The end of an era

Share this article

William Franklin considers the implications of the withdrawal of post transaction valuation checks

Key Points

What is the issue?

Earlier this year HMRC withdrew procedures whereby some share valuations for employee share schemes could be agreed promptly.

What does it mean for me?

As a result of this change there will be greater uncertainty as to the tax liabilities that may arise on some share awards.

What can I take away?

Different approaches and thinking will be needed to manage the associated heightened tax risk for clients.

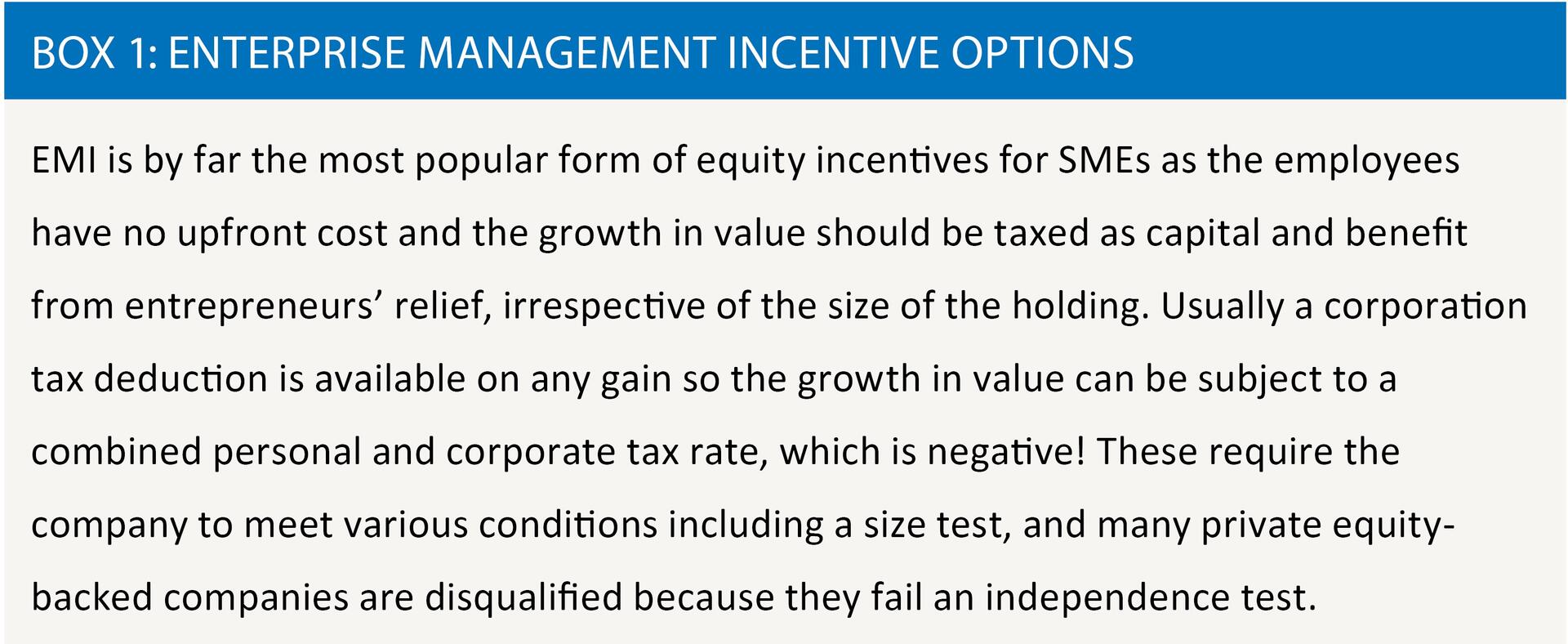

HMRC’s specialist Shares and Assets Valuation (SAV) Department in Nottingham (previously known as Shares Valuation Division (SVD)) receives consistently high ratings in surveys of its users. However, it is doubtful if it would always have been so highly regarded. Readers with long memories may recall the trench warfare that often prevailed in the last century between taxpayers and their advisers and HMRC. Too often, share valuations become lengthy legalistic battles over case law that had little relevance to modern business practices. For the last 15 years at least, the culture has been different. With the introduction of Enterprise Management Incentive (EMI) options (see box 1), it was recognised that optionholders and their employers were going to need certainty as to the value of the shares under the option. This helped foster a more pragmatic and commercially minded approach to fiscal valuations for share schemes among HMRC and advisers.

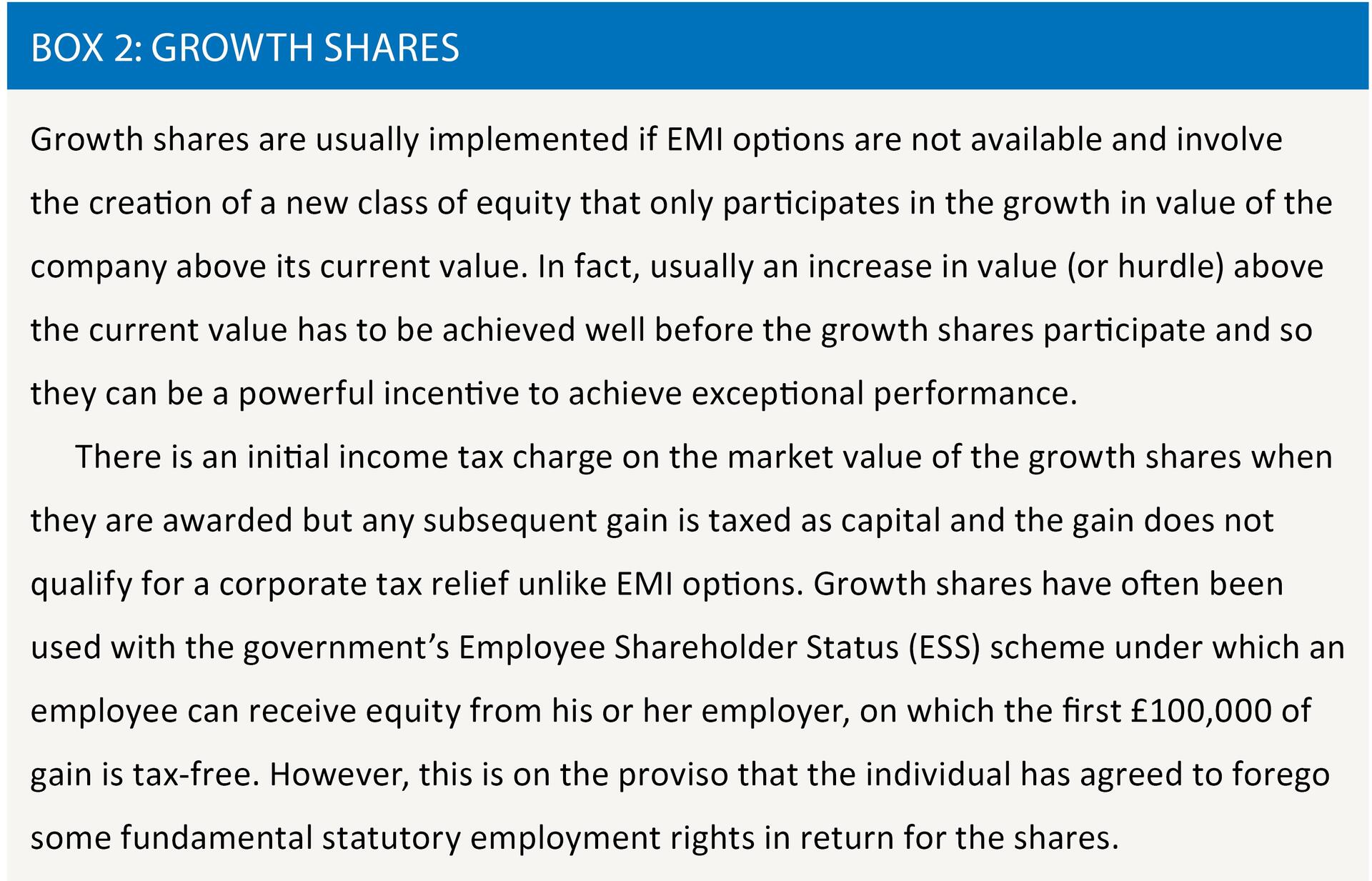

HMRC SAV became an important factor in the spread of equity incentives both EMI and non EMI amongst unquoted companies in the UK. SAV adopted a public service role of providing certainty for taxpayers; as well as raising revenue for the government and managing the tax system. However, with the government’s continuing deficit and pressure to reduce the running costs of government, it was perhaps inevitable that this wider public service role would come under scrutiny. This year, HMRC announced that they were withdrawing two longstanding non-statutory valuation agreement procedures: Post Transaction Valuation Checks (PTVCs) for ITEPA and Best Estimates for PAYE. These had often been used by larger unquoted companies that were too big to qualify for EMI options and had made other equity awards often in the form of growth shares (see box 2).

Consultation by HMRC, before they made this announcement, was limited. Some time before the announcement, HMRC had indicated at Fiscal Forums (an annual meeting between HMRC and share valuation specialists) and elsewhere that they might not be able to sustain these services. HMRC appealed to share valuations specialists to make it easier for them to understand the valuations of growth shares with complex legal drafting, which were time consuming for their staff to review. They asked for worked examples to analyse and illustrate the operation of the shares in different scenarios. But these appeals mostly went unheeded by outside advisers and the pressure on HMRC resources continued to grow.

After the announcement, HMRC sought to explain their reasons at meetings with interested parties and pointed out that in almost 90% of PTVC and Best Estimate cases the proposed valuations were accepted by HMRC. HMRC (not unreasonably) pointed out that, with valuers consistently getting valuations right, these reviews were a poor use of the department’s manpower. Following these discussions HMRC provided a breakdown of their workload. In 2015, the department dealt with about 14,000 share valuations of which 5,000 were EMI valuations. There were about 800 valuations for Employee Shareholder Status (‘ESS’) awards, 600 PTVC ITEPA valuations and 50 PAYE Best Estimate valuations. The rest were an assortment of valuations including: valuations for Share Incentive Plans (SIPs), Company Share Option Plans (CSOPs), PTVCs for CGT, Corporation Tax relief on option exercises and IHT. Many of the cases were referrals by local tax inspectors from reviews of personal and corporate tax returns.

Historically, many EMI options have not resulted in large gains being realised and many of the companies that use EMI are small and of low value when the awards are granted. This has encouraged HMRC to adopt a risk-based approach to the level of scrutiny and so HMRC have sought to restrict the significance of EMI agreements by saying they are only agreed for EMI purposes.

It is possible for the same shares to have different theoretical valuations. The value can differ with the size of the holding and the standard of information assumed. Fiscal valuations differ from commercial valuations because they need to reflect the law, cases and practices relevant for tax valuations. These differ from country to country so there may be different values in different jurisdictions. However, whether limiting the relevance of a valuation, simply because of the level of scrutiny HMRC choose to adopt, is logical and legally sustainable has yet to be tested in the courts.

Even with a risk-based approach, EMI valuations continue to absorb significant amounts of HMRC’s manpower and so they also announced that they were intending to examine EMI and other valuation procedures for efficiencies; suggesting that they might change these to some form of self-certification procedure. However, it is not clear how a self-certification procedure would work, and change would not be easy to implement where the existing procedures have a statutory basis.

One of the reasons PTVC valuations often absorbed so much time was that growth shares are much more difficult to value than ordinary shares. Ordinary shares reflect the current value of a company and there are established methodologies using historical performance to value ordinary shares, whereas growth shares – intended to encourage business growth – do not derive value from the current value of the company but from the hope value of future growth. This is inherently uncertain and dependent on future events over several years. Valuation methodologies such as earnings multiples and net assets are not easily applicable or even relevant.

Some people therefore argue that growth shares have no value, other than nominal value, particularly if the hurdle in the growth shares is demanding. This reasoning is often combined with the argument that for tax valuations the information standard means that future prospects and forecasts of the company would be confidential, and therefore excluded from consideration in preparing the valuation.

This reasoning has, in the past, been quite widely followed and, in some cases, accepted by HMRC for growth shares though it has not been tested in the courts. Nowadays, HMRC increasingly challenge this reasoning on the common sense grounds that: ‘why would a company go to the trouble of making complex changes to its articles to create a new class of shares to incentivise key employees if there was no expectation that shares could have some meaningful value in the future?’ HMRC argue that, if there is such an expectation, then the hope value today cannot be nil, although they acknowledge it might be quite small.

How then is this value to be determined? One approach is to rely on the ‘gut feel ‘of the valuer and how much he personally would pay to buy such a share. With so much uncertainty, such a subjective approach is not as unreasonable as it might seem, although it does rely on personal judgement, lacks any objective analysis and could give rise to inconsistent valuations. There are some advanced valuation techniques, such as the Capital Asset Pricing Model and Black Scholes option pricing theory, which might be used and one of the challenges facing valuers today is to develop more consistent and practicable bases for valuing growth shares.

If growth shares meet the conditions for ESS, then it is still possible to seek an early agreement from HMRC as to the value of the growth shares. Otherwise now, following the withdrawal of PTVCs, the normal route for the taxpayer to obtain certainty as to the market value, will be through the submission of personal tax returns. This is not a speedy process.

Employees need to disclose on their personal tax returns details of awards received and tax already paid on their behalf through PAYE. Although there is some ambiguity in tax returns as to what information needs to be disclosed, these tax returns give employees the opportunity to have the valuation effectively agreed by HMRC in due course. With the increasing digitisation of the UK tax systems, it will be important that the information disclosed by the Company in its annual share scheme return to HMRC (formerly called Form 42) is consistent with personal taxation returns, otherwise taxpayers may face unnecessary questions if there are inconsistencies between personal and corporate tax returns. With the normal time delays for submitting tax returns and agreeing the individuals’ entire tax affairs, there will be a considerable delay in effectively reaching an agreement (compared with the old PTVC procedures) for the year with the share award, even if no questions are raised on the valuation itself. Furthermore, self-assessment will not generate letters from HMRC formally agreeing valuations.

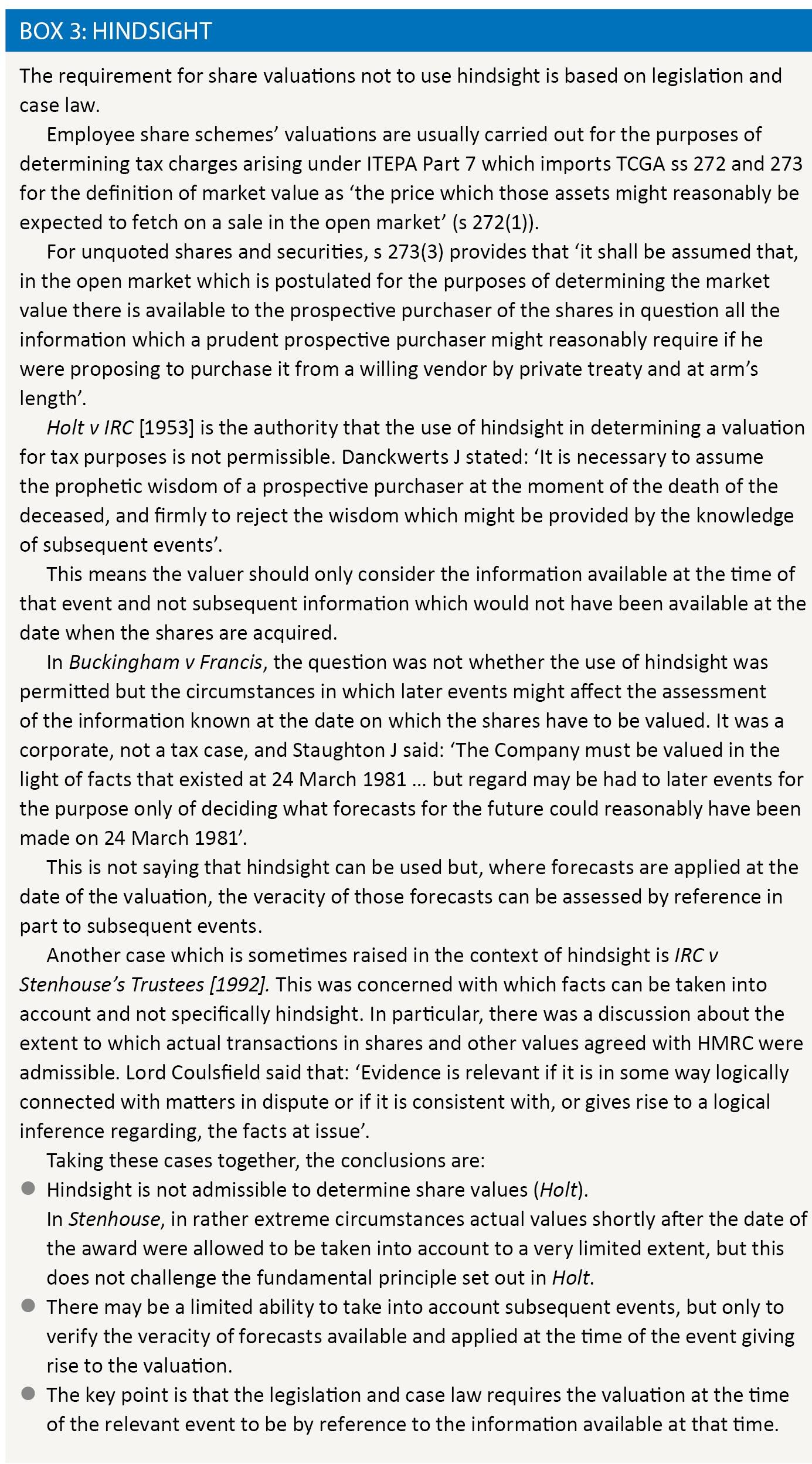

Any review under self-assessment by HMRC of a growth share valuation is likely to occur some years after the date of the award. This will give rise among taxpayers to concerns that hindsight will be applied in future reviews of valuations. However, fiscal valuations are not supposed to use hindsight and this rule is (by and large) followed by HMRC and taxpayers, although the position is not quite as clearcut as sometimes supposed (see Box 3). But as the valuation of growth shares is based on an assessment of future events, concern is understandable that, as HMRC’s review will be in the future, it might to some extent, be coloured by hindsight. The company will need to carefully document its reasoning and the evidence of the circumstances in existence at time of grant to be able to resist such challenges if they arise.

Employee share schemes are often key to the incentive arrangements for the managers and other key employees of SMEs and larger unquoted companies. They encourage managers and employees to think like owners and to grow the business. They can promote internal harmony by giving the employees broad parity of capital tax treatment with the owners. The concern is that the loss of certainty of the value of employee share awards, and therefore any potential upfront tax charge, may discourage their use. If the current regime for agreeing EMI valuations were to be withdrawn, these concerns would be heightened. This is a serious issue because, if managers are not incentivised to grow the country’s larger SMEs and unquoted companies, these companies may stagnate and not achieve their potential. That would be a very bad thing indeed for the UK economy.