuals – although this varies by country.

Non-compliance by the self-employed is often a result of a combination of factors, including high compliance costs and inadvertent underreporting. The self-employed often have little tax knowledge, struggle to navigate complex compliance rules, and may not be able to afford compliance costs such as the cost of a qualified accountant or tax advisor. They also have an increased opportunity for outright evasion because they can more easily under-declare their income, exaggerate their deductible expenses, or operate wholly in the shadow economy.

In addition to these general challenges, tax and social security compliance by platform workers is complicated by the fact that they are often involved in multiple simultaneous engagements, possibly on different terms, and therefore may have different employment statuses even within one country.

Platform workers can, moreover, provide their services in multiple jurisdictions, thereby earning income that may be taxable in more than one state, and subject to different rules on deductibility of expenses in those jurisdictions.

A further complication arises when one attempts to apply a progressive income tax to platform income earners, even within a jurisdiction, and more so across borders. Finally, in the EU, these complexities are compounded by the fact that the companies operating the platforms are often based outside the Union.

Thus, the proliferation of platform work and other types of platform income pose significant revenue mobilisation challenges for tax and social contribution agencies and, if improperly managed, could contribute to an increase in the shadow economy. Non-compliance could also result in an unfair competitive advantage for firms utilising platform work and platform-based models of providing accommodation and other services. Moreover, ‘[i]f a sizeable segment of the population does not pay social contributions or insurance and underpays on tax and pensions, this will eventually negatively impact the ability of national social protection systems to provide public goods and social benefits, while the demand for those benefits will increase’ (see bit.ly/3jP6xvr).

Viability of an EU-level reporting system

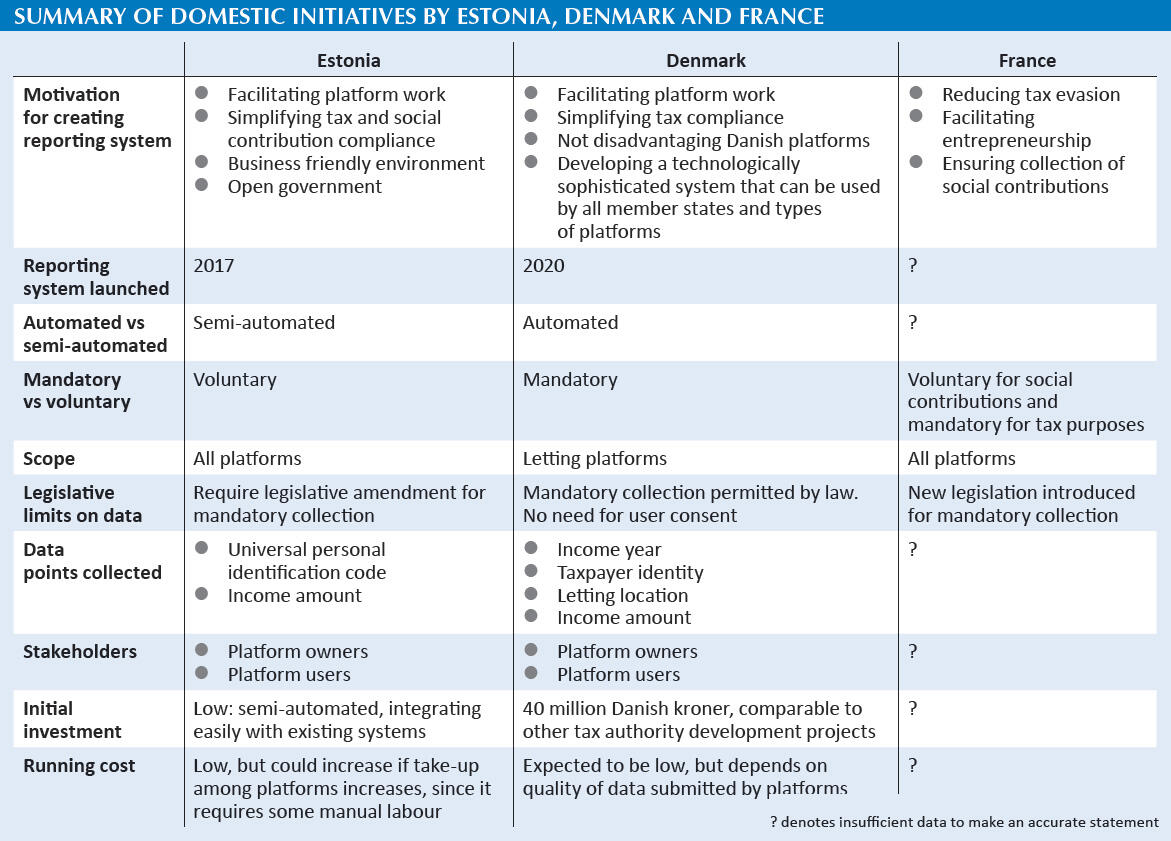

To address these challenges, some EU member states have embarked on domestic initiatives to obtain data on platform users’ earnings directly from the platform companies. For instance, Denmark’s Ministry of Taxation (SKAT) is developing an application programming interface (API) through which platforms can report data directly into its systems – a technologically sophisticated mandatory automated income reporting system, the technology of which could be later shared with other member states.

Estonia operates a voluntary semi-automated system whereby platforms share income data with the tax agency (ECTB) digitally via email. Unlike the Danish fully automated system that has only been tested in pilot projects, the Estonian semi-automated system has been operational since 2017. In France, the data reporting system has only just been legislated but the aims of its new legislation appear ambiti ous and cover taxation as well as social security coverage of platform workers. Other EU member states have also taken steps in this direction; for instance, the Office of Tax Simplification has recommended that government should consider plans in the UK for a potential ‘system equivalent to PAYE for self-employed platform workers (without aff ecting their employment status)’ (see bit.ly/3jQgf0H). Its October 2019 report on ‘Reporting and paying tax’ looked in more detail at the opportunity to help self-employed people through third party reporting (see bit.ly/3fQkIxg).

Are there benefits of scaling up existing domestic initiatives such as those in Estonia, Denmark and France, and developing not only common rules, but an EU-wide income reporting system (a ‘digital single window’)? There are good arguments in favour of doing so. First, collecting income data from foreign platforms without a registered presence or permanent establishment in the country is likely to be a significant hurdle for all the member states. With a digital single window, member states can pool their power and clout to exert pressure on foreign platforms to comply with an EU-wide requirement.

Second, developing a sophisticated automated API-based reporting solution that presents low compliance and maintenance costs is an expensive venture. While the cost and technology may be within the reach of higher income-earning member states like Denmark, it may not be easily affordable or accessible for some other member states. A digital single window would allow member states to pool their financial and technical resources for a more cost-eff ective system.

Third, some countries are already at advanced stages of designing different income reporting systems and it is likely that other member states will begin similar initiatives. While this approach may not pose a challenge for platforms that operate only domestically, a digital single window would benefit platforms that operate cross-jurisdictionally by saving them from having to use and comply with 28 different reporting systems. Further, a lower compliance cost could encourage the growth of smaller domestic platforms and nudge them towards expanding to other member states without experiencing higher compliance costs. This growth and expansion would benefit innovation in Europe.

In recent developments, on 3 July 2020, the OECD published a document containing model rules that interested jurisdictions can adopt to ‘collect information on transactions and income realised by platform sellers, in order to contain the proliferation of different domestic reporting requirements and to facilitate the automatic exchange agreements between such interested jurisdictions’ (see bit.ly/307t7Yn).

These model rules seem to be geared towards creating a ‘network model’ where member states collect data from web-based platforms having a permanent establishment or registered office in their jurisdiction and share that data with other member states whose taxpayers use the platforms but do not have such a permanent establishment or registered office.

A more ambitious approach that would address some of the limitations of a network model could be a ‘hub and spoke’ style digital single window for income data reporting, so termed because its topology resembles a cartwheel. In this set-up, member states would nominate a central agency (the ‘hub’) to receive income data from all the platforms with users in the member states and forward it to national tax and social security agencies (the ‘spokes’), in whatever form they require. Such a model is currently unprecedented in the EU when it comes to taxation.

However, admittedly, there are significant barriers to achieving such an ambitious system in the EU. The most significant barrier remains the lack of harmonisation of income taxation and social security systems in the Union and the fact that income taxation is not an EU competence. Further, if taxpayers’ data are being shared more widely or stored more centrally, there is a risk of more frequent or more serious data breaches.

The most workable avenue for the time being may be for each member state to continue developing its own solutions.

In time, some data sharing resembling a network model is likely to develop spontaneously between competent authorities under the auspices of existing data sharing arrangements, such as the mandatory Automatic Exchange of Information scheme. Initiatives such as the new OECD Model Rules for Reporting by Platform Operators with respect to Sellers in the Sharing and Gig Economy will help to drive this forward.

While a hub-and-spoke digital single window would allow the pooling of resources and clout and could simplify compliance, it would require the creation of a new legal basis in EU law – a more distant prospect. It may also be that the network model would eventually lead to a member state serving as a hub, a scenario that may only require amendments to existing tax co-operation and information sharing arrangements rather than new EU legislation.

A longer version of this article was first published in the British Tax Review as Daisy Ogembo and Vili Lehdonvirta, ‘Taxing Earnings from the Platform Economy: An EU Digital Single Window for Income Data?’ [2020] BTR 82. This research has received financial support from EaSI (2014-2020).