Electric vehicle company car schemes: the impact on employees and employers

Share this article

With the cost of living playing such a vital part in our decision making process, we explore the impact of electric vehicle company car schemes on both employees and employers.

Key Points

What is the issue?

The tax system is currently geared to offer a range of financial incentives intended to increase the take up of electric vehicles. As a result, employers are well placed to enable and accelerate the switch to electric vehicles, making a positive environmental impact and help to ease pressure on the cost of living.

What does it mean for me?

This article looks to unpick some of this complexity and shed light on how specific aspects of the tax system and electric vehicles could be used to further the UK government’s sustainability agenda.

What can I take away?

Currently, there is a very strong business case for making the move to electric. However, there will be challenges to overcome in future, especially as the government seeks to replace much needed revenue from tax on company cars, fuel duty and vehicle excise duty.

Transport is the biggest source of greenhouse gas emissions and accounts for 27% of the UK’s total emissions according to figures published by the Department for Business, Energy and Industrial Strategy. Based on the figures published, cars and taxis are responsible for 55% of the greenhouse gas emissions from transport. Switching to electric vehicles is an essential step on the UK Road to achieving Net Zero by 2050. In 2020, the government announced the end of the sale of new petrol and diesel cars by 2030, so it’s now a question of ‘when’ people will make the switch to an electric vehicle.

Currently, there remains a price premium for electric vehicles when compared with internal combustion engine alternatives. In some cases, the price premium for electric vehicles means they are out of reach for some households. Electric vehicle registrations are growing, with recent figures published by the Society of Motor Manufacturers and Traders showing that they accounted for one in five of new cars registered so far in 2022. However, with electric vehicles only accounting for around 3% of the cars on UK roads, there is a long way to go.

Company cars are typically cycled into the ‘used’ car market after three to four years of use. Over time, the volumes of used electric vehicles that are introduced into the company car market could help to increase the overall supply and reduce price, helping to make the move to electric vehicles a more affordable proposition for all.

The tax system is currently geared to offer a range of financial incentives intended to increase the take up of electric vehicles. As a result, employers are well placed to enable and accelerate the switch to electric vehicles, making a positive environmental impact and helping to ease pressure on the cost of living.

Introduction to company cars

In general, where an employee is provided with a non-cash benefit paid for by their employer, such as a company car, this is referred to as a benefit in kind. An employee will pay income tax at their marginal tax rate based on the value of the benefit in kind they receive, and the employer will also pay NICs based on the benefit in kind value.

For company cars, the benefit in kind value is broadly calculated based on the list price of the car in question, multiplied by a percentage (the ‘appropriate percentage’) that is determined by its CO2 emissions, fuel type and electric range. Income Tax (Earnings and Pensions Act (ITEPA) 2003 ss 121 to 144 cover the method for calculating a company car benefit in kind value.

The tax rules for company cars are designed to encourage the selection of cars with lower CO2 emissions. Opting for a lower emission car will result in a lower a benefit in kind value, meaning less income tax to pay for the employee, and less NICs for the employer. The appropriate percentage for a battery electric vehicle is currently frozen at 2% until 5 April 2025 and will rise to a maximum of 5% in the 2027/28 tax year. The sustained low rate offers a significant financial incentive to opt for a zero-emission car and it is likely to be the main factor for the increase in popularity of battery electric vehicles as company cars. The latest figures from HMRC estimate that battery electric vehicles will have accounted for 7% of the company cars reported in 2020/21, a sharp rise from less than 1% the year before.

At a high level, the tax rules appear to be relatively simple and offer an incentive to switch to electric vehicles. However, as with many things, the devil is in the detail. When you start to look at the wider considerations for electric vehicles, such as charging infrastructure, provision of electricity, expenses policies, reporting requirements, HMRC compliance, etc., things can get more complicated. This article looks to unpick some of this complexity and shed light on how specific aspects of the tax system and electric vehicles could be used to further the UK government’s sustainability agenda.

It is important to note that whilst this article focuses on the employment taxes impact of electric vehicles, there are also corporation tax and VAT implications for a business to consider in relation to providing company cars and associated benefits.

Job-need company cars

Job-need company cars are commonplace in some industries and are often provided to lower paid employees. Since an employee with a job-need company car will pay income tax on the benefit in kind value of the car they have to use for work, reducing this tax burden is likely to be well received.

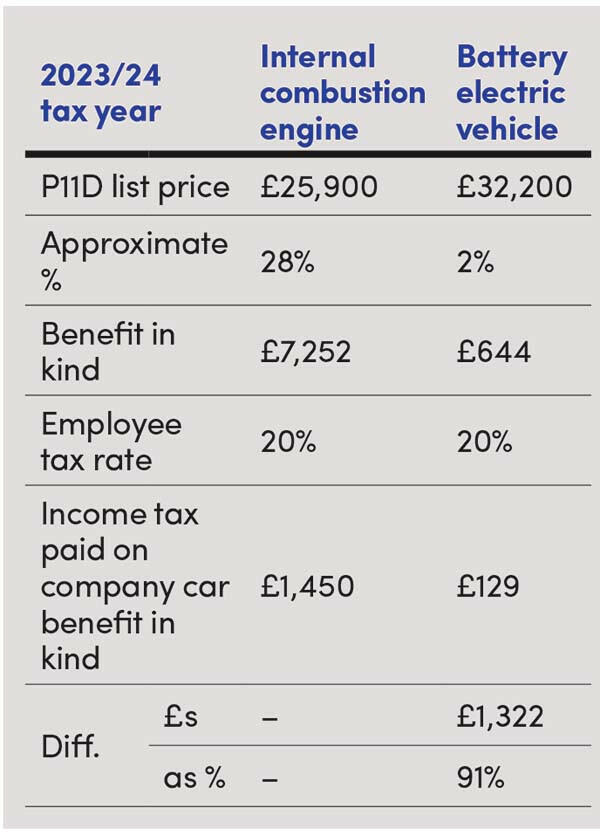

The example below demonstrates the impact of income tax costs for a basic rate taxpayer switching from a typical internal combustion engine company car to a comparable battery electric vehicle alternative. (Please note, the higher P11D list price for the battery electric vehicle is an example of the price premium that can apply for a comparable electric vehicle.)

This example shows that the employee would see a 91% drop in the amount of income tax paid on the company car benefit in kind. This change in income tax would equate to an increase in take home pay of around £110 per month.

Another way of looking at this position is that the switch to an electric vehicle would deliver the same financial impact for the employee as giving them a pay rise of almost £2,000 per annum. However, it is important for job-need employees to consider the financial impact of fuel and electricity costs incurred driving business mileage.

We explore this in more detail later in this article.

The financial benefit in this example is not just for the employee. A business would see the cost of employer NICs on the company car benefit in kind fall by £912 per annum. Across a fleet of 100 cars, this could generate annual employer NICs savings of around £91,000.

Cash or car schemes

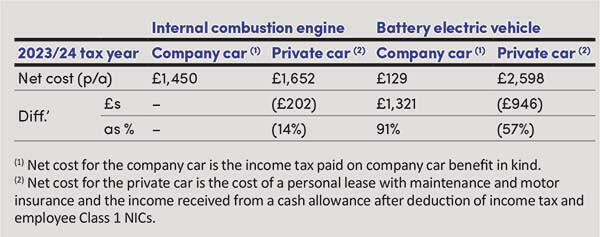

It is fairly common practice for employers to offer employees the choice of a company car or a cash allowance.

However, if an employee wants to make the switch to an electric vehicle and reduce their carbon footprint, opting for a cash allowance may not be the right move.

The example above demonstrates the financial impact for a basic rate taxpayer choosing between a comparable internal combustion engine car or a battery electric vehicle, with the cars provided as a company car or a private car funded with a cash allowance. Opting for a battery electric vehicle as a company car will offer the employee a significant saving when compared to a cash allowance.

As before, the financial benefit is not just for the employee. In this example, a business funding the battery electric vehicle company car would save at least 10% when compared to funding the internal combustion engine company car or cash allowance.

Where an employee has the choice of a company car or cash allowance, the Optional Remuneration Arrangement (OpRA) legislation comes into play. The OpRA legislation largely removes the income tax and NICs advantages of arrangements where an employee gives up the right to an amount of earnings in return for a benefit. The legislation works by calculating a benefit value based on the greater of the earnings given up, or the value based on normal benefit in kind rules. However, the OpRA legislation has an exemption for vehicles with emissions of 75g/km or less, which means it doesn’t apply to most electric vehicles (see ITEPA 2003 s 120A(3)(c)).

Salary sacrifice schemes

Traditional company car schemes are only open to a limited population of a company’s employees. However, introducing a salary sacrifice for an electric vehicle arrangement can allow an employer to open access to company cars to its entire workforce (subject to national minimum wage restrictions).

In a salary sacrifice, an employee agrees to a contractual reduction in their gross pay, and in return is provided with a fully insured and maintained electric vehicle as a company car. The employer saves on both the salary costs and the associated employer NICs thereon. These savings can be used to offset the costs of providing the car so the arrangement can be operated on a cost neutral basis or structured to deliver employer savings (if desired).

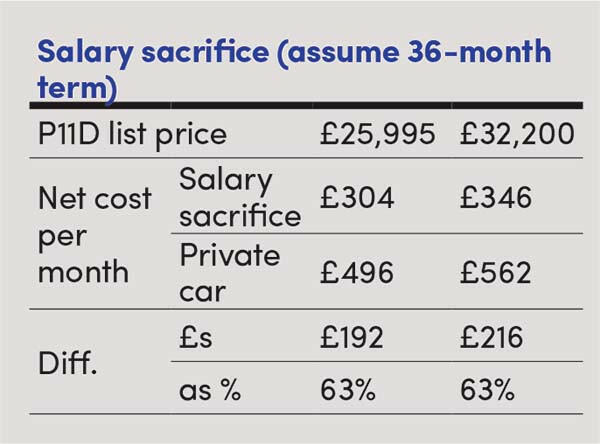

The following example demonstrates the financial impact for an employee of taking an electric vehicle via salary sacrifice when compared to funding the same car privately. (We have included the battery electric vehicle car used in the job-need calculation above as well as a lower cost alternative.)

The example shows that the employees could save up to 63% when opting for an electric vehicle via salary sacrifice compared to funding the same car privately.

While the monthly net costs for salary sacrifice represents a significant spend, the employee would get a brand new electric vehicle that is fully insured and maintained, leaving the cost of charging as their only other motoring outlay. If the employee only had the option of a private car, the much higher monthly costs might make the switch to an electric vehicle unaffordable.

It is worth noting that the example is based on a scheme designed to generate an employer saving as well, with 50% of the employer NICs saved on the sacrifice being retained by the business. Retaining some employer NICs is relatively common to offset some of the costs involved with operating the arrangement.

Given the potential benefits available, it is not surprising that in a recent Deloitte poll almost 70% of respondents said they were either considering the introduction of an electric vehicle salary sacrifice scheme or were in the process of implementing one. The respondents cited the opportunity to reduce carbon emissions (34%) and the ability to offer a new engaging employee benefit (33%) as the main drivers behind this decision.

Before making the decision to implement a salary sacrifice for an electric vehicle arrangement, it is important for an employer to evaluate the full range of implications to ensure that the proposed arrangement meets the needs of the business and its employees (both now and in the future). For example, a business may wish to consider the cost of implementation and ongoing operation, the range of benefits to offer, financial risks for the business and/or employees, finding the right provider, employment law impacts, etc.

Access to charging

A key element of the transition to electric vehicles will be ensuring convenient and cost-effective access to vehicle charging facilities. It is worth noting that with the cost of electricity on the rise, charging is becoming more expensive both to the employees and the employers. This may have an impact on the charging choices made, as well as the decision to switch to an electric vehicle.

Broadly speaking, access to charging falls into the following categories:

- residential;

- public (including on the go and destination charging); and

- workplace.

Access to charging is another area where an employer can play a role and leverage the incentives offered by the tax system, although there is some complexity with the rules.

Residential charging

Based on HMRC guidance (EIM23900), if an employer pays for a vehicle charging point to be installed at the employee’s home there is no taxable benefit where it is used for a company car. This is because the installation of a charge point would meet the conditions for ITEPA 2003 s 239 and no liability would arise for payments and benefits connected with company cars (which includes cars provided via a salary sacrifice arrangement). There would be a taxable benefit based on the cost to the employer if it was used for a private car.

HMRC guidance states that if an employer reimburses the cost of electricity used to charge an electric company car at home, the reimbursement should be taxed as earnings, with the employee being entitled to a deduction for the cost of business miles travelled. However, there is some uncertainty in relation to this guidance and whether ITEPA 2003 s 239 should also apply. If it does, the reimbursement for electricity would not trigger an income tax and NICs liability, regardless of whether it is for business or private use. This has been raised by CIOT in discussions with HMRC so we may expect a clarification to the published guidance in the future.

Public charging

The cost associated with public charging is only likely to be the cost of electricity used and any provider subscription fees. Based on HMRC guidance, if an employer meets these costs for an employee with a company car, ITEPA 2003 s 239 should apply and no liability would arise. As before, the exemption only applies to company cars and so this would be a taxable benefit based on the cost to the employer in a private car.

Workplace charging

The provision of workplace charging for employees with a company car meets the conditions for ITEPA 2003 s 239 to apply and so no taxable benefit should arise for the provision of charge points and the electricity provided. Since 6 April 2018, a similar exemption for workplace charging of private cars has been in place to cover charging facilities which includes the provision of electricity (see ITEPA 2003 s 237A). The exemption applies on the condition that the facilities are made available generally to the employer’s employees at that workplace.

We are seeing more employers help their employees make the move to electric vehicles. The employer provision of access to charging facilities and electricity can help to reduce the financial burden for employees and the tax system provides a mechanism to help.

Electricity costs

The wholesale price of electricity has risen sharply, such that the government felt it was necessary to introduce the energy price guarantee. This effectively caps the cost of residential electricity until April 2023, with a review planned in the meantime to determine how best to help households after the guarantee ends. The result of this is that the cost per mile for electricity has risen from around 5p-8p at this point last year, to around 10p-14p now (assuming an electricity price at the 34p/kWh energy price guarantee).

While this has removed some of the financial benefits of switching to an electric vehicle, charging at home can still offer a cheaper cost per mile than petrol or diesel. However, if an employee can only charge in public, often where electricity costs are much higher, then the cost per mile of using an electric vehicle could be higher than a petrol or diesel car.

A key challenge for employers is setting a policy for reimbursing business mileage in electric vehicles. The HMRC advisory electric rate is set to rise from 5p to 8p per mile on 1 December. Despite the increase, some employees undertaking business mileage in an electric vehicle may still be significantly out of pocket when reimbursed at this rate. As with fuel, employers can opt to reimburse employees based on the actual cost incurred to ensure they aren’t left out of pocket. However, when you look at what is needed to measure and track electricity from home and public charge points, and the interaction of workplace charging, care needs to be taken to implement this in a way that is aligned with HMRC guidance.

The Autumn Statement

In the Autumn Statement, the government announced the rates affecting company cars for three further tax years (with rates now known up to 5 April 2028). The extension of the low rates for EVs will give greater certainty and a longer-term financial incentive to help boost the take up of EVs. However, it is important to note that the government also announced that EVs will begin to pay vehicle excise duty in the same way as petrol and diesel cars from 1 April 2025. The change to VED will reduce some of the financial incentive currently available for people making the move to an EV.

Looking ahead to the future

Currently, there is a very strong business case for making the move to electric, with significant environmental and financial benefits. The design of the tax system means employers are uniquely placed to enable and accelerate the switch to electric vehicles, and in some cases make it a financially viable option that otherwise would not be open to some employees.

A key factor enabling the move is the financial incentive offered by the tax system. However, there will be challenges to overcome, especially as the government may seek to replace much needed revenue from tax on company cars, fuel duty and vehicle excise duty as more people make the switch to electric vehicles.