A donation for VAT purposes: no-strings attached giving

Share this article

What conditions need to be met to ensure that a donation will not be subject to VAT?

Key Points

What is the issue?

Income earned by a charity or other organisation is outside the scope of VAT if it relates to a genuine donation. It is also ignored as far as the VAT registration threshold is concerned. However, there can sometimes be areas of doubt when a close examination of a contract or agreement will be necessary to establish the correct VAT position.

What does it mean for me?

HMRC has the power to correct VAT errors going back four years, so it is important to ensure that records and supporting documents are kept to prove that a payment is a genuine donation. An acknowledgement of the donation on a website or annual report is not a benefit to the donor and can be ignored as being a possible supply of advertising or sponsorship.

What can I take away?

HMRC accepts in its guidance that some arrangements could be a part donation and part sponsorship arrangement. In such cases, the value of the sponsorship should be clearly determined based on the value of the benefits being provided to the sponsor and output tax apportioned on a fair and reasonable basis.

There’s an old saying that ‘there’s no such thing as a free lunch.’ Fortunately, that is not always the case, and charities receive sizable no-strings attached donations from many benefactors and supporters. But sometimes a donation is not really a donation: ‘I’ll give you £1,000 as long as you agree to… etc.’

As far as the nation’s favourite tax is concerned, we all know that there is no VAT payable on a genuine donation received by a charity or other organisation. It is outside the scope of VAT because there is neither a supply of goods nor services taking place. And the income is excluded from the Box 6 ‘outputs’ figure on the recipient’s VAT returns, assuming they are registered of course.

However, there can sometimes be grey areas on this issue: what exactly is a donation and might it be subject to VAT in some cases?

Are goods or services being supplied?

A number of years ago, an environmental charity I acted for was challenged by HMRC about the VAT liability of donations it received from its supporters. For each £10 payment paid to the charity, it would plant a tree in Scotland. The officer claimed that the £10 payments were standard rated because they related to the planting of trees – a standard rated activity.

In my view, this situation had no ‘fifty shades of grey’ about it. The donor had no idea where – or even if – the trees were being planted and certainly did not gain any personal benefit from the payment; it was not as if the trees were being planted in their back garden. The payments were outside the scope of VAT and not subject to output tax. This tale had a happy ending, with the officer accepting this outcome.

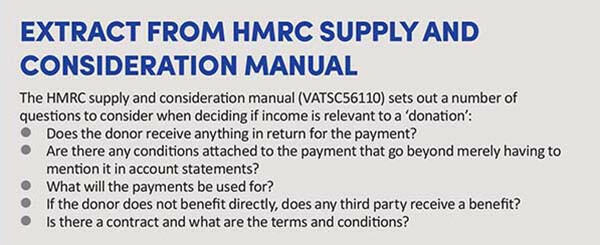

The starting point is to consider the helpful checklist produced by HMRC, where five important questions need to be considered for each arrangement. See Extract from HMRC supply and consideration manual.

Image

Case law examples

The HMRC guidance refers to a historic European Court of Justice case, which I always find amusing. To cut to the chase, the Dutch tax authorities assessed Mr Tolsma (Case C-16/93) for output tax on money he collected from passers-by on a public highway for entertaining them with his barrel organ. You can hopefully picture the scene.

The ECJ ruled in favour of the taxpayer, on the basis that the payments did not constitute a supply of services carried out for a consideration. There was no contract or agreement in place between any parties and the payments from the passers-by were voluntary donations. Hurrah!

In the case of European Commission v Austria (Case C-51/18), the CJEU considered the following arrangement:

- An artist sold a painting to a buyer.

- The buyer resold the painting in the future, and the artist was entitled to a royalty payment based on the resale value. The artist had no control in how much royalty he received.

- The Austrian tax authorities said that the royalty payment to the artist was subject to VAT but the European Commission disagreed as there was no supply of goods or services made by the artist. His only taxable supply had been made when he sold the painting.

The CJEU considered Article 2(1) of the Principal VAT Directive and ruled that a supply only existed where there was a ‘consideration’ that related to a legal relationship between the supplier and the customer which involved the supply of goods or services. There had to be a reciprocal performance, with the remuneration received by the supplier being linked to the value of goods or services supplied to the customer. In this situation, the royalty payment was to ensure the artist had a share of the ‘economic success of the original work of art’. This was different to a payment for goods or services.

Commission or donation?

The donation or supply challenge can also affect a commercial business. Imagine that you are an overworked tax adviser and don’t want to take on any new clients. However, you are keen to refer business leads to other advisers that you know will do a good job, which also encourages young businesses to prosper. One of the advisers that you recommend has kindly agreed to give you £500 for each successful lead, even though there is no obligation on her part to do this. Are the £500 payments subject to VAT, again assuming you are registered?

My view is that the payments are outside the scope of VAT because there is no legal or even verbal contract in place that defines the ‘consideration’ for this arrangement. The amount paid is totally out of your hands and wholly dependent on the generous response – or otherwise – of the adviser being given a lucrative client. The HMRC guidance I quoted above is very supportive of this conclusion in the opening sentence: ‘If a monetary donation is freely given, it is not consideration for any supply and so is outside the scope of VAT. In this situation, the donation has to be unconditional.’

Donor expectations

To share another tale, a local rugby club – VAT registered because of its healthy income from bar and gate receipts – received a generous £10,000 payment each year from a national retailer. It was described as a donation but the reality was that the retailer received an entitlement to buy the club’s allocation of international rugby tickets in return for its payment. The payment was not made in return for the tickets, only the right to buy them when they became available.

To be honest, I am not a fan of the oval ball but I understand that international rugby tickets at Twickenham are as popular as free beer at a stag party. The key question is as follows: if the retailer did not get the entitlement to the tickets, would they still make the annual payment? The answer is almost certainly ‘no’. Their expectation is that they will be able to buy rugby tickets, so the £10,000 payment should be standard rated. This scenario scores none out of five as far as the key questions in HMRC’s guidance is concerned.

Is it sponsorship?

To develop the arguments, there can sometimes be a fine dividing line between a donation and sponsorship arrangement.

For example, a number of years ago, a county cricket club charged members a fee of £120 for the member to have his or her name engraved on a brick outside the club’s pavilion, with the name of their favourite player at the club – past or present – also being included. In my view, the fee is standard rated because the member is getting a clear and worthwhile benefit for their payment. If the member’s name was spelt wrongly on the brick – or the wrong player was included – they would be justified in asking for a discount or refund because the ‘service’ they ordered has not been delivered.

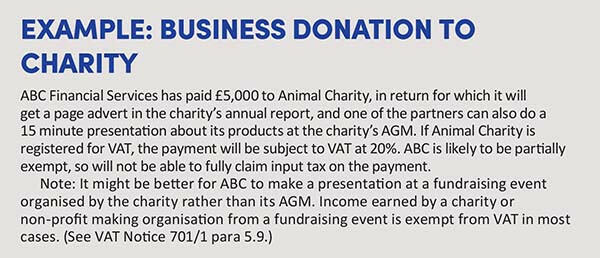

For another practical situation, see Example: Business donation to charity.

Note: there is further guidance in HMRC’s policy note VATSC03560 in its supply and consideration manual.

Image

Sponsorship and donation: dual purpose

HMRC updated its guidance a few years ago about when a payment to a charity could comprise two separate elements, with different VAT outcomes for each part. The updated guidance is contained in VAT Notice 701/41 para 2.3 and VAT Notice 701/1 para 5.9.6. The revised policy recognises that some charitable payments made by a business will consist of both a sponsorship benefit and a donation. For example, the £5,000 payment made by ABC in my example with Animal Charity might not be the going rate for sponsorship if only five people attend the charity’s AGM!

The challenge is to ensure that any donation is completely separate from any sponsorship agreement. Ideally, a business should make two separate payments to the charity and only the sponsorship payment will be subject to VAT. The agreement between the two parties should make this clear and the value of the sponsorship should accurately reflect the VATable benefits received from the charity.

Conclusion

Overall, there are key issues to consider, which will hopefully lead to the correct VAT outcome in most cases:

- What are the expectations of the payer when they part with their hard-earned cash? Do they expect to receive worthwhile benefits for their payment and not just, say, a token of appreciation on the recipient’s website?

- Is the phrase ‘donation’ correct? Be clear that the phrase ‘minimum donation’ is not a donation for VAT purposes and the phrase ‘suggested donation’ is only a donation if the word ‘suggested’ is what it says on the tin.