Encouraging growth

Share this article

William Franklin and Alan Garrod consider the importance of robust share scheme incentives in rewarding employees of all salaries and ages

Key Points

What is the issue?

Our erratic and illogical tax rates on income mean that bonuses paid in a single year for performance over number of years can suffer unfairly high marginal rates of tax which can seriously detract from their effectiveness as incentives.

What does it mean for me?

This is a problem for middle managers and lower paid employees and will become an increasingly acute problem for young graduates who face very high marginal tax rates on their income because of the Disguised Graduate Income Tax.

What can I take away?

Well designed share schemes can substantially moderate the distortions which have accumulated in our tax regime on income over the past 30 years. But they are too often overlooked and undervalued for moderately or averagely paid workers.

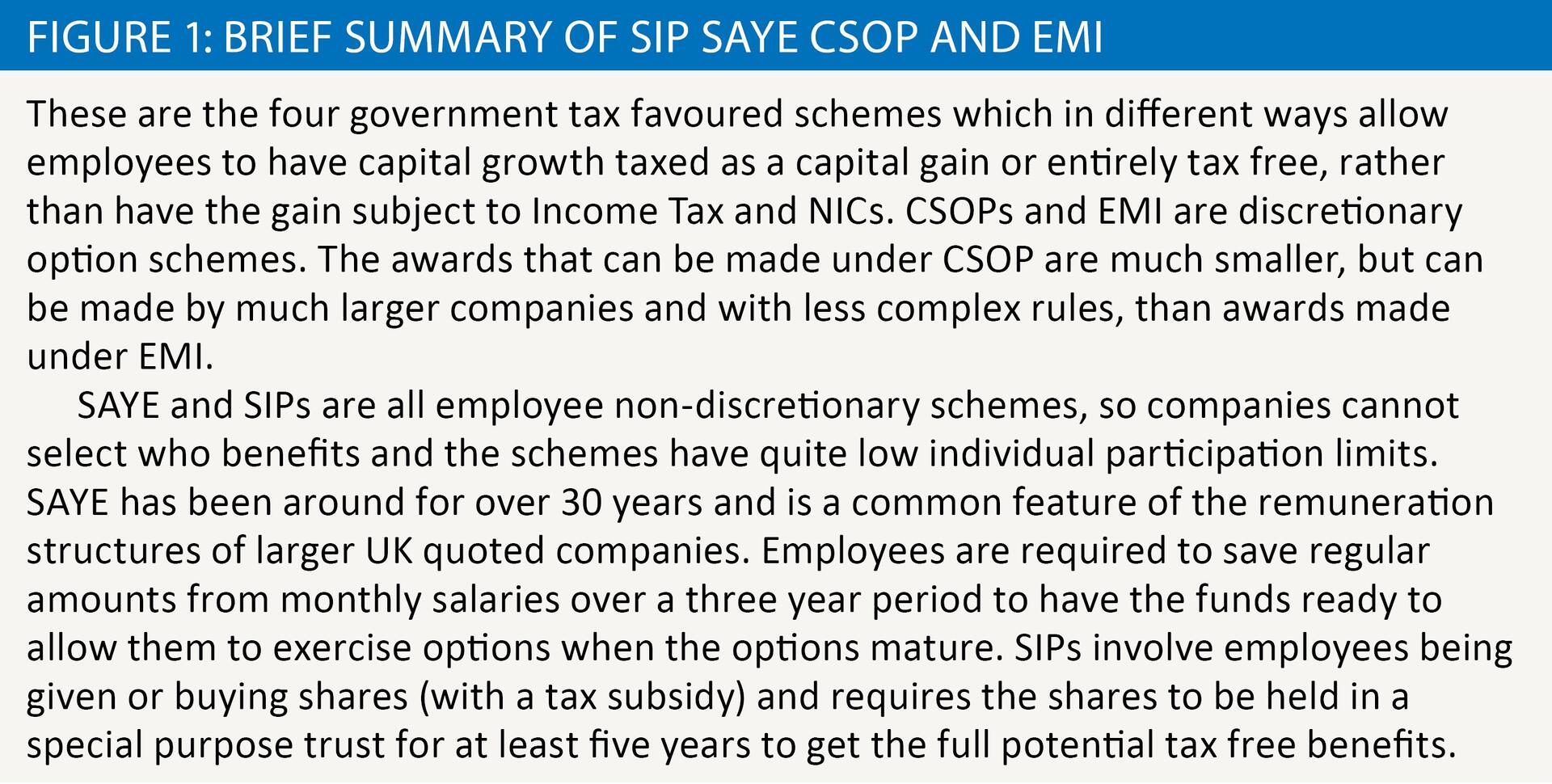

In the UK our tax system is often said to encourage the use of employee share schemes. That view is based on the existence of a number of government tax favoured schemes such as CSOP, SAYE, SIPs and, in particular Enterprise Management Incentives (EMI) (see figure 1). Broadly speaking, these schemes seek to put employees in a similar position to the owners of companies and align the interests of employees and owners. They aim to encourage and reward growth and achieve parity of tax treatment by taxing growth as a capital gain, in much the same way as the owner would be taxed.

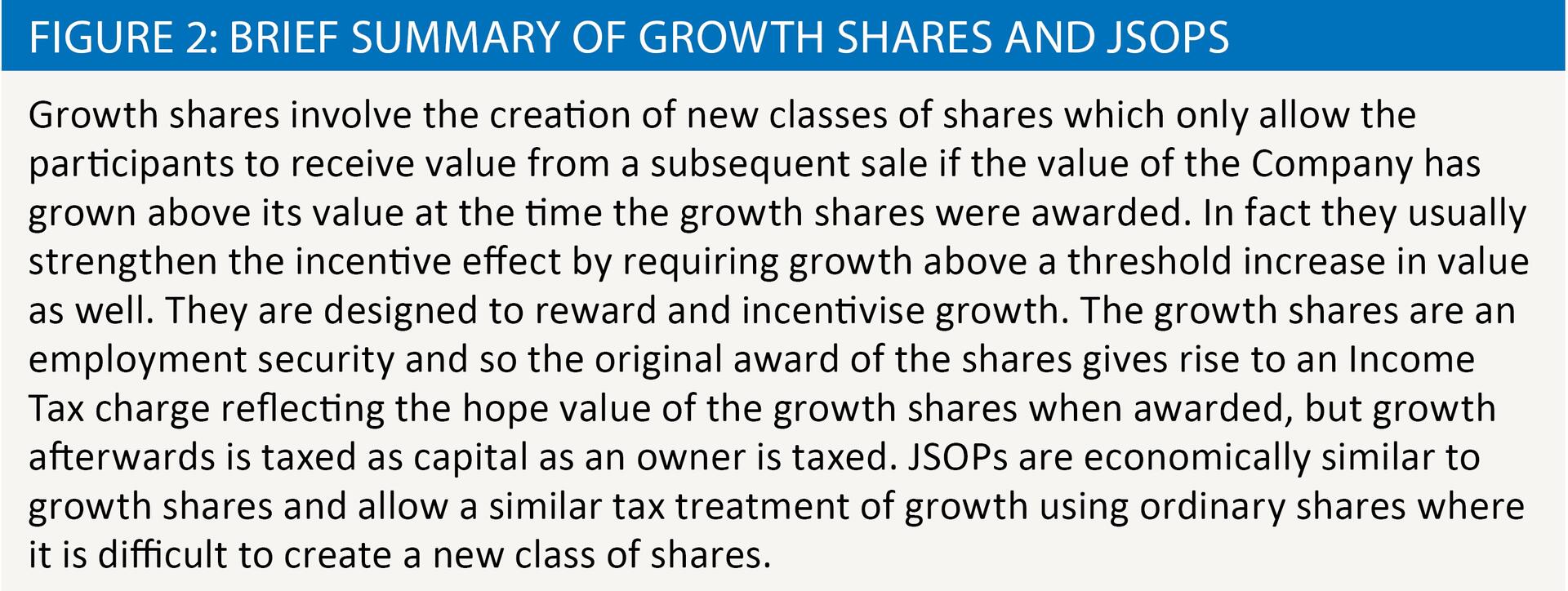

However, these schemes mask the underlying harshness of the overall ‘employment tax regime’ when these government schemes or other structures, such as Growth Shares or Joint Share Ownership Plans (JSOP) (see figure 2 for summaries) are not available, or are not used. We have a tax regime on employment income, which as a result of cumulative changes over more than a couple of decades has become for many key employees rather arbitrary and harsh. In particular, for many younger working people on whom growth in the economy depends, the employment tax regime could actually discourage them from participating in share based incentives if these tax favoured arrangements were not available.

An option which is granted outside one of these schemes has no tax on its grant. Such options are known in outdated tax jargon as Unapproved Share Options. However, once such an option is exercised a harsh tax regime begins. The gain on exercise, (which is the difference between the market value of the shares on exercise and the exercise price of the option which the employee pays to acquire the shares) is taxed as income. Very often the shares at the time of exercise will fall within the now widely drawn definition of ‘readily convertible assets’ bringing them also into the regime of PAYE. As a result, the ‘gain’ will be subject to National Insurance (Employee’s and Employers) as well as income tax. Because PAYE applies these employment ‘taxes’ have to be paid to HMRC within a few weeks of the exercise of the options by the company which then has to recover the income tax and Employee’s National Insurance from the employees otherwise there is an additional penal tax charge.

If the option is exercised without the employee having the opportunity to sell the shares, because the company is unquoted, the employee not only has to fund the exercise price to acquire the shares but also has to pay tax on an unrealised gain. This is an example of a dry tax charge because the employee has a tax liability from an event (exercise) but no cash proceeds from the event with which to pay the tax. It is hard to imagine a tax regime less conducive to employees wishing to become long term shareholders in unquoted companies that are not planning an imminent sale or other liquidity event. For a wealthy individual a dry tax charge might be just about tolerable but for a young worker hard pressed with student loans, rent or mortgages, the costs of starting a family and providing for retirement as well as normal living expenses, such as a dry tax charge is about the last thing one could want. This tax regime reinforces the UK’s business culture which has for many years encouraged unquoted companies to seek early exits rather than long term independence, organic growth and the creation of large scale companies.

One way of alleviating the dry tax charge would be for the income tax and National Insurance to be deferred until the shares were actually sold and the employee had the money to pay the tax. Ideas along these lines were proposed to the Office of Tax Simplification a few years ago but fell on deaf ears at the Treasury, who were apparently more concerned about the risk of losing immediate tax revenue than encouraging long term employee share ownership.

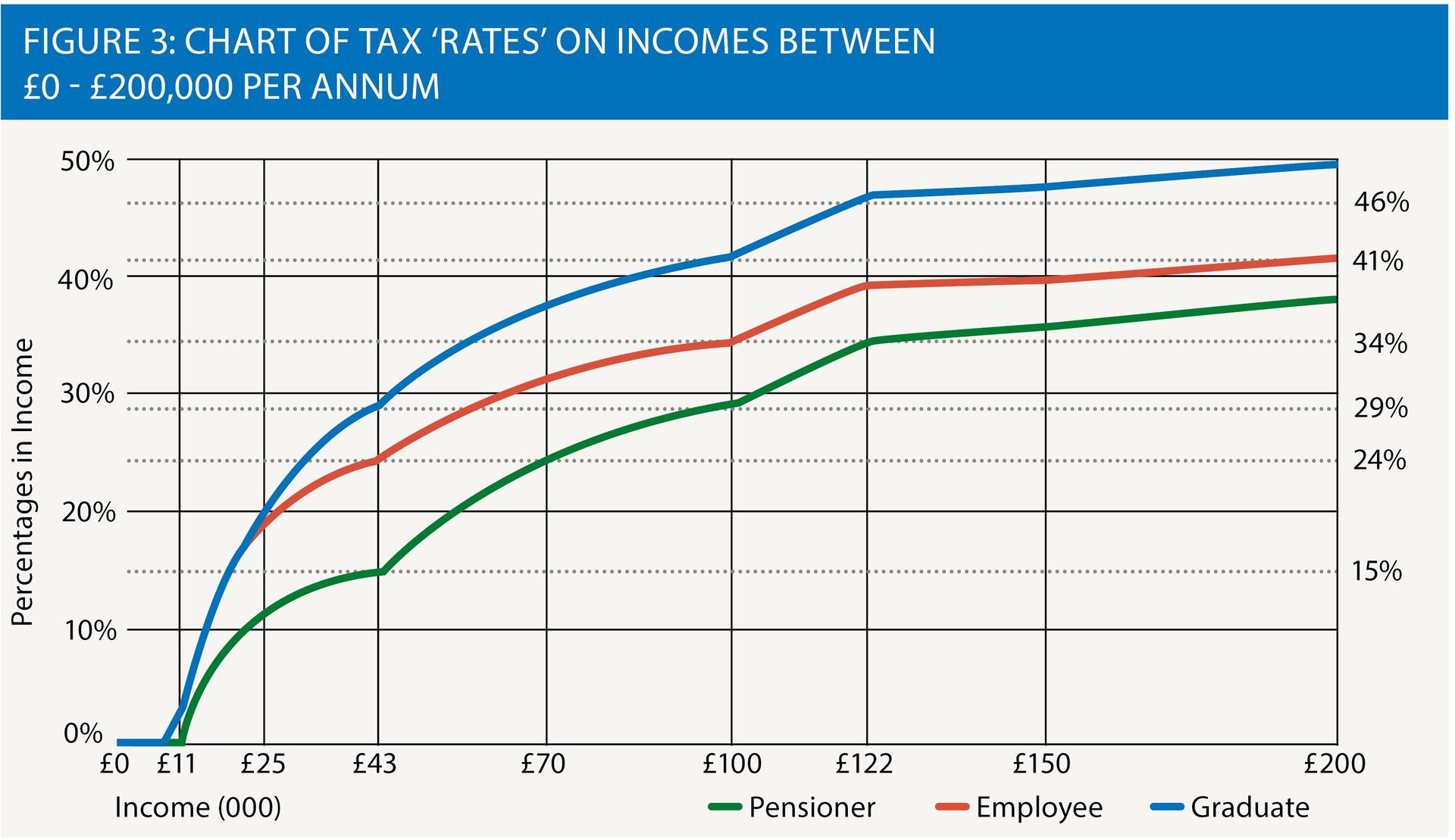

In addition to the harshness of taxing unrealised gains, the employment tax regime can also cause employees to pay seemingly disproportionate amounts of their gains as tax. An employee who participates in a share scheme will usually receive the gains in a lump in a single tax year. But it would have been a long term incentive, which was intended to reward long term performance and contribution over a number of years. If the taxable value of the share based gain for an employee is large relative to the person’s annual income in a particular year and is taxed as income not capital it can push the employee’s total income in that year through the erratic ‘tax’ bands on employment income that now exist (see figure 3 for a graphical illustration of 2016/17 tax rates). A surprisingly large proportion of gains will then be taken by the taxman, detracting significantly from the incentive effect of the equity incentives. It is not surprising therefore that, share schemes, such as EMI, which protect the gain from being taxed as income are so keenly sought by companies offering employee share based incentives.

How is it that we have such erratic and irrational tax bands on income? While income tax rates have generally fallen since the 1970s National Insurance contributions have been increased and now the total revenues raised by the government from income tax and National Insurance is approaching parity. Other changes to the tax and benefits system such as the clawbacks of family allowances (child benefits) for incomes over £50,000 and of personal allowances for incomes over £100,000, the restrictions on working family tax credits and pension tax reliefs contribute to creating high, complex and erratic combined marginal rates of income tax and National Insurance.

There are age based effects as well that add to the distortions. Employee National Insurance is not payable after reaching retirement age. By contrast, the new generation of graduate workers who went to university after 2012 (‘new graduates’), are now burdened with even higher levels of student debt than their immediate predecessors. For post 2012 students it is hard not to conclude that (because the loans are much larger and will normally increase each year by interest charges of about 3% + RPI) the student loan regime is effectively an additional Disguised Graduate Income Tax of 9% on most of their earnings for at least the first 30 years of their working lives.

For employees on less than twice national average earnings even a modest gain can be sufficient to push an employee into the higher rate 40% tax band and if they have children trigger the clawback of child benefit or family allowances, giving eye-wateringly high effective marginal rates of ‘tax’ on their remuneration from work.

This is a very different and much more complex overall employment tax regime than a basic rate of 20% and a higher rate of 40% established in the late 1980s when the then Chancellor Nigel Lawson cut higher income tax rates but failed to integrate National Insurance with income tax.

The jargon of National Insurance can mislead people into thinking that they have paid into a fund. Over the years various Chancellors (e.g. Lawson and Osborne) have raised the possibility of recognising reality by consolidating income tax and National Insurance into a single combined tax on income but have backed away from making changes from the fear of the political backlash of vested interests such as the retired who escape National Insurance on their retirement income.

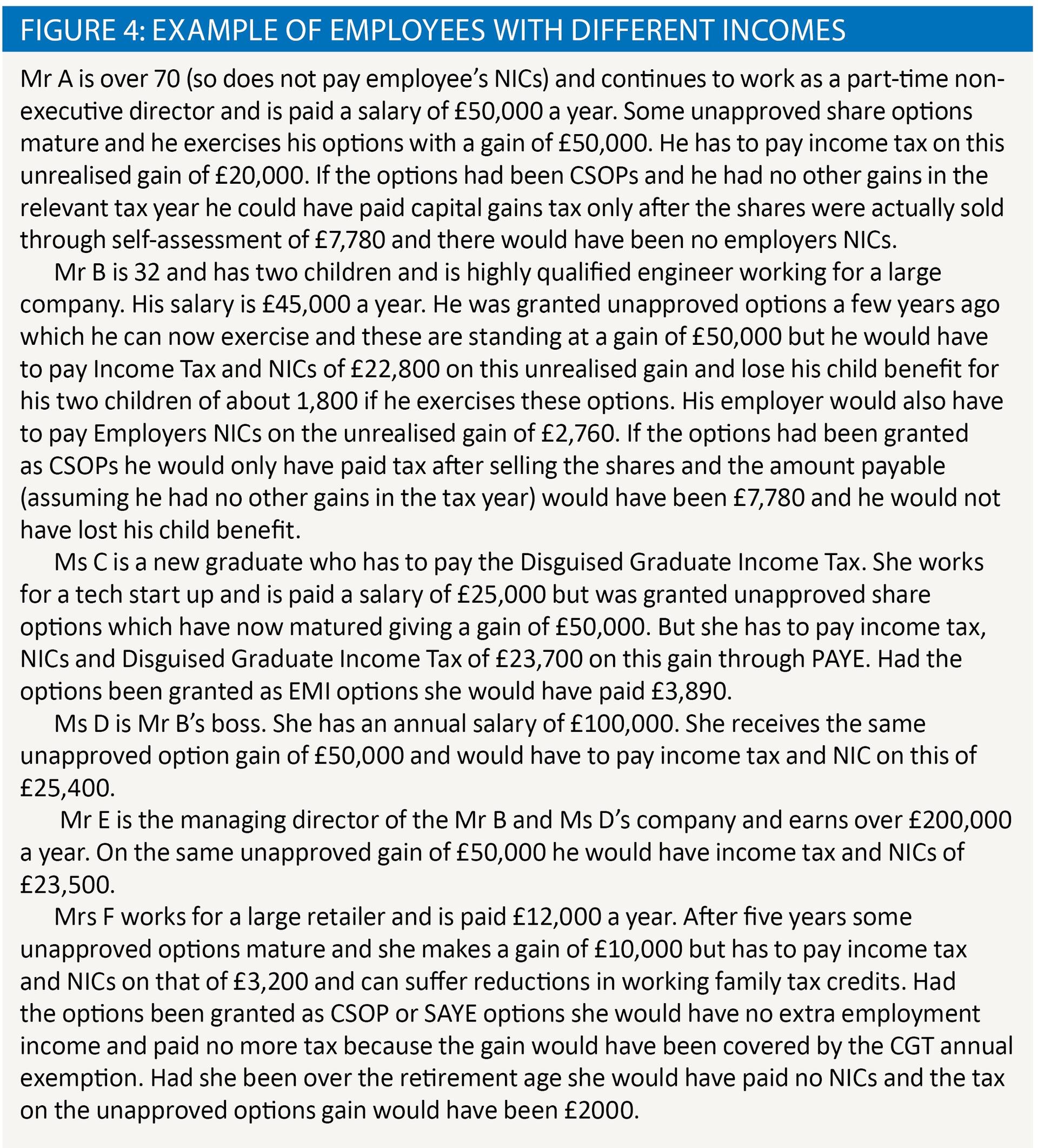

When Lawson changed the rates of income tax he also equalised the rates of income tax and capital gains tax. However, subsequent, governments in order to encourage growth and entrepreneurial activity reduced the tax rates on capital gains significantly and after 2000, EMI options were introduced which allowed option gains to be taxed as capital and encouraged the use of options among smaller companies with growth potential. As is illustrated in the examples of employees with different incomes in figure 4, a capital gains tax treatment considerably moderates the harsh effects of lump sum options gains being taxed as income.

Faced with a seemingly intractable deficit and growing demands for increased spending, the pressures on government to raise more taxes show no sign of abating. But as Britain approaches Brexit and the pressures on our companies to compete in global markets intensify our political leaders would be well advised to remember that our tax system needs to encourage and reward growth and enterprise and work, rather than penalise them; and do this for the many and not just the few.

Share schemes have an important role to play in encouraging growth and softening the basic harshness of a tax regime which would otherwise treat unrealised lump sum gains as income and subject them to the complex and distorted system of ‘taxes on employment income’ which the UK now has. It is important that they do because if an award falls outside these favoured schemes it suffers a treatment reminiscent of the tax regime of the 1970s stagflation era.