Employment ownership trusts

Share this article

William Franklin looks at the relative benefits of employee-owned companies

Key Points

What is the issue?

What is an employee owned company?

What does it mean for me?

How is such a company structured?

What can I take away?

In what circumstances might it be appropriate?

When future economic historians assess the long term effects of the Coalition government, it is possible they may one day conclude that the most lasting impact arose from some little noticed legislation in Sch 37 of the Finance Act 2014 (FA 2014). These are the provisions that introduced some new and relatively generous tax reliefs for employee-owned companies.

For these purposes an employee-owned company is a normal limited company which is run on a commercial basis. The key difference is that the majority of the shares are owned by a trust collectively for the long term benefit of the employees as a whole. To distinguish this kind of trust from other forms of employee benefit trusts (EBTs) the trust is normally known as an employee ownership trust (EOT). Employee-owned companies have indirect employee share ownership through the EOT.

In introducing these tax reliefs the government had strategic objectives. It wished to encourage the growth of what is sometimes called a ‘John Lewis economy’. John Lewis is the leading example of a UK business with this indirect employee ownership model. However, John Lewis is by no means the only example and there are many other companies with a similar ownership structure. After the financial crisis the government saw encouraging more John Lewis style companies as one possible way that could help rebalance the UK economy.

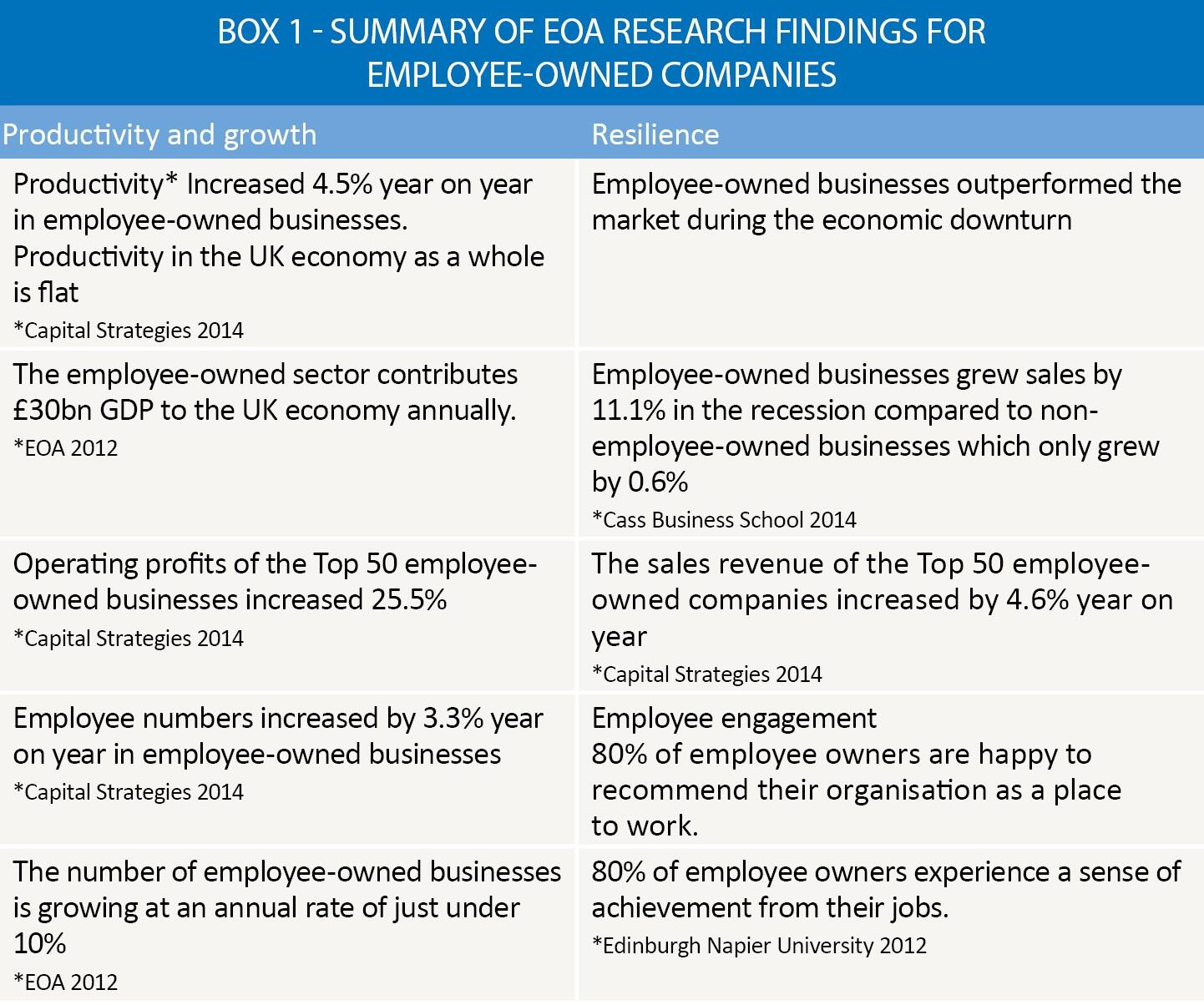

Advocates of the model argue that employee-owned companies display greater resilience to economic fluctuations, and certainly some of them have achieved a longevity and continued independent existence that is somewhat unusual for UK businesses. An association of employee-owned companies known as the Employee Ownership Association (EOA) exists to promote these companies and it has collected research into their economic performance which suggests that employee-owned companies often achieve a strong financial performance. In 2015 the EOA published some findings and these are summarised in Box 1.

Under FA 2014 Sch 37 it is possible for the owners of a company to sell their shares tax-free to an EOT. The sale must be for the majority of the shares so that the company becomes owned and controlled by the EOT.

After the EOT has acquired the shares, it may not have any funds to pay the consideration, and so it is not unusual for all or most of the consideration to be left unpaid until the EOT has received sufficient funds from the company that the EOT has acquired. This might be in the form of a loan by the company, but such loans can trigger tax liabilities under the loans to participators rules, so funding by gift tends to be the preferred approach.

In this scenario, from an economic perspective the purchase consideration is ultimately being funded from future earnings and this can make the arrangement attractive to an owner who wishes to retire. Future earnings that otherwise might have been taxed as income can be released from the business without income tax or National Insurance. However, this benefit is to an extent offset by the fact that gifts to fund the EOT do not qualify as deductions for corporation tax purposes, unlike employee remuneration which would be deductible.

A vendor of the company might, of course, have had the benefit of entrepreneurs’ relief on a conventional sale of the shares and only have had to pay 10% tax on the gain anyway. So, while a tax-free sale is attractive it is unlikely by itself to be a sufficient reason for converting the company into an EOT ownership structure.

Tax considerations should only be a relatively minor factor in a decision to become an employee-owned company. The owners need to have compelling reasons for making such a fundamental change in ownership structure because once a company has become majority-owned by an EOT it is not easy to reverse the structure, as the trustees of the EOT have to act in the long-term interest of employees as a whole.

It is important that the owners think through how the corporate governance of the business will function after the company has become owned by the EOT, and there are many non-tax issues that must be addressed. For example:

- Who should the trustees be and how should they be appointed? It is normal for there to be a corporate trustee and for the corporate trustee board to include employee and independent directors.

- How should employees influence decisions? An employee council is often created that may advise and appoint employee trustee directors, but is it the intention that key commercial decision be referred to employees? If someone later wants to buy the company, should the employees have a vote or even a veto?

While a tax-free sale funded from future earnings has obvious attractions to existing owners who are exiting, indirect collective ownership may not be so attractive to future key employees, if they are denied the opportunity for capital accumulation through direct ownership of shares. However, the government thought about this and another advantage of Sch 37 EOTs is that up to 49% of the shares can remain in direct ownership. Tax-favoured share schemes, such as enterprise management incentives (EMI) and share incentive plans (SIPs) are available as there are special rules for an EOT-owned company with a corporate trustee that set aside the corporate independence requirements that normally would prevent such tax-favoured schemes.

EOT-owned structures with direct shareholdings and or options over shares are often called hybrid schemes. They can appear to offer the best of both worlds, allowing the company to be put on the long-term secure footing of control by indirect employee ownership while allowing individuals to have direct equity participation. An internal market might be created with possibly a separate EBT acting as a company-funded market maker. However, there are issues that need to be carefully considered with such a structure. For example, what is the fair market value of the shares if EOT control means an external sale is highly unlikely? If share options or new shares are issued the company needs to be careful that the EOT’s holding is not accidentally diluted below 51%, triggering clawbacks or other tax charges.

A case study that explores the potential tax and other issues that need to be addressed when a company considers moving to an EOT owned structure is set out in Box 2.

Schedule 37 also provides another tax sweetener to encourage more employee-owned companies. The company (not the EOT) can pay tax-free annual cash bonuses up to a value of £3,600 per employee. This is a cash bonus, not a dividend, and so it can be paid without the company having to make a profit or have distributable reserves.

The EOT-owned company legislation does not exempt sales of shares into such structures from the transactions in securities rules set out in Income Tax Act 2007 ss 682 et seq. This means that the funding of the consideration paid by the EOT from future earnings generated by the company could potentially create an exposure under this legislation. Therefore, many companies will wish to obtain an advance clearance from HMRC that the transactions in securities provisions will not be invoked. If the sale of the shares is intended to create a genuine employee-owned company and the transaction is carefully explained to HMRC, then it is unlikely that it will withhold a clearance. The continued relevance of this legislation is likely to act as a deterrent to those who might seek to use the tax reliefs for potentially abusive purposes.

EOT-owned companies are not a complete solution and most owners and companies will probably not wish to make use of these tax advantages, but it is hoped that a significant minority of entrepreneurs and their advisers will at least consider the EOT route when considering exit planning.

Since the legislation was introduced growth in the number of companies in the sector has continued and appears to be modestly increasing. The model seems to appeal particularly to smaller professional service firms or other people businesses which need to retain good quality staff. Whether the changes will have the effect hoped for and the employee-owned company sector becomes a substantial part of the UK is something that may have to be left to the economic historians to decide.