The Employer of Record model: employment tax considerations

Share this article

We consider the increasing use of the Employer of Record model, and the importance of understanding and managing UK employment tax obligations.

Key Points

What is the issue?

There is concern that organisations are failing to consider the potential continued UK employment tax consequences for business travellers to the UK who are engaged via an Employer of Record (EOR) model.

What does it mean to me?

Even when using an EOR model, the organisation retains crucial employment tax responsibilities for business travellers. Failure to understand and meet these obligations can result in PAYE failure with associated consequences of being charged interest and potentially penalties.

What can I take away?

Organisations must ensure that there are robust monitoring processes in place with regards to identifying continuing UK employment tax obligations for EOR engaged business travellers.

We are operating in a world where attracting and retaining talent is a challenge that all organisations are facing, with workers seeking roles that give them the flexibility to work when and where they choose, while organisations also seek the candidate with the right skills to fill their role from the global talent market.

This is driving the need for organisations to consider a suite of engagement models when hiring individuals, including the Employer of Record (EOR) model.

In this article, we’ll explain what the EOR model is and then focus on the continuing UK employment tax compliance obligations for organisations utilising an EOR – which many are at risk of failing to consider.

What is an Employer of Record?

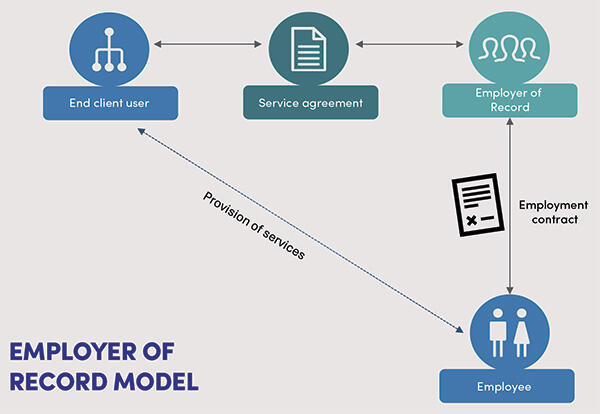

An EOR is a third-party service provider that acts as the legal employer of an individual and discharges ‘employer functions’ in the work location; for example, income tax and social security payroll withholding, and provision of other mandatory benefits. The EOR then assigns the individual exclusively back to the end-user organisation, via a service agreement, which provides control over the day-to-day activities, job duties and responsibilities of the worker. See the Employer of Record model opposite.

The Employer of Record model

There are a number of names and acronyms used in the market – such as Global Employment Outsourcing (GEO) and Professional Employer Organisation (PEO) – to describe an EOR (or similar, but nuanced structures).

Whilst it may seem like EORs are a recent phenomenon, they are not new to the market. They are often utilised as an option in the M&A space to aid the transition of employees between organisations where the acquiring party has no current corporate presence in a location where newly acquired employees are working. There has been a period of sustained growth and innovation in the EOR market, fuelled by factors such as the expansion of cross-border business activities, advancements in technology and the rise in remote work.

Are EORs a suitable option to engage talent?

This is a key question, and it is imperative that organisations carry out an appropriate feasibility exercise, as well as ongoing reviews at appropriate regular intervals. The EOR model must fit sufficiently with the strategic objectives of the organisation, alongside other considerations such as meeting the business’s key challenges and managing risk appropriately.

This feasibility exercise should cover multi-disciplinary functions including but not limited to employment tax and social security, corporate tax and permanent establishment risk, indirect tax, employment law, culture, cost, reward and the impact of the draft ‘umbrella company’ legislation.

As always, the benefits of this type of engagement model should be balanced against some potential limitations that organisations will want to be conscious of and manage wherever possible.

Spotlight on UK employment tax considerations

We have seen significant growth in utilisation of the EOR model over the past four to five years and are concerned that organisations are failing to consider the continued employment tax consequences for the organisation as the end user.

A key benefit for many organisations of the EOR model is that the EOR discharges income tax and social security withholding and other mandatory employer obligations in the country of work. For example, if the individual was employed by an EOR in the UK, the EOR would withhold appropriate Pay As You Earn (PAYE) for tax and social security.

However, there are potential UK employment tax considerations regarding individuals who are employed by EORs outside of the UK, where the individuals mainly perform their duties in the overseas location but come to the UK as short-term business visitors to perform work duties for the UK organisation. This is best demonstrated in an example of how UK employment tax obligations could be triggered in this scenario.

EORs in practice: Nazreet and XYZ Ltd

XYZ Ltd, a UK entity with a PAYE presence, have identified a need to engage the services of an individual, Nazreet, based in India. They have conducted a full feasibility study and determined that they are comfortable with using the EOR model to do this. They have engaged a global EOR, and the EOR’s local India entity employs and pays Nazreet.

Under a service agreement with the EOR, all of Nazreet’s work is performed for XYZ Ltd, and he travels to the UK for around 30 workdays each year as part of his role.

XYZ Ltd will need to assess whether there are any UK employment tax obligations resulting from these UK workdays as follows.

Step 1: Assess whether there is a PAYE obligation

Whilst Nazreet is paid by and employed by the EOR in India, XYZ Ltd exercises management and control (or has a right to do so) over Nazreet. A PAYE obligation will therefore exist as Nazreet is ‘working for’ XYZ Ltd, an entity with a UK PAYE presence.

Step 2: Assess the UK income tax reporting obligations

The dependent services article of the double tax agreement between the UK and India should then be assessed to determine whether there is any relief from taxation in the UK under the agreement, also considering the OECD model convention guidance.

Nazreet will be considered economically employed in the UK by XYZ Ltd as the EOR is unlikely to be able to function as the economic employer, with XYZ Ltd bearing all economic risk and responsibility for the individual’s work. Nazreet’s remuneration is also being paid by the EOR on behalf of the UK resident entity of XYZ Ltd. In the first instance, no relief is available under the treaty.

However, HMRC’s ‘less than 60-day rule’ practice should next be assessed. This enables treaty relief to still be claimed even where an individual is considered economically employed in the UK, and where remuneration is borne on behalf of a UK entity (as above), if the individual is in the UK for such a short period that he can never be integrated into the UK business.

The practice can only apply where the individual is present in the UK for a period of less than 60 days which also doesn’t form more of a substantial period of presence in the UK (considering past and future excepted visits to the UK). The number of tax years to be considered here is open-ended, though many organisations will consider a three to four tax year period to make an initial assessment.

As Nazreet will be coming to the UK for 30 workdays each year as part of his role, it is clear he cannot fall within the ‘less than 60-day’ practice and the double tax agreement cannot be used to relieve the income tax obligation for Nazreet.

Step 3: Assess how the PAYE obligation should be discharged

In the first instance, as there is a PAYE obligation and no relief is available under the double tax agreement, Nazreet should be added to the end client user’s UK payroll and PAYE should be operated on Nazreet’s full remuneration subject to PAYE from day 1.

Further consideration can be taken to determine whether withholding PAYE on 100% of his remuneration PAYE can be relieved, for example, via the Globally Mobile Employees PAYE notification (see tinyurl.com/msunvdfh) or the use of an Appendix 8 agreement (see tinyurl.com/43dz24sm).

Other areas to consider

Some examples of other areas to consider are set out below:

Social security obligations: In the scenario of Nazreet and XYZ Ltd, we note that there is currently no India/UK social security agreement. However, both countries have agreed to negotiate a reciprocal agreement for social security purposes as part of the wider Comprehensive Economic and Trade Agreement. At present, UK domestic law would apply to Nazreet’s social security position. As he is employed outside the UK, he would likely be eligible for an exemption from UK NIC, provided that he is not working in the UK for a continuous period of 52 weeks.

Residence: Nazreet’s residence position should be considered. In the example above, we have assumed that Nazreet is domestically non-resident under the UK’s Statutory Residence Test. Other facts and circumstances may be in play which mean this is not the case and would impact the assessment above. Approaches taken will also impact Nazreet’s personal income tax obligations in the UK; for example, the obligation to file a tax return in the UK if the Globally Mobile Employee PAYE notification agreement is in place.

Tax liability: Who will be liable to pay the UK taxes? If the organisation will cover these taxes, there are additional considerations with regards to the operation of UK payroll, including gross-up taxes. Other questions arise too. How are the taxes paid by the UK entity treated for tax and social security purposes in Nazreet’s home country? If Nazreet is responsible for the taxes in the UK, can and will the EOR agree to deduct those from Nazreet via their Indian payroll?

Length of stay in the UK: What if Nazreet only spent a handful of days in the UK each year? In this scenario, the ‘60-day’ rule could potentially apply if Nazreet is not expected to be present in the UK for more than 59 days across all tax years and these days do not form more of a substantial period of presence in the UK. The company would need to consider Nazreet’s UK days within their organisations’ annual Appendix 4 Short Term Business Visitor reporting to HMRC.

What is the risk of taking no action?

Notwithstanding reputational risk, and the cost of resource and/or specialist advisor fees to resolve non-compliance and support with HMRC enquiries, failure to address ongoing UK employment tax responsibilities could lead to PAYE failure or incorrect reporting under the Appendix 4 Short Term Business Visitor agreement.

This could result in interest being charged and potentially penalties for PAYE failure. HMRC could also cancel the Appendix 4 agreement if dissatisfied with employer controls generally, which would mean an organisation has a day 1 PAYE requirement for any business visitors to the UK where a PAYE obligation arises.

What should companies be doing?

As demonstrated by our example, organisations need to ensure that in their business traveller tracking, they are appropriately including the tracking and assessment of compliance for individuals who are providing services to their company via the EOR model. This should also be assessed as part of the annual process to determine reporting under any Appendix 4 Short Term Business Visitor agreement in place with HMRC. What additional policies, processes and education programmes need to be in place to ensure this monitoring and compliance?

Whilst we have focused on a UK employment tax implication for the EOR model, assessment should be made as to whether there are any similar obligations in any other jurisdictions which the EOR individuals are working in.

There are currently limited published views from country tax authorities on the use of EORs in their geographies. However, as their use becomes more commonplace, we anticipate views and regulations will be forthcoming which will need to be factored into the feasibility and ongoing management of EOR models.

In conclusion

Organisations must ensure that there are appropriate processes in place with regards to assessing continuing employment tax obligations when utilising EORs, and ensure that compliance is handled appropriately once identified. EOR business travellers to the UK cannot safely be ignored.

© Getty images